CUSTOMS EXCISE & SERVICE TAX APPELLATE TRIBUNAL

Sanjiv Srivastava, Technical Member

M/s Kunwar Bahadur Shri Kishan – Appellant

Versus

Commissioner of Central Excise – Respondent

FINAL ORDER NO.70005/2026

| Table of Content |

|---|

| 1. recovery and entries in diary are substantial evidence. (Para 1 , 2) |

SANJIV SRIVASTAVA:

This appeal is directed against Order-In-Appeal No. 250- 251-CE/LKO/2012 dated 30.05.2012. By the impugned order following has been held:

9. In the circumstances, I modify the impugned Order-in- Original No. 05-AC/FBD/CEX/12 dated 17/02/2012 passed by the Assistant Commissioner. Central Excise Division Farrukhabad to the extent that the penalty imposed upon Shri Ajay Gupta (Appellant No.2) under Rule 26 of the Central Excise Rules is set aside.

1.2 By the order in original dated 17.02.2012 following was held:

ORDER

1. I therefore,. confirm the demand of Basic Excise Duty of Rs 3,16,940/-, Additional Excise duty of Rs. 31,694/, Ed. Cess of Rs 6,973/- and S&H Cess of Rs. 3,486/- totaling to RS. 3,59,093/- involved on 1509.24 bags of 8 gms; under Section 11A of the Central Excise Act. 1944 alongwith interest under Section 11A B of the said Act. The amount so deposited by the party as Rs.25,000/-vide GAR-7 no. 18 dated 19.1.2010 against the said clandestine removal is hereby appropriated.

2. I further confirm the demand of BED of Rs. 94,507/-, Additional Excise duty of Rs. 9,451/-, Ed. Cess Rs. 2,079/- and S & H Cess of Rs. 1,040/- totaling to Rs, 1,07,077/- involved on 300.022 bags of Moni sada 14 gms under Section 11 -A of Central Excise Act, 1944 along with interest under Section 11 - AB read with Section 11 AA of the said Act. The amount deposited by the party as Rs. 25,000/- vide GAR-7 no. 20 dated 09.02.2010 against the said clandestine removal is hereby appropriated

3. I impose a penalty of Rs.4,66,170/- (Rupees four lacs sixty Six thousand one hundred seventy only ) on party No.1, M/s Kunwar Nagar, Kaimganj, Distt. Farrukhabad Bahadur Shri Kishan Prem under Rule 25 (b) of the Central Excise Rules, 2002 read with Section 11 -AC of the Central Excise Act, 1944 ;

4. I also impose personal penalty of Rs.4,66,170/- (Rupees four lacs sixty six thousand one hundred seventy only ) under Rule 26 on Shri Ajay Gupta, partner of the party M/S Kunwar Bahadur Shri Kishan Prem Nagar, Kaimganj, Distt. Farrukhabad.

2.1 Appellant is engaged in the production of Unmanufactured Branded Chewing Tobacco (UMBCT) of "Moni Sada brand falling under Chapter Sub heading No. 2401 1090 of the Central Excise Tariff Act 1985.

