INCOME TAX APPELLATE TRIBUNAL (MUMBAI BENCH)

SHRI OM PRAKASH KANT, AM, SHRI SUNIL KUMAR SINGH, JM

ACIT 32(1) – Appellant

Versus

VKT Ventures LLP – Respondent

ORDER

PER OM PRAKASH KANT, AM

These appeals by the Revenue are directed against two separate orders dated 06.03.2024 and 07.03.2024 passed by the Ld. Commissioner of Income-tax (Appeals) — National Faceless Appeal Centre, Delhi [in short ‘the Ld. CIT(A)’] for assessment year 2013-14 and 2014-15 respectively.

2. The sole ground involved in both these appeals is in respect of the disallowance of interest u/s 36(1)(iii) of the Income-tax Act, 1961 (in short ‘the Act). Therefore, both these appeals were heard together and disposed off by way of this consolidated order for convenience. For Brevity the ground raised by the assessee in assessment year 2013-14 is reproduced as under:

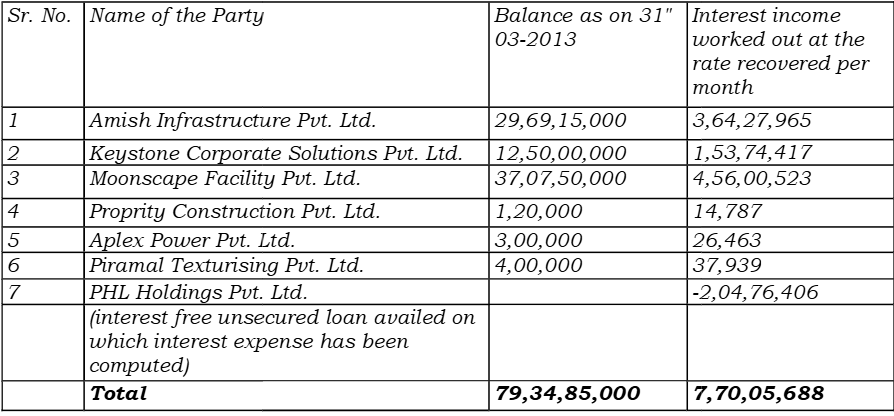

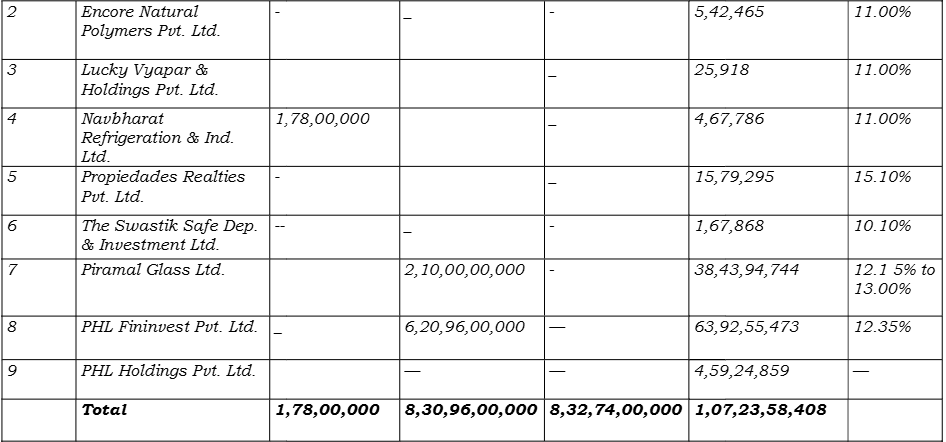

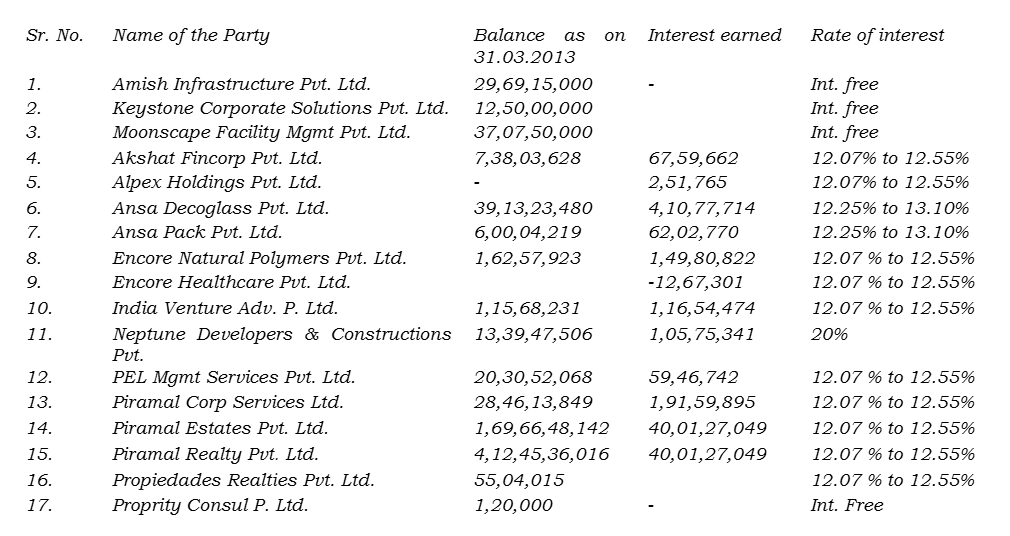

1. On the facts and in the circumstances of the case and in law, the Ld. CIT(A) erred in deleting the disallowance of interest of Rs.123046063/- u/s 36(1)(iii) of the Income Tax Act.

3. Briefly stated facts of the case are that the assessee firm is in the business of investment and finance activity along with trading in goods and commodities. The assessee filed return of income electronically on 29.09.2013 declaring total income _ at Rs.35,99,660/-. The return of income filed by the assessee was selected for scruti

An indispensable Tool for Legal Professionals, Endorsed by Various High Court and Judicial Officers

Please visit our Training & Support

Center or Contact Us for assistance

Scan Me!

India’s Legal research and Law Firm App, Download now!

For Daily Legal Updates, Join us on :