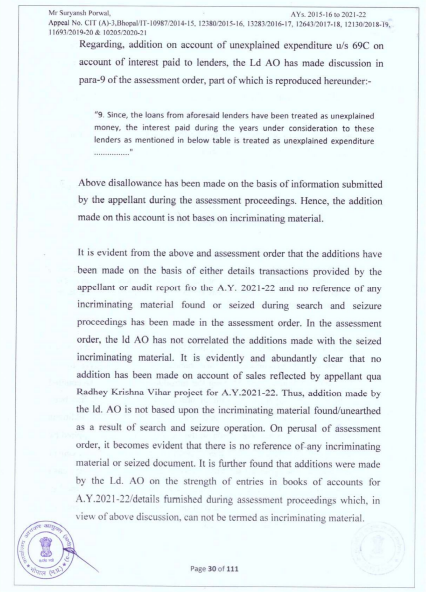

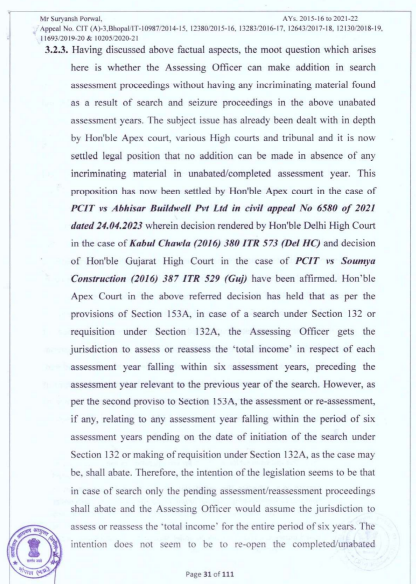

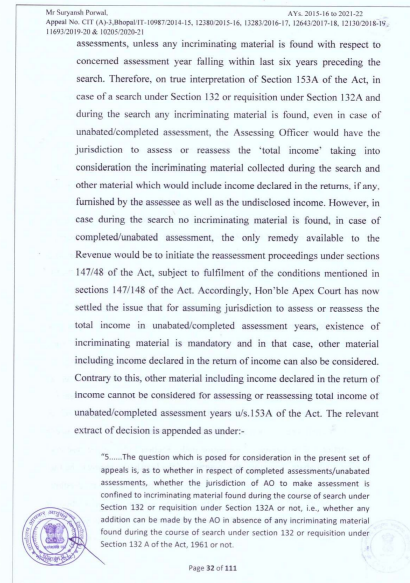

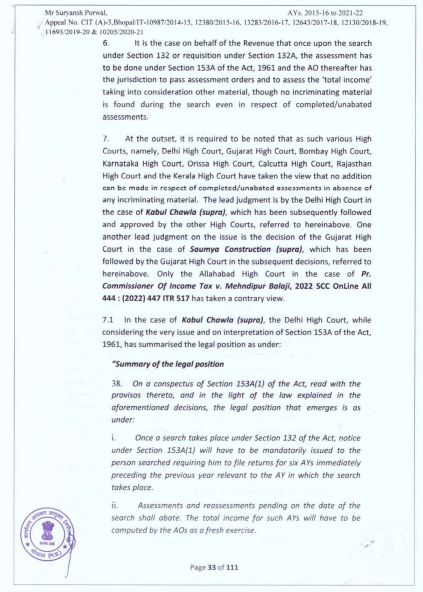

INCOME TAX APPELLATE TRIBUNAL (INDORE BENCH)

B.M. BIYANI, AM, PARESH M. JOSHI, JM

DCIT, Central, Circle -1 Indore – Appellant

Versus

Suryaansh Porwal – Respondent

आदेश/ORDER

Per Bench:

