INCOME TAX APPELLATE TRIBUNAL (GUWAHATI BENCH)

SHRI SANJAY GARG, J, SHRI GIRISH AGRAWAL, ACJ

Assistant Commissioner of Income-tax, Circle-2, Guwahati – Appellant

Versus

Front Line Vyapar Private Limited – Respondent

| Table of Content |

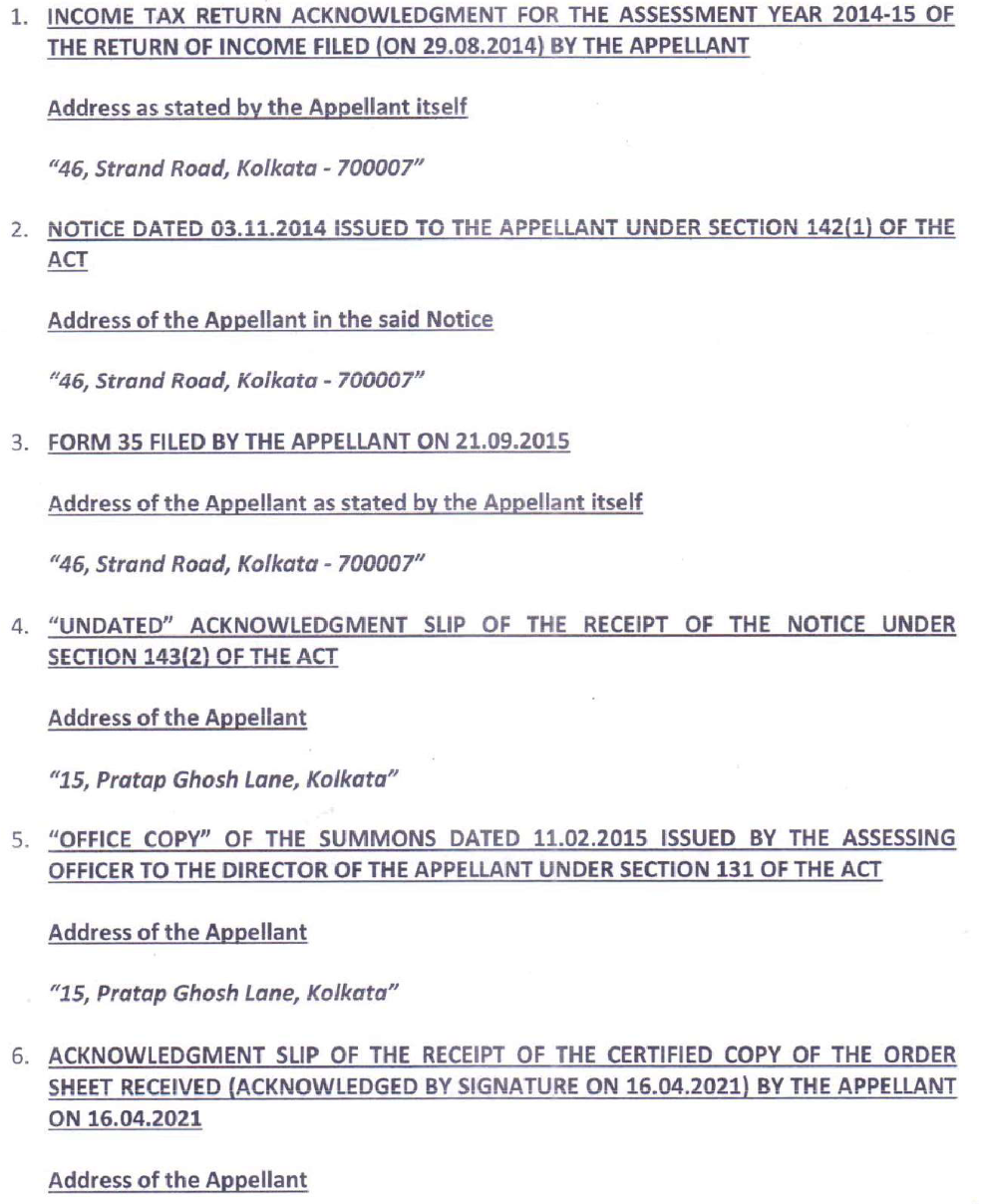

|---|

| 1. failure to establish genuineness of the share premium raised. (Para 3 , 4 , 5) |

| 2. determination of proper jurisdiction and venue for appeal. (Para 6 , 7 , 8) |

| 3. final decision dismissed for incorrect filing jurisdiction. (Para 9) |

ORDER

PER GIRISH AGRAWAL, ACCOUNTANT MEMBER:

