INCOME TAX APPELLATE TRIBUNAL (BANGALORE BENCH)

SHRI CHANDRA POOJARI, ACJ, SHRI KESHAV DUBEY, J

MKH Infrastructure – Appellant

Versus

Income Tax Department – Respondent

ORDER

PER CHANDRA POOJARI, ACCOUNTANT MEMBER:

These appeals are emanated from different orders of CIT(A) for the assessment years 2017-18 & 2018-19 in case of above three assessees.

ITA Nos.414 & 415/Bang/2024 (AY 2017-18 & 2018-19)

Emirates Hindustan Builders and Developers:

2. First, we will take ITA Nos.414 & 415/Bang/2024, wherein certain issues are common except figures, hence these are clubbed together, heard together and disposed of by this common order for the sake of convenience. In this appeal the assessee has raised following grounds of appeal in ITA No.414/Bang/2024:

1. “The ld. CIT(A) erred in passing the order in the manner he did.

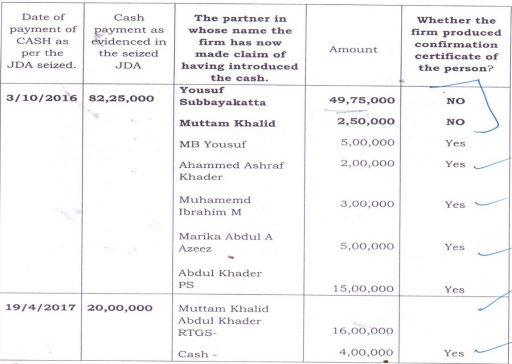

2. The ld. CIT(A) further erred in confirming the addition u/s 68 of the Income Tax Act, 1961 without appreciating the submission of the appellant.

3. The ld. CIT(A) further erred in confirming the order of assessing officer by merely relying on sworn statement of the partner without any incriminating material having being found.

4. The ld. CIT(A) further erred in not appreciating that return in response to notice u/s 148 was filed only on 4.1.2019 and hence the assessment was time barred.

5. The ld. CIT(A) further erred in assessing the income u/s

An indispensable Tool for Legal Professionals, Endorsed by Various High Court and Judicial Officers

Please visit our Training & Support

Center or Contact Us for assistance

Scan Me!

India’s Legal research and Law Firm App, Download now!

For Daily Legal Updates, Join us on :