INCOME TAX APPELLATE TRIBUNAL (MUMBAI BENCH)

Sandeep Gosain, JM, Girish Agrawal, AM

Income Tax Department – Appellant

Versus

Shri Vimal Punmiya – Respondent

| Table of Content |

|---|

| 1. the appeal concerns the deletion of additions related to long-term capital gains arising from penny stock transactions. (Para 1 , 2 , 3) |

| 2. the evidence presented supports the respondent's claim, emphasizing the legitimacy of the reported gains. (Para 4 , 5 , 6) |

| 3. the revenue's arguments based on hearsay and third-party information lack substantiation. (Para 7 , 8 , 9 , 10) |

| 4. the court finds that the documentation provided establishes the transactions as genuine. (Para 11 , 12 , 13) |

| 5. the cit(a) rightly allowed the exemption under section 10(38), and the appeal is dismissed. (Para 14 , 15) |

ORDER

PER SANDEEP GOSAIN, JM:

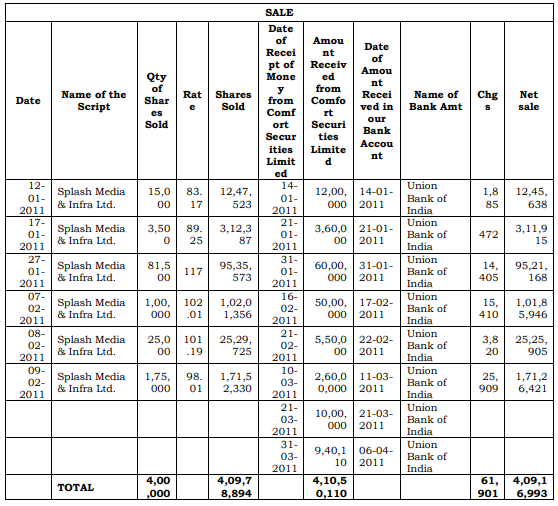

The present appeal has been filed by the revenue challenging the impugned order dt. 22.01.2025 passed u/s 263 of the Income Tax Act, 1961 (‘the Act’), by the National Faceless Appeal Centre, Delhi (NFAC) for the assessment year 2011-12.

2. All the ground raised by the revenue are interrelated and interconnected and relates to challenging the order of Ld. CIT(A) in deleting the additions made u/s 68 of the Act. Therefore we have decided to adjudicate the same through the present consolidated order.

3. Ld. DR appearing on behalf of the revenue while rel

An indispensable Tool for Legal Professionals, Endorsed by Various High Court and Judicial Officers

Please visit our Training & Support

Center or Contact Us for assistance

Scan Me!

India’s Legal research and Law Firm App, Download now!

For Daily Legal Updates, Join us on :