IN THE HIGH COURT OF ALLAHABAD

Saral Srivastava, J.

Mohd. Ashif Khan and another - Petitioner

Versus

State of U.P. and others - Respondents

Civil Misc. Writ Petition No. 26636 of 2012

Decided On : 30-01-2024

Stamp Duty - Indian Stamp Act - Section 47A - The court interpreted Section 47A of the Indian Stamp Act regarding the determination of stamp duty deficiency, emphasizing the importance of the land's potential use at the time of sale and the burden of proof on the state.

Fact of the Case:

The petitioners challenged the Collector's order determining a deficiency in stamp duty on a land purchase, asserting it was agricultural land and that they paid the correct stamp duty based on its classification.

Finding of the Court:

The court found that the Collector's determination was justified based on evidence of residential use from a related sale-deed, despite the petitioners' claims of agricultural use.

Issues: Whether the Collector's determination of stamp duty deficiency was valid given the evidence of residential use and the procedural compliance with the relevant rules.

Ratio Decidendi: The court held that the potential use of land at the time of sale is relevant for determining stamp duty, and the state met its burden of proof by presenting evidence of residential use.

Result: The writ petition was dismissed with no order as to costs.

JUDGMENT :

Saral Srivastava, J.

Heard learned counsel for the petitioners and Sri Rishi Kumar, Additional Chief Standing Counsel for the respondents.

2. The petitioners by means of the present writ petition have assailed the order dated 22.3.2010 passed by respondent No. 3-Collector Stamp/District Magistrate, Shajahanpur in Stamp Case No. 67/24/2009, under Section 47A (3) of the Indian Stamp Act determining the deficiency of stamp duty to the tune of Rs. 14,53,410/- and, imposition of penalty of Rs. 1590/- and interest at the rate of 1.5% per month, and the order dated 25.4.2012 passed by the respondent No. 2-Chief Controlling Revenue Authority/Board of Revenue U.P. at Allahabad in Stamp Appeal No. 50/2011-12 affirming the order passed by the respondent No. 3-Collector Stamp.

3. The facts, in brief, are that the petitioners through sale-deed No. 8006/2009, dated 13.4.2009, purchased a piece of land measuring area 1.166 hectares i.e. 11,660 sq. meters from plot No. 64 having a total area of 2.485 hectares situated in the village Northern Area of the City outside Chungi near Village Chinnaur for agricultural purpose and paid stamp duty as per the circle rate prevailing in the area applicable for agricultural land i.e. Rs. 9,42,000/- per hectare (hereinafter referred to as the 'plot').

4. According to the petitioners, the distance of the plot purchased by them from the road is about 1 kilometre and the Abadi is also about 1/2 kilometre from the plot. Since the use of the plot on the date of the sale-deed was agricultural, therefore, the petitioners paid the stamp duty of Rs. 77,000/-.

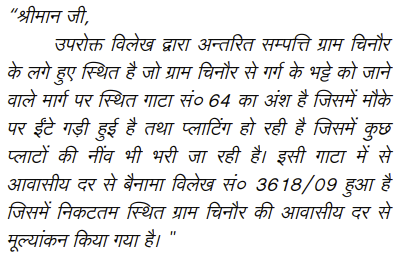

5. It appears that an inspection of the plot was conducted by the Sub Registrar, Sadar, Shahjahanpur on 11.8.2009. He found that Gata No. 64 is situated on the road connecting to brick-klin (Bhatta), and the bricks have been stored on the plot, and plotting activities were also being carried out over the plot. The report of the Sub-Registrar further stated that another sale-deed No. 3613/09 was executed from the same plot. In the sale-deed No. 3613/09, stamp duty was paid as per the circle rate applicable to the residential area. The Assistant Collector (Stamp) registered a case based on the report of the Sub Registrar, under Section 47A(3) of the Indian Stamp Act as case No. 67/24/2009 and issued notice to the petitioners calling upon them to submit an objection about the deficiency in payment of stamp duty.

6. The petitioners submitted an objection contending inter alia that the report of the Sub-Registrar is based upon incorrect facts. It is also stated that the plot is an agricultural plot and is surrounded by agricultural land, therefore, the petitioners have paid the correct stamp duty as per the circle rate applicable to the agricultural land.

7. The Collector (Stamp) rejected the objection of the petitioners by recording a finding that the stamp duty as per residential area was paid in respect to another sale-deed No. 3613/09 purchased from the same plot which establishes that the residential activities are being carried out in the vicinity of the plot, and the petitioners have submitted incorrect map alongwith the sale-deed to pay insufficient stamp duty. Accordingly, he concluded that the petitioners are liable to pay the stamp duty applicable to the residential land. Consequently, he determined the deficiency of stamp duty to the tune of Rs. 14,53,410/-. He further imposed a penalty of Rs. 1590/- and interest at the rate of 1.5% per month on the deficient stamp duty.

8. The order passed by the Collector Stamp was assailed by the petitioners in statutory appeal being Stamp Appeal No. 50/2011-12. In the memo of appeal, petitioners have specifically stated that the report of the Sub-Registrar was ex-parte and no spot inspection was carried out by the Collector Stamp before determining the stamp duty. It is further stated that the sale-deed No. 3613/09 is not relevant for the determination of the present case.

9. The Respondent No. 2-Chief Controlling

The potential use of land at the time of sale is critical in determining stamp duty, and the burden of proof lies with the state to show that the correct duty was not paid.

The Collector must follow due process and provide notice before determining stamp duty; reliance on ex-parte inspections without evidence contravenes procedural laws.

Point of Law : Person presenting the instrument is required to disclose the nature of economic activity, industrial development, if any, prevailing in the locality where the property is situated and ....

The necessity of conducting a spot inspection before determining stamp duty to ensure assessments are based on factual evidence rather than presumptions.

The matter is remitted to the respondent no.2 or the competent authority who may be seized of the matter, to assess the market value taking into account the monetary consideration reflected in the ex....

The classification of agricultural land cannot be altered based solely on its proximity to commercial activity without proper legal declaration.

The classification of land for stamp duty must be based on actual use and verified inspections, not merely on surrounding residential activities.

Stamp duty on agricultural land cannot be evaluated at residential rates without a legal declaration, reinforcing the agricultural character despite proximity to residential properties.

Agreement to sell – Imposition of enhanced stamp duty and penalty – Power of Collector cannot be unduly circumscribed by ruling out potential to which land can be advantageously deployed at the time ....

An indispensable Tool for Legal Professionals, Endorsed by Various High Court and Judicial Officers

Please visit our Training & Support

Center or Contact Us for assistance

Scan Me!

India’s Legal research and Law Firm App, Download now!

For Daily Legal Updates, Join us on :