Appeal filed by the revenue is against the order of Ld. CIT(A), Central NER, Guwahati dated 27.01.2023 passed against the assessment order by ITO, Ward-9(2), Kolkata u/s. 143(3) of the Income-tax Act, 1961 (hereinafter referred to as the “Act”), dated 23.03.2015 for AY 2012-13 .

2. Grounds raised by the revenue are reproduced as under:

Under sub-section 2 of section 253 of the Income Tax Act, 1961 , I, hereby direct the Assessing Officer holding jurisdiction over the case of Frontline Vyapar Pvt. Ltd., (PAN- AABCF8058R), A.Y.2012-13, to file appeal before the Income Tax Appellate Tribunal, Guwahati Bench, Guwahati against the order passed by the Lei. CIT (A), Central NER, Guwahati/l0014/2013-14 dtd 30.12.2022 on the grounds mentioned below:-

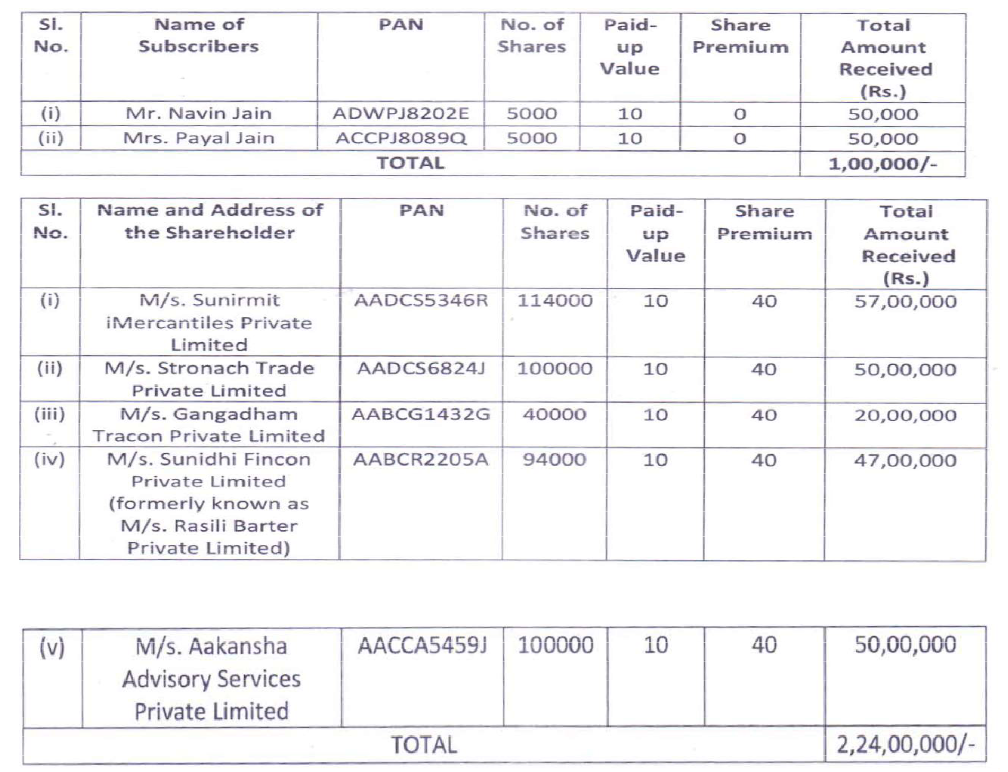

1. Whether on the facts and circumstances of the case, the Ld. CIT(A) has erred in deleting the addition to the tune of Rs.2,25,00,000/- under the head of unexpl

An indispensable Tool for Legal Professionals, Endorsed by Various High Court and Judicial Officers

Please visit our Training & Support

Center or Contact Us for assistance

Scan Me!

India’s Legal research and Law Firm App, Download now!

For Daily Legal Updates, Join us on :