INCOME TAX APPELLATE TRIBUNAL (INDORE BENCH)

Shri Vijay Pal Rao, Shri B.M. Biyani, JJ

Revenue – Appellant

Versus

Assessee – Respondent

| Table of Content |

|---|

| 1. background facts pertaining to the appeals. (Para 1 , 2 , 3) |

| 2. revenue's grounds challenging cit(a)'s actions. (Para 4 , 5 , 6) |

| 3. discussion on applicability of section 40a(3). (Para 7 , 8 , 9) |

| 4. observations by the court on cash payments to hamals. (Para 10 , 11 , 12) |

| 5. court's analysis on dvo's report and valuation dispute. (Para 13 , 14 , 15) |

| 6. conclusions on the estimated cost of the construction. (Para 16 , 17 , 18) |

| 7. final decision regarding the disallowance of expenses. (Para 19 , 20) |

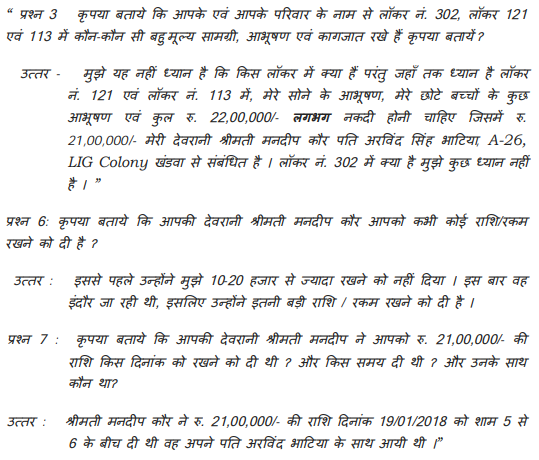

| 8. assessment of locker cash as unexplained. (Para 21 , 22 , 23) |

| 9. final decision on the appeal resolutions. (Para 24 , 25 , 26 , 27) |

ORDER

Per Bench:

The captioned three appeals are related to same assessee. ITA No. 206 & 207/Ind/2023 for AY 2015-16 and 2016-17 respectively are preferred by revenue and ITA No. 227/Ind/2023 for AY 2018-19 is preferred by assessee. All these appeals are directed against appeal-order dated 30.03.2023 passed by learned Commissioner of Income-tax (Appeals)-3, Bhopal [“CIT(A)”] which in turn arise out of assessment-order dated 30.12.2009 passed by ACIT, Ujjain, stationed at Indore [“AO”] u/s 153A/143(3) of the Income-tax Act, 1961 [“the Act”].

2.

An indispensable Tool for Legal Professionals, Endorsed by Various High Court and Judicial Officers

Please visit our Training & Support

Center or Contact Us for assistance

Scan Me!

India’s Legal research and Law Firm App, Download now!

For Daily Legal Updates, Join us on :