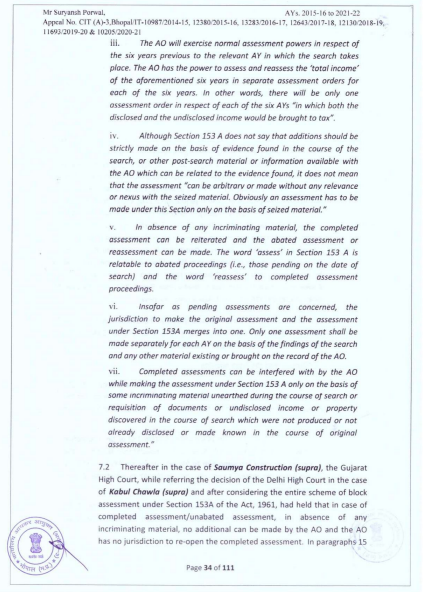

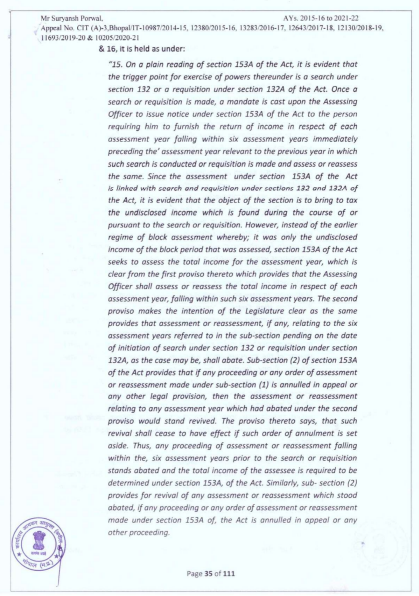

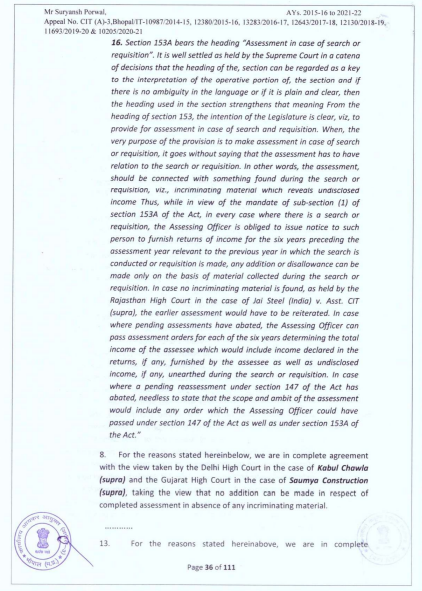

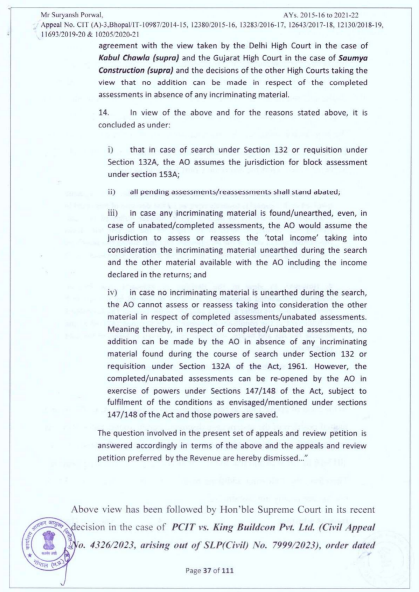

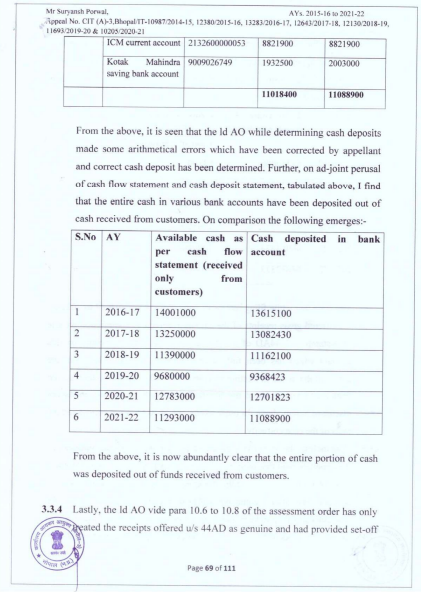

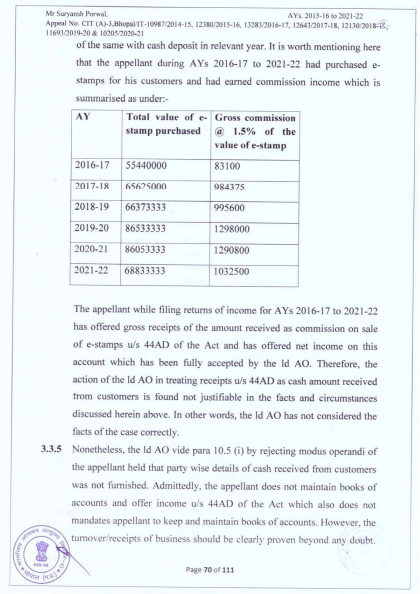

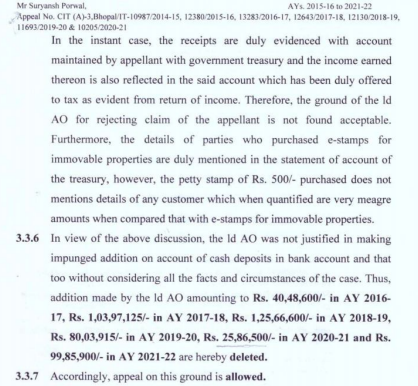

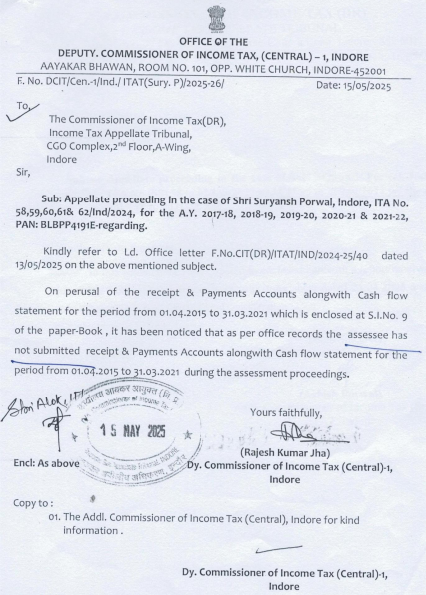

The captioned five (5) appeals are filed by revenue against a consolidated order of first-appeal dated 11.08.2023 passed by learned Commissioner of Income-tax (Appeals)-3, Bhopal [“CIT(A)”], which in turn arises out of a consolidated assessment-order dated 08.09.2022 passed by ACIT (Central)- 1, Indore [“AO”] u/ s 153A/ 143(3) of the Income-tax Act, 1961 [“the Act”] for five Assessment-Years [“AY”] 2017-18 to 2021-22.

