CUSTOMS EXCISE & SERVICE TAX APPELLATE TRIBUNAL

M. Ajit Kumar, Technical Member, Ajayan T.V., Judicial Member

Nagarjuna Hospital Ltd. – Appellant

Versus

Commissioner of Customs (General) – Respondent

| Table of Content |

|---|

| 1. classification and tariff implications (Para 2 , 3 , 4) |

| 2. provisions for time limits on customs actions (Para 5 , 6 , 11) |

| 3. critique of misclassification arguments (Para 8 , 12 , 18) |

| 4. final outcome related to procedural adherence. (Para 19 , 20) |

Per M. Ajit Kumar,

This appeal is filed by the appellant against Order in Original No. 65701/2018 dated 17.10.2018 passed by the Commissioner of Customs, (General), Chennai (impugned order).

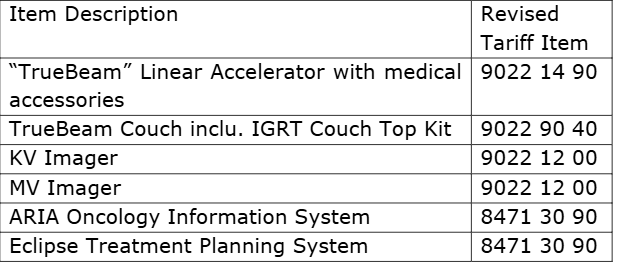

2. Brief facts of the case are that the appellant cleared medical equipment described as 'True Beam' Linear Accelerator under two Bills of Entry (BE), dated 18.03.2016, claiming duty exemption under Customs Notifications No. 012/2012 (Sl. No. 473) and 021/2012 (Sl. No. 95). The BE’s were assessed finally, without resorting to provisional assessment as was prescribed under Public Notice No.91/87 for the goods supplied against contract in multiple shipments. Investigation allegedly revealed that the appellant divided the goods into 15 sections and although in the invoices, the HS Code for the goods was mentioned as 9022 1400, the appellant, deliberately declared the goods as ‘Radiation Beam Delivery Unit / Equipment’ under Tariff Heading

An indispensable Tool for Legal Professionals, Endorsed by Various High Court and Judicial Officers

Please visit our Training & Support

Center or Contact Us for assistance

Scan Me!

India’s Legal research and Law Firm App, Download now!

For Daily Legal Updates, Join us on :