INCOME TAX APPELLATE TRIBUNAL (DELHI BENCH)

SH. PRADIP KUMAR KEDIA, ACJ, SHRI YOGESH KUMAR U.S., JM

NIHON PARKERIZING (INDIA) PVT. LTD. GURGAON – Appellant

Versus

DCIT CIRCLE-18(1) NEW DELHI – Respondent

| Table of Content |

|---|

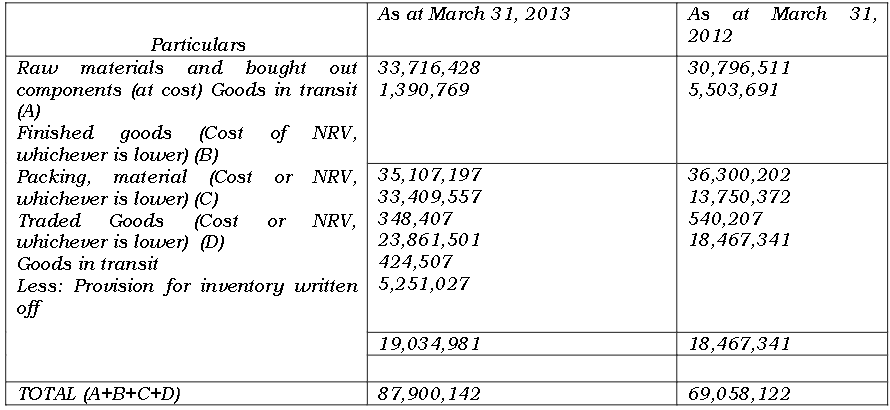

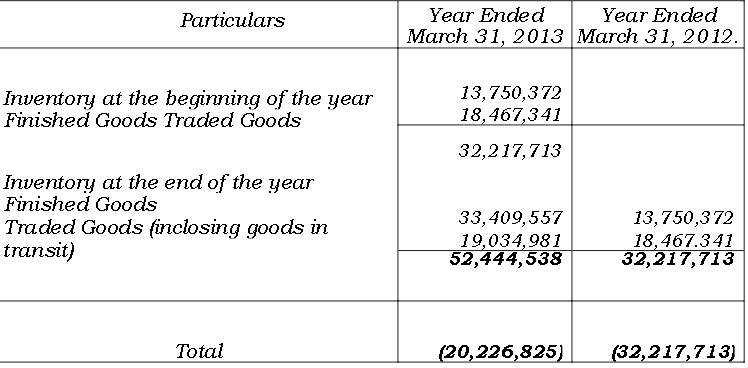

| 1. overview of assessment and disallowances due to inventory write-off. (Para 3 , 4) |

| 2. arguments regarding the disallowance of inventory write-off and failure of the cit(a) to appreciate documentation. (Para 5 , 6) |

| 3. court observations on inventory valuation practices and necessity of substantiation. (Para 7 , 8 , 12 , 14) |

| 4. the tribunal's reasoning for allowing the deduction based on relevant case laws and accounting standards. (Para 13 , 15) |

ORDER

PER YOGESH KUMAR U.S., JM

The present appeal is filed by the assessee for Assessment Year 2013-14 against the order of the Ld. Commissioner of Income Tax (Appeals)- (‘Ld. CIT(A)’ for short)-6, New Delhi, dated 18/04/2019.

2. The grounds of Appeal are as under:-

“1. That the order of the Ld. Commissioner of Income Tax (Appeals)-6, New Delhi ("CIT-A"), of not allowing deduction of Rs 52,51,027/- in respect of traded goods written off on account of obsolete, damaged, expired stock and not appreciating the various facts of the case as per the details, explanation and documents provided by the assessee during the course of assessment/appellate proceedings, is against law and facts of the case.

2. That the order of the Ld. Commissio

An indispensable Tool for Legal Professionals, Endorsed by Various High Court and Judicial Officers

Please visit our Training & Support

Center or Contact Us for assistance

Scan Me!

India’s Legal research and Law Firm App, Download now!

For Daily Legal Updates, Join us on :