-

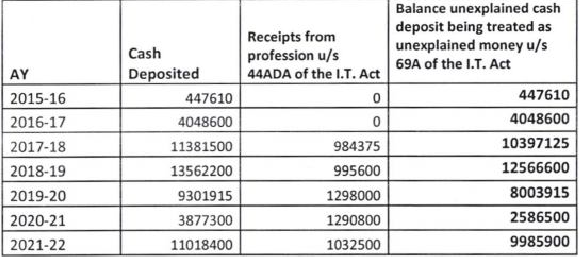

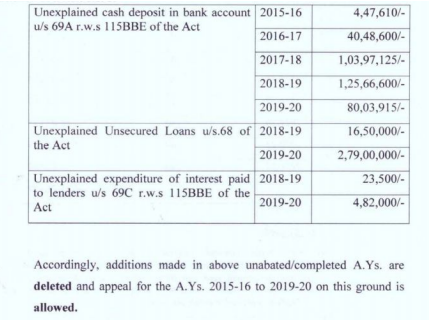

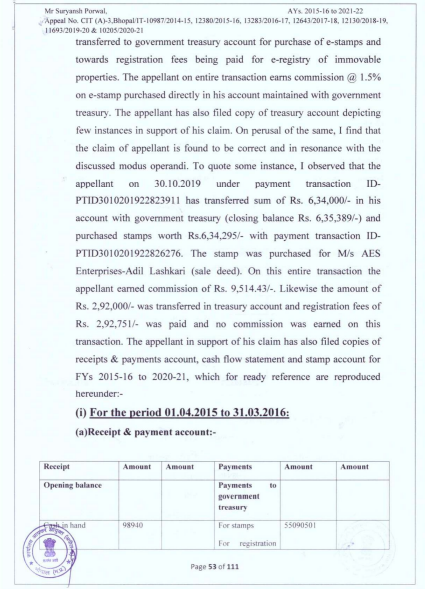

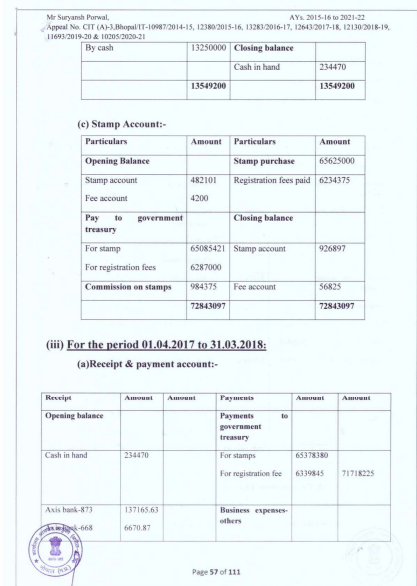

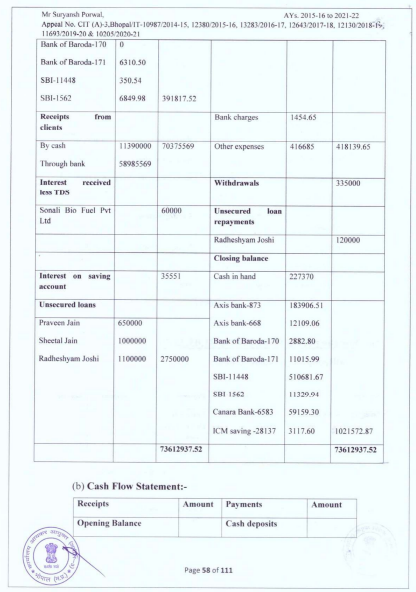

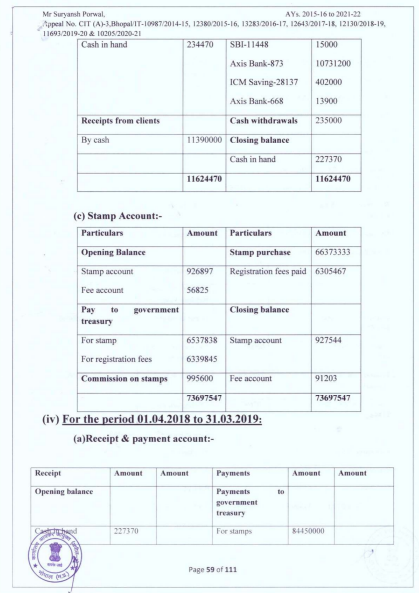

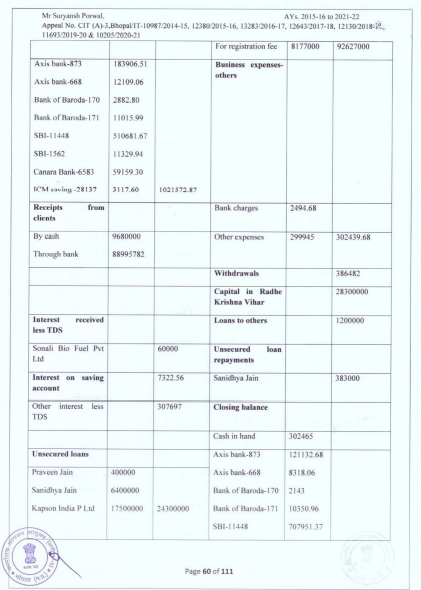

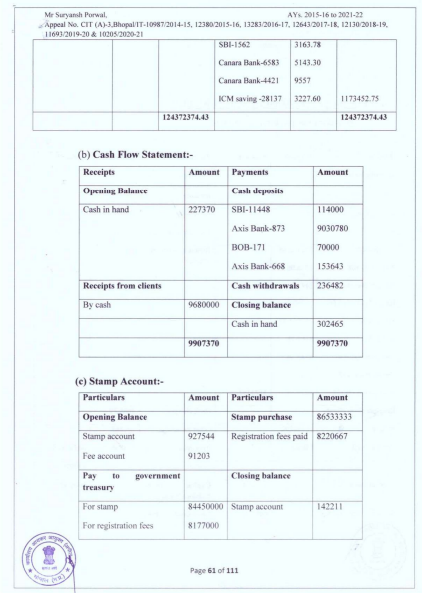

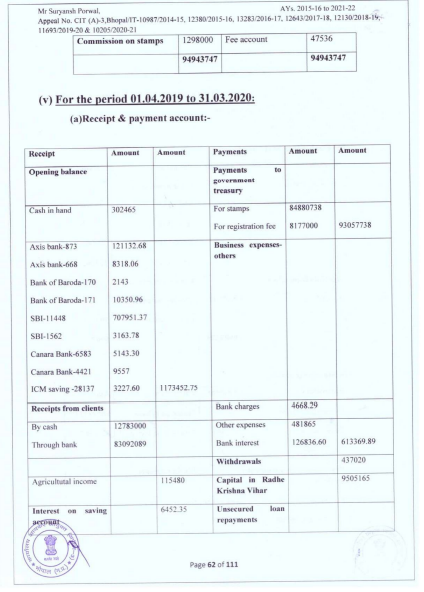

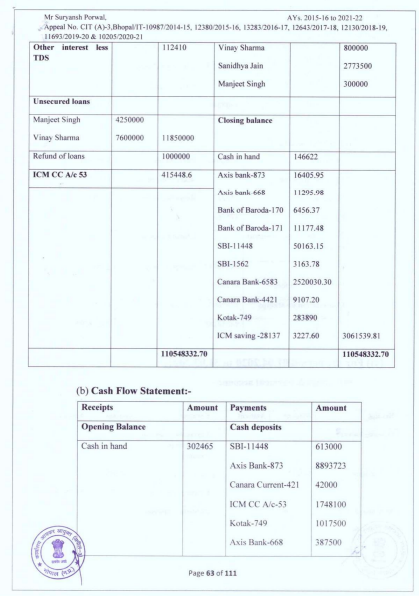

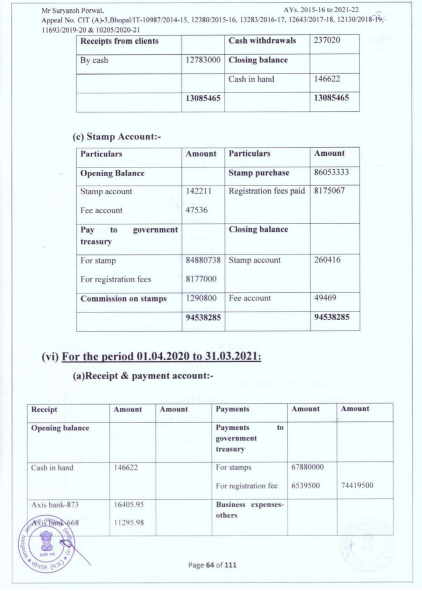

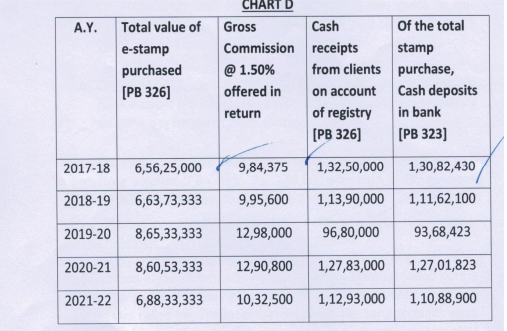

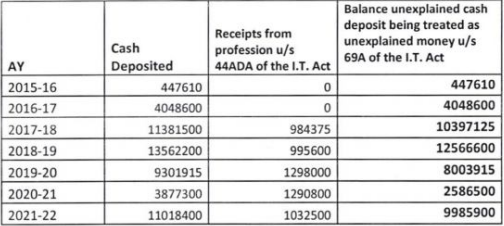

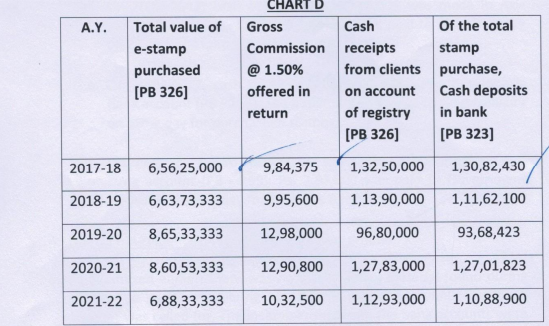

2. The background facts leading to present appeals are such that the assessee is an individual deriving income from business and profession, interest and other sources. A search u/ s 132 was conducted upon “JRG Group” including assessee on 12.01.2021. Pursuant to search proceeding, the assessments of assessee were framed for six preceding AYs 2015-16 to 2020-21 u/ s 153A/ 143(3) and for current AY 2021-22 u/ s 143(3). Presently, in these five appeals, we are concerned with AYs 2017-18 to 2021-22 for which the AO made assessments after making certain additions as under:

| Natu re of addition | AY 2017-18 | 2018-19 | 2019-20 | 2020-21 | 2021-22 | |

| 1 | Unexplain ed deposi ts in Ban k A/ cs | 1,03,97,125 | 1,25,66,600 | 80,03,915 | 25,86,500 | 99,85,900 |

| 2 | Unexplain ed cash credit s | -- | 16,50,000 | 2 | ||

An indispensable Tool for Legal Professionals, Endorsed by Various High Court and Judicial Officers

Please visit our Training & Support

Center or Contact Us for assistance

Scan Me!

India’s Legal research and Law Firm App, Download now!

For Daily Legal Updates, Join us on :