CUSTOMS EXCISE & SERVICE TAX APPELLATE TRIBUNAL

ASHOK JINDAL, J, K. ANPAZHAKAN, Technical Member

M/s. Jindal Steel & Power Limited – Appellant

Versus

Commissioner of Central Tax, G.S.T. and C.X. – Respondent

ORDER: [PER SHRI ASHOK JINDAL]

The appellant is in appeal against the impugned order wherein central excise duty amounting to Rs.333,22,45,002/-, along with interest, has been demanded and penalty thereon under Section 11AC of the Central Excise Act, 1944 read with Rule 25 of the Central Excise Rules, 2002 has been imposed.

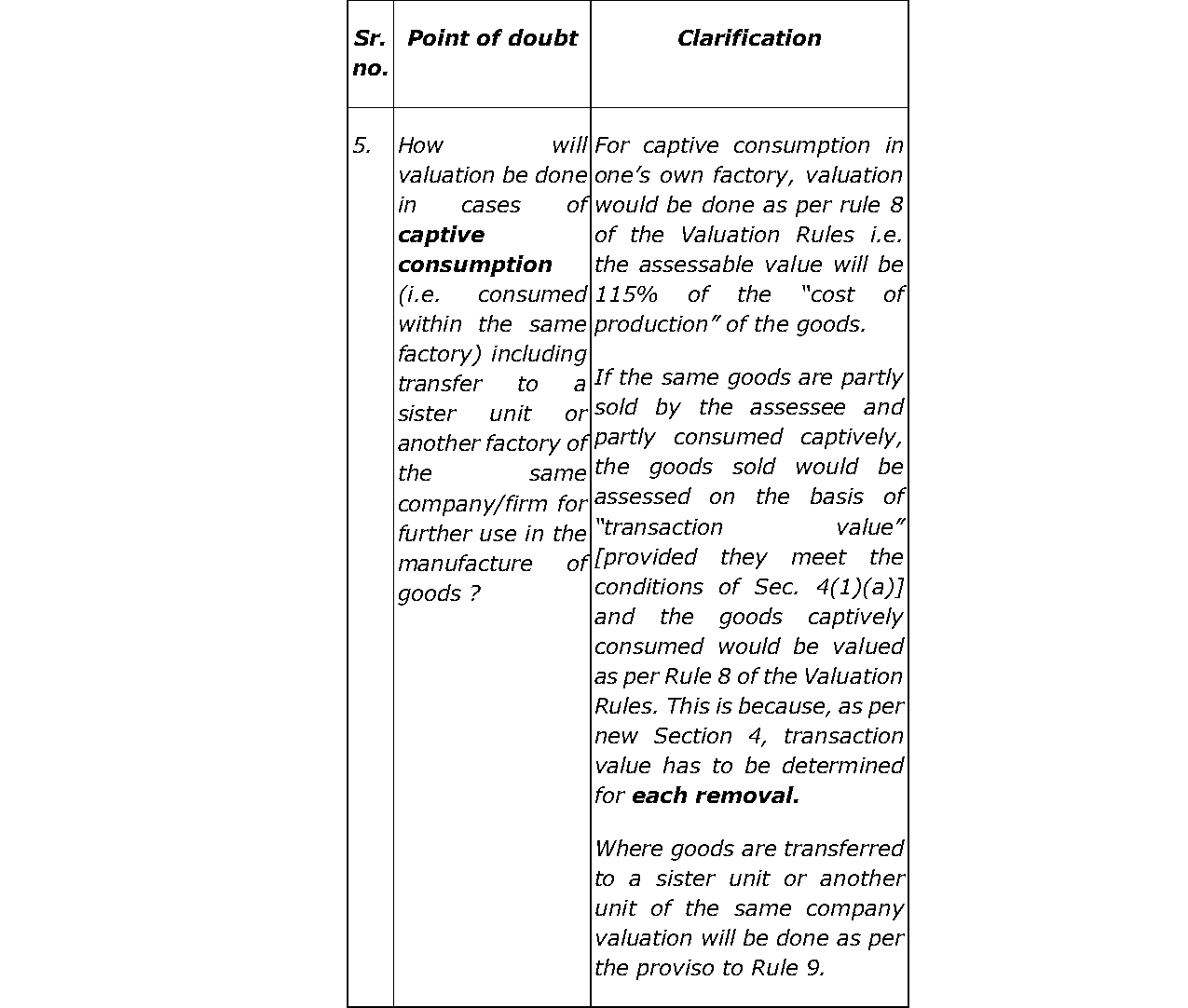

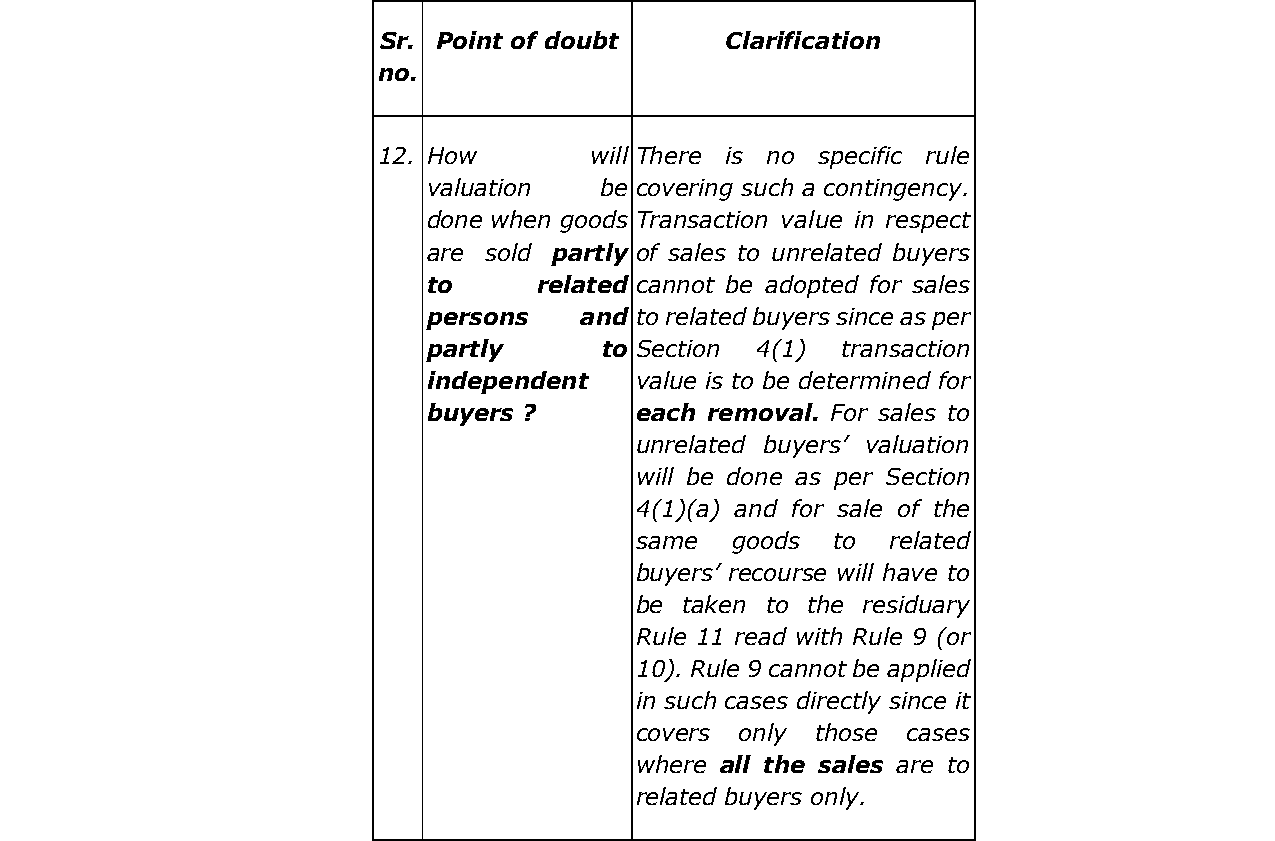

2. The brief facts of the case are that M/s. Jindal Steel & Power Ltd. (‘JSPL’), Barbil Unit, the appellant before us, is engaged in the manufacture of iron ore pellets falling under Chapter 26 of the Central Excise Tariff Act, 1985, (‘CETA’). The pellets manufactured by the appellant are primarily cleared to its own manufacturing units located at Angul, in the State of Odisha and Raigarh, in the State of Chhattisgarh, for captive consumption. The appellant also sells iron ore pellets to independent third-party buyers.

2.1. With regard to the clearances made by the appellant to its own units for captive consumption, during the period in dispute, the excise duty was paid on the value determined in terms of Rule 8 of the Central Excise Valuation (Determination of Price of Excisable Goods) Rules, 2000 (hereinafter referred to as “Valuation Rules”) i.e., on the basis

An indispensable Tool for Legal Professionals, Endorsed by Various High Court and Judicial Officers

Please visit our Training & Support

Center or Contact Us for assistance

Scan Me!

India’s Legal research and Law Firm App, Download now!

For Daily Legal Updates, Join us on :