CUSTOMS EXCISE & SERVICE TAX APPELLATE TRIBUNAL

Binu Tamta, Member (Judicial), Hemambika R. Priya, Member (Technical)

Amazon Internet Services Pvt.Ltd. – Appellant

Versus

Commissioner of CGST (East) – Respondent

| Table of Content |

|---|

| 1. understanding the conditions of the appellant's service. (Para 1 , 2 , 3 , 4 , 5) |

| 2. appellant's argument that it is not an intermediary. (Para 6 , 7 , 8 , 9 , 10) |

| 3. court's reasoning on intermediary definition. (Para 11 , 12 , 13 , 14 , 15 , 16 , 17 , 18 , 19 , 20) |

| 4. examination of intermediary criteria and application. (Para 21 , 22 , 23 , 24 , 25 , 26 , 27) |

| 5. determining service tax liability and remand factors. (Para 28 , 29) |

| 6. final order and conclusion of the appeal. (Para 31) |

BINU TAMTA:

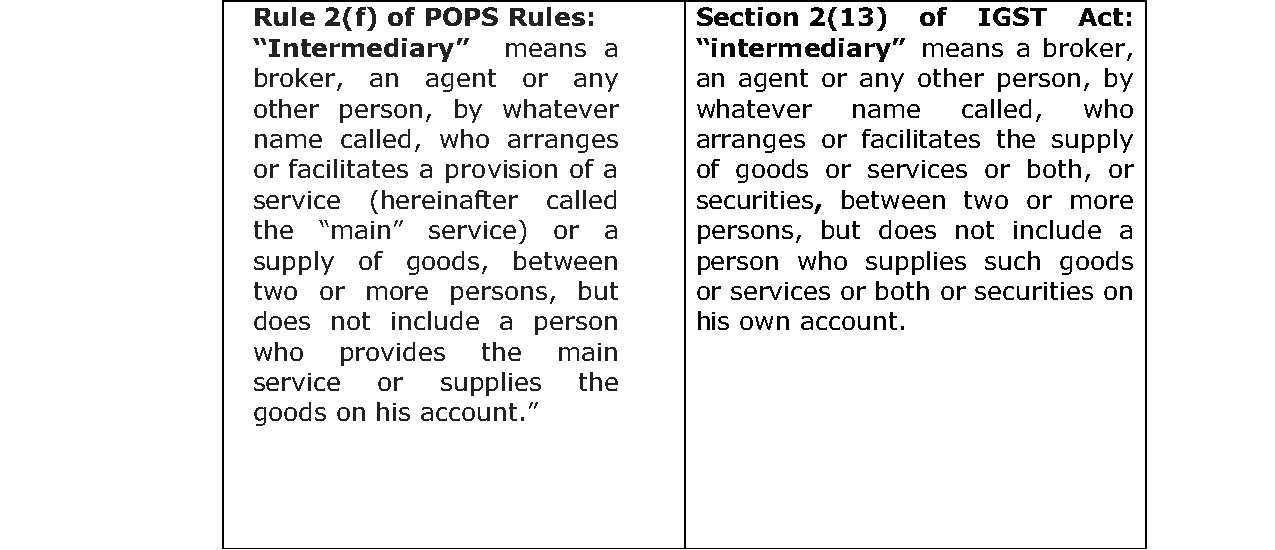

1. Challenge in the present appeal is to the Order-in-Original No.183-184/Commr./Delhi East/AP/2022-23 dated 10.03.2023, whereby the demand raised in the two show cause notices was upheld on the ground that the appellant is covered under the definition of „intermediary‟ under Rule 2(f) of Place of Provision of Service Rules, 2012, POPS Rules

2. Amazon Internet Services Pvt. Ltd., The Appellant is engaged in providing data hosting services and marketing services to Amazon Web Services, Inc. USA, AWSI under the Data Services Agreement, DSA and Marketing Services Agreement dated 1.07.2013. The data hosting services entail the management, operation and maintenance of data centres.

An indispensable Tool for Legal Professionals, Endorsed by Various High Court and Judicial Officers

Please visit our Training & Support

Center or Contact Us for assistance

Scan Me!

India’s Legal research and Law Firm App, Download now!

For Daily Legal Updates, Join us on :