CUSTOMS EXCISE & SERVICE TAX APPELLATE TRIBUNAL

Ashok Jindal, J, K. Anpazhakan, Technical Member

M/s The Mining & Engineering Corporation – Appellant

Versus

Commissioner of CGST & Central Excise, Kolkata – Respondent

ST/77057/2016

| Table of Content |

|---|

| 1. facts of tax demand and penalties (Para 1 , 2) |

| 2. arguments against service tax liability (Para 3) |

| 3. court's observations on service tax applicability (Para 4 , 5 , 6 , 7) |

| 4. decision on supply of tangible goods and service tax (Para 8 , 9 , 10 , 11 , 12) |

Per Ashok Jindal :

The appellant is in appeal against the impugned order wherein the demand of service tax along with interest has been confirmed and an equivalent amount of penalty has been imposed on the appellant.

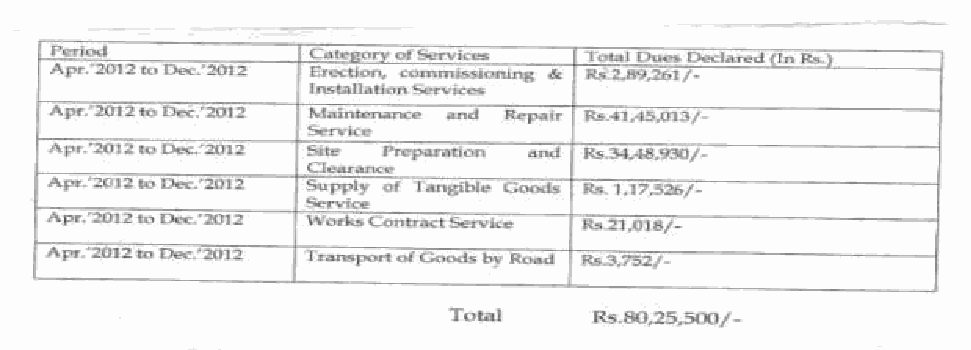

2. The brief facts of the case are that the appellant has obtained service tax registration from the Service Tax Authorities for providing services under the category of “Erection, Commissioning & Installation”, “Site Preparation and Clearance”, “Supply of Tangible Goods for Use Services”, “Works Contract Services”, “Transport of Goods by Road”, “Maintenance or Repair Services”, “Construction Services in respect of Commercial or Industrial Building and Civil Structures” etc.. For the said services, the appellant filed a declaration under Sub-section (1) of Section 107 of the Finance Act , 2013 read with Rule 4 of the Service Tax Voluntary Compliance Encouragement Rules, 2013 in Form VCES-I dated 24.12.2013, which was received by the VCES Cell under declaration No.KOL1125 dated 24.12.2013, wherein they declared tax dues as under :

2.1 On scrutiny of documents and records submitted by the appellant, it appears that the above mentioned declaration dated 24.12.2013, made in Form VCES-1 under Service Tax Voluntary Compliance Encouragement Scheme, 2013 is substantially false in as much as the appellant had 'tax dues' amounting to Rs.1,28,28,267/- only for the period from 01.10.2007 to 31.12.2012.

2.2 The appellant filed a VCES declaration on 24.12.2013, whereas investigation by the Department was started much earlier i.e., on 21.12.2012 on the basis of intelligence gathered by SIV to the effect that one party named and styled as M/s. The Mining & Engineering Corporation, DD House, P-32, Kasba Industrial Estate, Phase-I, Kolkata 700 107 holder of service tax registration bearing No. AABCV2600BST001 on 25.07.2007 under the category of Supply of Tangible Goods for Use Services', classifiable under Section 65 (105)(zzzzj) of the Finance Act , 1994, as amended, were providing taxable services to their clients, but were not paying service tax properly on the gross amounts received by them under the category "Supply of Tangible Goods for Use Services'.

2.3 Accordingly, a Letter dated 20.08.2013 under Rule 5A(1) of Service Tax Rules' had been issued to them for verification of documents and records. Subsequently, the appellant submitted Balance Sheets and Profit and Loss Account and reconciliation sheets etc. for the period 2007-08 to 2012-13 etc.. The appellants have income in the name of 'Hire Sale', 'Hire Sale (interstate)', 'Hire Sale (local)' for the period 2007-08 (Oct-Mar.) to 2012-13 (Apr.-Dec.). The party has submitted work orders/purchase orders, invoices and ledgers for the year 2010-11 and 2011-12 through their letter dated 18 11 2014.

2.4. On scrutiny of the above documents/records submitted by the appellants, it seems that the appellant is providing site analyser machines on hire as is evident from invoices no.MEC/Laying/2011- 12/171 dated 01.08.2011 [RUD-11] MEC/Laying/2011-12/173 dated 02.08.2011[RUD-12], MEC/Laying/2010-11/468 dated 31.03.2011 [RUD-13] and wherein it is seen that machines bearing serial no. 100400309, 100700320, 100700321, 101600277 have been given on hire to same/different companies on different dates. This cannot be construed as 'Sale' and clearly comes under the category of Supply of Tangible Goods for Use Services'. The appellants have paid VAT but it is nothing but camouflage stance. A single machine cannot be sold to different buyers on different dates by the same supplier. It is also seen that the actual ownership has not been transferred to the receiver.

2.5. Hence, 'tax dues' of the said appellant, as quantified on the bas

An indispensable Tool for Legal Professionals, Endorsed by Various High Court and Judicial Officers

Please visit our Training & Support

Center or Contact Us for assistance

Scan Me!

India’s Legal research and Law Firm App, Download now!

For Daily Legal Updates, Join us on :