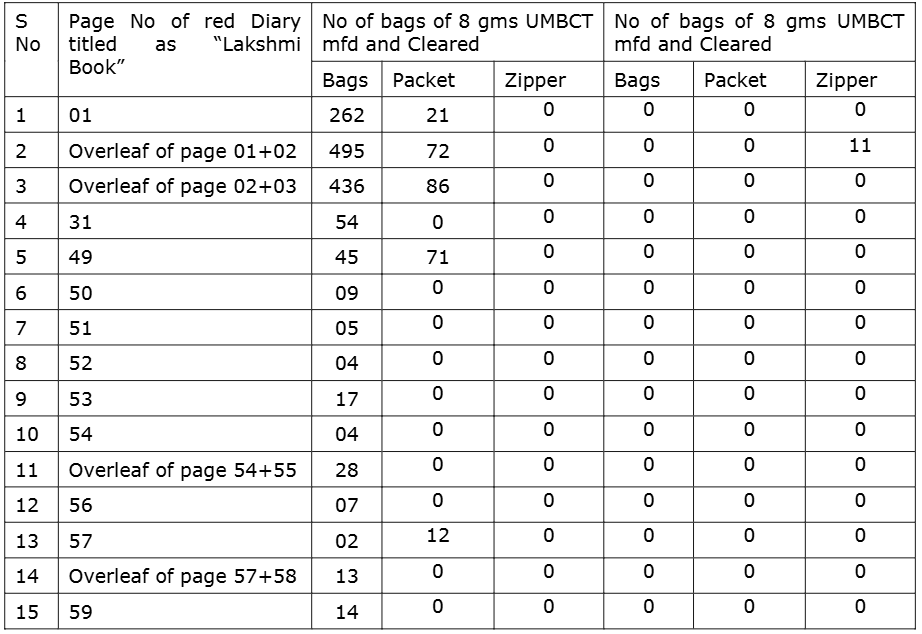

2.2 On 11/01/2010, during the course of checking of the premises of appellant No. 1, the Departmental officers recovered one red coloured diary titled as "LAKSHMI BOOK" having 68 pages, containing details of UMBCT manufactured and cleared. On scrutiny of the "LAKSHMI BOOK", same was found containing records of clearance and sale of bags and pouches of "Moni sada” UMBCT of 8 gms each and "Moni sada" UMBCT of 14 gms each by the appellant party to various purchasers without making entries of the same in their statutory records and clearing the same without issuing invoices and without payment of duty. On detailed scrutiny, it was found that the appellant No. 1 had manufactured 1502 bags + 262 packets of Moni sada UMBCT of 8 gms each (total value Rs 7,53,620/-) and 300 bags + 11 zipper pouches (total value Rs 2,25.000/-) of Moni sada UMBCT of 14 gms each without making entries in respect of the same in their statutory records and clearing the same without payment of duty. The details as available in the said dairy are reproduced below:

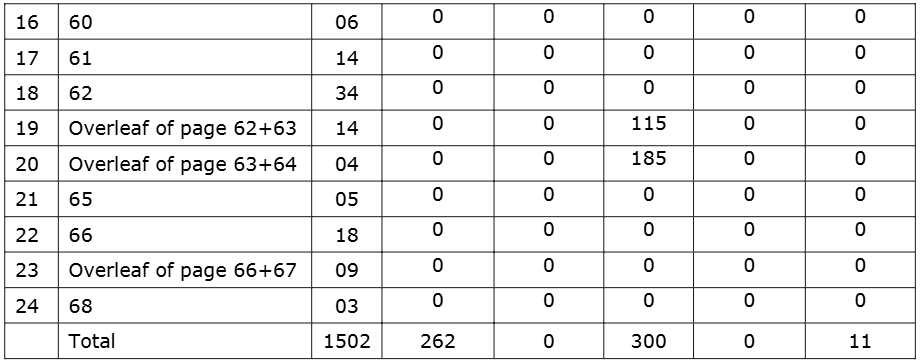

2.3 The diary also contained the details of the purchasers and payments received as detailed in table below:

2.4 Shri Ajay Gupta, Partner in his statement dated 11/01/2010 recorded on the spot under section 14 of the Central Excise Act 1944, admitted the recovery of the above diary from his factory. He further admitted packing of 300 bags, each containing 14 gms "Moni sada" UMBCT, during the period from October 2009 to January 2010 without making proper entry in the statutory records and subsequently removing the same clandestinely without payment of Central Excise duty the appellant party deposited Rs 25

An indispensable Tool for Legal Professionals, Endorsed by Various High Court and Judicial Officers

Please visit our Training & Support

Center or Contact Us for assistance

Scan Me!

India’s Legal research and Law Firm App, Download now!

For Daily Legal Updates, Join us on :