HIGH COURT OF BOMBAY

G. S. Kulkarni, Aarti Sathe, JJ

CHEC-TPL Line 4 Joint Venture – Appellant

Versus

Union of India – Respondent

WRIT PETITION NO.2583 OF 2025

| Table of Content |

|---|

| 1. challenges rejection of inverted structure gst refunds. (Para 1 , 2) |

| 2. itc accumulates from higher input tax rates. (Para 3) |

| 3. sc upholds rule 89(5), excludes input services. (Para 4 , 5) |

| 4. resubmitted refunds rejected despite notification 14/2022. (Para 6) |

| 5. petitioner urges retrospective notification 14/2022 application. (Para 7 , 8) |

| 6. gst council amends formula per sc urging. (Para 9 , 10) |

| 7. rule 89(5) includes input services in refund formula. (Para 11) |

| 8. amendment clarificatory, retrospective for timely claims. (Para 12) |

| 9. gujarat hc rulings affirmed by sc dismissals. (Para 13 , 14 , 15) |

| 10. court quashes orders, grants inverted structure refund. (Para 16 , 17) |

ORAL JUDGMENT – (Per : G.S.Kulkarni, J.) :-

1. Rule. Rule made returnable forthwith. Heard finally with the consent of the parties.

2. The Petitioner in this petition under Article 226 of the Constitution of India is aggrieved by the rejection of refund claims for the accumulated tax credit due to inverted tax structure concurrently by the Original Authority as also in appeal by the Appellate Authority. The substantive prayers as made in the petition are required to be noted, which read thus :

“(a) that this Hon’ble Court be pleased to issue a Writ of Certiorari or a writ in the nature of Certiorari or any other writ, order or direction under Article 226 of the Constitution of India calling for the records pertaining to the Petitioner’s case and quash and set aside the Order-in-Appeal No.SG/JC/GST/189-195/RGD/APP/ 23-24, dated 31.10.2023 (viz.Impugned Order 1) issued by the Respondent no.2;

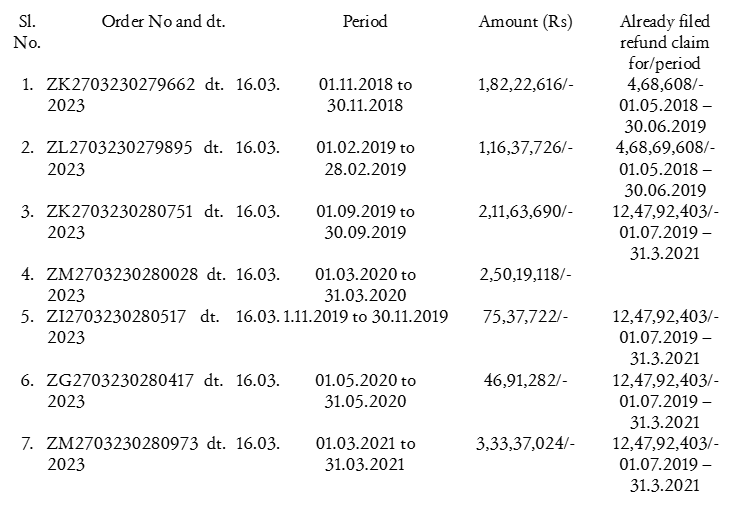

(b) that this Hon’ble Court be pleased to issue a Writ of Certiorari or a writ in the nature of Certiorari or any other writ, order or direction under Article 226 of the Constitution of India calling for the records pertaining to the Petitioner’s case and quash and set aside the Order-in-Originals (i) ZK2703230279662 dated 16.0.2023, (ii) ZL2703230279895 dated 16.03.2023, (iii) ZK2703230280751 dated 16.03.2023, (iv) ZI2703230280517 dated 16.03.2023, (v) ZM2703230280028 dated 16.03.2023, (vi) ZG2703230280417 dated 16.03.2023 and (vii) ZM2703230280973 dated 16.03.2023, all issued by the Respondent no.3;

(c) this Hon’ble Court be pleased to issue a writ of mandamus or any other appropriate writ, order or direction ordering and directing the Respondents to forthwith grant the refund of Rs.12,16,09,178/- as claimed by the Petitioner vide seven (7) separate applications for the period viz. (i) August 2018 to November 2018 (ii) December 2018 to February 2019 (iii) April 2019 to September 2019 (iv) November 2019 (v) December 2019 to March 2020 (vi) May 2020 and (vii) August 2020 to March 2021 along with interest.”

3. Briefly the case of the Petitioner is to the following effect.

The Petitioner is an unincorporated joint venture between China Harbour Engineering Company (CHEC) and Tata Projects Limited (TPL). It is engaged in providing works contract primarily to its customer Mumbai Metropolitan Region Development Authority (MMRDA) in relation to construction of metro rail works. It is not in dispute that the Petitioner had obtained Goods and Service Tax (GST) registration in the State of Maharashtra being Registration No.27AADAC6040JIZU. The Petitioner has contended that it discharges GST @ 12% on the services provided as per the rate prescribed in Notification No.11/2017-Central Tax (Rate) dated 28th June 2017. The Petitioner has contended that the Petitioner procures various inputs and input services that are taxed at higher GST rates primarily @ ;18% and 28% and since the rates of services are higher than the GST rate applicable to the outward supply of works contract services, provided by the Petitioner, there is an accumulation of Input Tax Credit (ITC). Accordingly this made the Petitioner entitled for refund of accumulated ITC as per provisions of Section 54(3)(ii) of the Central Goods and Service Tax Act, 2017 (`CGST Act’ for short). The Petitioner in such circumstance

An indispensable Tool for Legal Professionals, Endorsed by Various High Court and Judicial Officers

Please visit our Training & Support

Center or Contact Us for assistance

Scan Me!

India’s Legal research and Law Firm App, Download now!

For Daily Legal Updates, Join us on :