INCOME TAX APPELLATE TRIBUNAL (DELHI BENCH)

Shri Anubhav Sharma, J, Shri Brajesh Kumar Singh, ACJ

MONICA CAPOOR GURGAON – Appellant

Versus

ITO-WARD - 2(4) GURGAON – Respondent

| Table of Content |

|---|

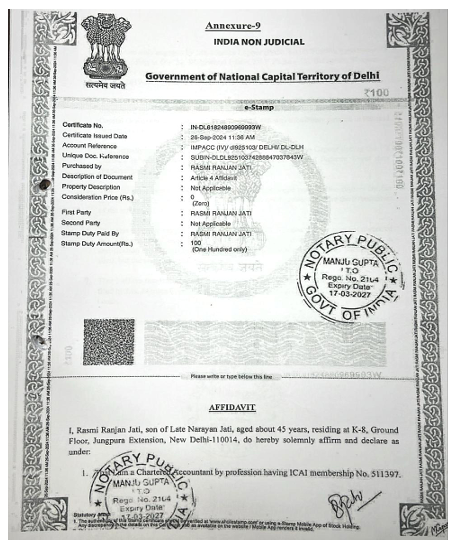

| 1. typographical error explanation (Para 3) |

| 2. cit(a) dismissal of appeal (Para 4 , 5 , 6 , 7 , 8 , 9) |

ORDER

PER BRAJESH KUMAR SINGH, AM,

This appeal filed by the assessee is directed against the order dated 29.07.2024 of the National Faceless Appeal Centre (NFAC)/Ld. Commissioner of Income Tax (Appeals), Delhi, relating to Assessment Year 2020-21, arising out of order dated 22.06.2023 passed by the Income Tax Officer, Ward-2(4), Gurgaon, under section 154 of the Income Tax Act, 1961 (hereinafter referred as ‘the Act’).

2. The grounds of appeal raised by the assessee are as under:-

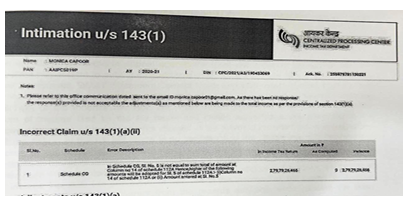

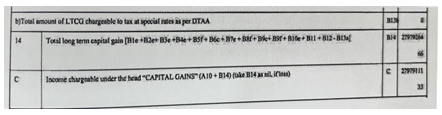

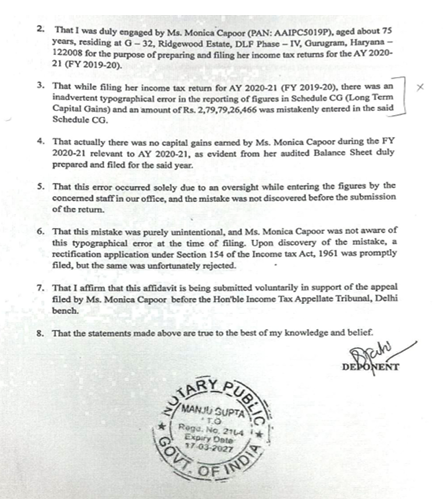

1. The Ld. CIT(A) has erred in law and on facts in upholding the erroneous adjustment made by the CPC under Section 143(1), which incorrectly computed an LTCG of Rs.2,79,68,49,392/-, based on a typographical error in Schedule CG of the return of income filed by the office of the appellant's CA.

2. The Ld. CIT(A) has failed to appreciate that the mistake in reporting Rs.2,79,79,26,466/- in Schedule CG was a bona fide typographical error made by the office of the appeltant's CA while filing the return of income. The mistake was clearly explained and demonstrated in the rectification applications

An indispensable Tool for Legal Professionals, Endorsed by Various High Court and Judicial Officers

Please visit our Training & Support

Center or Contact Us for assistance

Scan Me!

India’s Legal research and Law Firm App, Download now!

For Daily Legal Updates, Join us on :