CUSTOMS EXCISE & SERVICE TAX APPELLATE TRIBUNAL

Ashok Jindal, J, K. Anpazhakan, Technical Member

M/s. Nanu Shome & Co. – Appellant

Versus

Commissioner of C.G.S.T. and Central Excise – Respondent

| Table of Content |

|---|

| 1. nature of appellant's services (Para 2) |

| 2. arguments for service tax exemption based on notifications (Para 4 , 5) |

| 3. need for independent verification for tax demands (Para 8) |

| 4. procedural requirements affecting service tax notices (Para 9) |

| 5. final decision and implications for tax demand (Para 11) |

ORDER:

[PER SHRI K. ANPAZHAKAN]

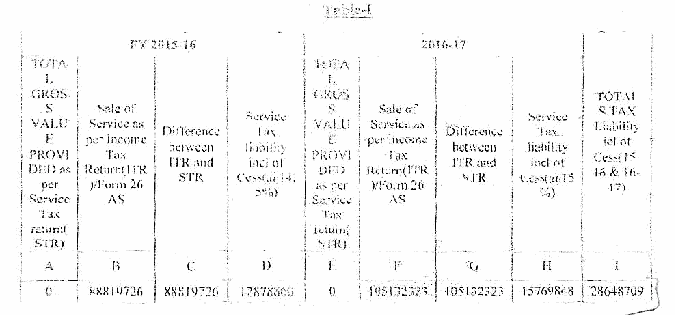

The present appeal has been filed challenging the Order-in-Original No. 60/COMM/ST/SLG/23-24 dated 28.03.2024 passed by the Commissioner, Siliguri Central Excise and C.G.S.T. Commissionerate wherein the demand of Service Tax amounting to Rs.2,86,48,709/- (inclusive of cesses) for the period from April 2015 to March 2017 has been confirmed, along with interest. A penalty equal to the above Service Tax demand confirmed has also been imposed by the ld. adjudicating authority under Section 78 of the Finance Act, 1994 ; penalty of Rs.10,000/- under Section 77 (1)(c) of the Act and late fee of Rs.80,000/- on account of non-filing of ST-3 Returns under Section 70 of the Act read with Rule 7(C) of the Service Tax Rules, 1994 have also been imposed.

2. The facts of the case are that M/s. Nanu Shome & Co. (hereinafter referred to as the “appellant”)

An indispensable Tool for Legal Professionals, Endorsed by Various High Court and Judicial Officers

Please visit our Training & Support

Center or Contact Us for assistance

Scan Me!

India’s Legal research and Law Firm App, Download now!

For Daily Legal Updates, Join us on :