INCOME TAX APPELLATE TRIBUNAL (MUMBAI BENCH)

C V BHADANG, CJ

Assessee – Appellant

Versus

Revenue – Respondent

ORDER

Per Padmavathy S, AM:

These cross appeals by the assessee and the revenue are against the separate orders of the Commissioner of Income Tax (Appeals)-4, Mumbai [In short 'CIT(A)'] passed under section 250 of the Income Tax Act, 1961 (the Act) dated 14.03.2013 for AY 2009-10, dated 07.09.2015 for AY 2011-12, dated 04.09.2015 for AY 2010- 11.

AY 2009-10 ITA

No. 4172/Mum/2013

2. The assessee is a company engaged in the business of manufacturing of Fans, Telecommunication, Transmission Line Towers, Hot Dip Galvanizing and trading in electrical appliances, Lamps, Lighting, engineering and project services and generation of wind energy. The assessee filed the return of income for AY 2009-10 on 30.09.2009 declaring a total income of Rs. 144,68,01,374/-. Subsequently the assessee filed a revised return of income on 08.02.2010 and also second time on 30.03.2011 declaring total income of Rs. 160,06,53,482/- and Rs. 145,57,22,635/- respectively. The assessee's case was selected for scrutiny and the statutory notices were duly served on the assessee. The Assessing Officer (AO) completed the assessment by making the following disallowance:

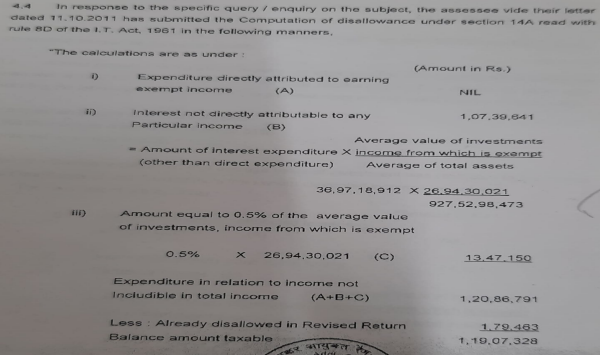

(i) Disallowance under section 14A r.w.r. 8D - Rs.

An indispensable Tool for Legal Professionals, Endorsed by Various High Court and Judicial Officers

Please visit our Training & Support

Center or Contact Us for assistance

Scan Me!

India’s Legal research and Law Firm App, Download now!

For Daily Legal Updates, Join us on :