INCOME TAX APPELLATE TRIBUNAL (JAIPUR BENCH)

RATHOD KAMLESH JAYANTBHAI, J

M/s Shivcharanlal Satyanarayan – Appellant

Versus

National Faceless Assessment Unit – Respondent

Income Tax Appeal | 2024

| Table of Content |

|---|

| 1. facts surrounding the assessee's appeal (Para 1 , 3) |

| 2. arguments challenging the assessment order (Para 2 , 4 , 6) |

| 3. observations made by the learned cit(a) (Para 7 , 8) |

| 4. final ruling on the validity of the assessment (Para 9 , 17) |

| 5. court's analysis on the invocation of provisions (Para 10 , 12) |

ORDER

PER: RATHOD KAMLESH JAYANTBHAI, AM

In this appeal the above-named assessee challenges the order of the learned National Faceless Appeal Centre, Delhi dated 03/10/2024 [ for short CIT(A)] which relates to the assessment year 2021-22. The said order of the ld. CIT(A) arises because the assessee has challenged the assessment order dated 21.12.2022 passed under section 143(3) r.w.s. 144B of the Income Tax Act, 1961 [ for short “Act”] by National Faceless Assessment Unit [ for short AO ].

2. The assessee has assailed the present appeal on the following grounds: -

1. That the Ld. AO has erred in law as well in facts in passing order u/s. 143(3) r.w.s 144B of IT Act.

2. That both the lower authorities have erred in law as well in facts in invoking/sustaining rejection of books of Accounts u/s 145(3) of the Act.

3. That both the lower authorities have erred in law as well in facts in making/sustaining addition of Rs. 1,29,91,430/- by estimating Income by applying unprecedented GP rate of 8%, divorced from past history, comparable case & nature of business and thereby made/sustain addition of Rs. 1,29,91,430/-.

4. That Ld. CIT(A) erred in law as well in facts in not holding that AO travelled beyond the scope of limited scrutiny in violation of CBDT guideline.

5. That the appellant reserves his right to add, amend, alter or withdraw any ground of appeal on or before hearing of this appeal.

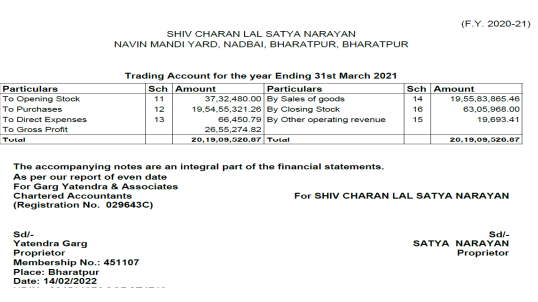

3. Succinctly, the fact as culled out from the records is that the assessee is the proprietor of M/s Shivcharanlal Satyanarayan and is a General Commission Agent at Navin Mandi, Nadbai, Bharatpur. The assessee has filed his return of income showing Rs. 4,94,540/- as his taxable income on a total turnover of Rs. 19,56,03,558/-. The case was selected for scrutiny through CASS for the following reason:

Assessee has made substantial purchases from such suppliers who are either non filers or have filed non business ITR or reflected a substantially lower turnover in ITR as compared to turnover shown in GSTR 1 Return. There is possibility that assessee has booked bogus expenses in order to reduce its profit/taxable income. Therefore genuineness/correctness of expenses related with these entities may be verified.

3.1 Based on the above reasons ld. AO noted that the assessee has made substantial purchases from such suppliers who are either non-filers or have filed non business ITR or reflected a substantially lower turnover in ITR as compared to turnover shown in GSTR 1 Return and therefore, he noted that there is possibility that assessee has booked bogus expenses in order to reduce its profit / taxable income. As a result, notices u/s 143(2), u/s 142(1) and other notices/letters were issued from time to time for conducting enquiries and making compliances. The assessee was required to furnish reply to inter-alia regarding purchases, transportation, payments to suppliers, expenses etc. In response to the above, the assessee had furnished the list of all suppliers from whom purchases were made. He also submitted the payments made to them but not supported the same by necessary evidence. The assessee also did not furnish the details of transportation and merely stated that the transportation was mostly done by Tractor trolley, camel cart and buffalo cart.

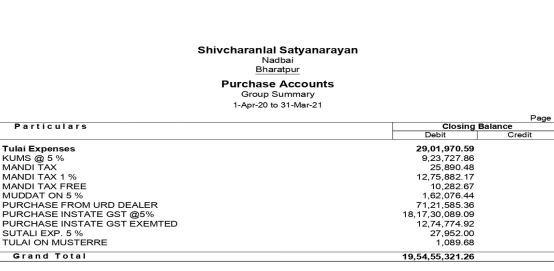

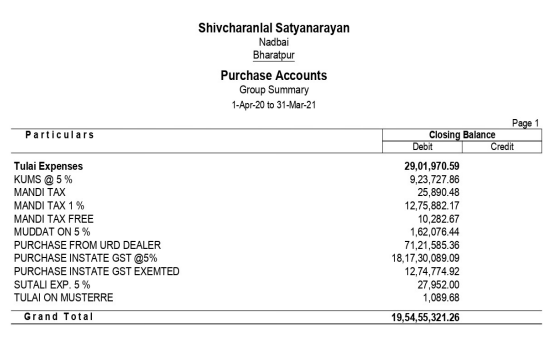

3.2 Ld. AO considering the information so submitted by the assessee ld. AO noted that total GST purchase [exclusive of GST ] shown by the assessee is Rs. 18,17,30,089/- while the corresponding purchase available on the system amounts to Rs. 18,50,48,070/- [Difference amount Rs. 33,17,981/- ]. The ld. AO asked the assessee to furnish the details of payment made to the supplies along with supporting docum

An indispensable Tool for Legal Professionals, Endorsed by Various High Court and Judicial Officers

Please visit our Training & Support

Center or Contact Us for assistance

Scan Me!

India’s Legal research and Law Firm App, Download now!

For Daily Legal Updates, Join us on :