INCOME TAX APPELLATE TRIBUNAL (INDORE BENCH)

Shri Vijay Pal Rao, J, Shri B.M. Biyani, A.M.

LATE MANOHARASINGH THROUGH LEGAL HEIR SHRI SURAJ MANDLOI INDORE – Appellant

Versus

ITO 1(1) INDORE – Respondent

| Table of Content |

|---|

| 1. background of appeal regarding unexplained cash deposits. (Para 1 , 2) |

| 2. challenges upon initial assessment findings. (Para 4 , 10) |

| 3. assessment of cash sources and evidence by the court. (Para 6 , 11 , 12) |

| 4. discussion on the retroactive application of amended tax rates. (Para 15 , 16) |

| 5. final ruling on the appeal based on evidentiary grounds. (Para 17) |

आदेश/ORDER

Per B.M. Biyani, A.M.:

Feeling aggrieved by appeal-order dated 06.12.2019 passed by learned Commissioner of Income-Tax (Appeals)-NFAC, Delhi [“CIT(A)”] which in turn arises out of assessment-order dated 06.12.2019 passed by learned ITO- 1(1), Indore [“AO”] u/ s 143(3) of Income-tax Act, 1961 [“the Act”] for Assessment-Year [“AY”] 2017-18, the assessee has filed this appeal.

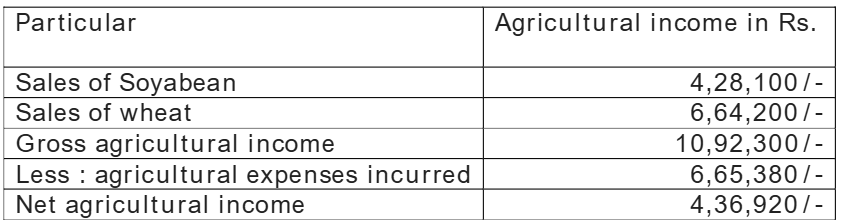

2. The background facts leading to present appeal are such that the assessee filed return of AY 2017-18 on 30.03.2018 declaring aggregate income of Rs. 7,39,140/ - consisting of taxable income of Rs. 3,02,220/ - from other sources and agricultural income of Rs. 4,36,920/ -, which was subjected to “limited scrutiny” assessment through CASS to examine “cash deposits during demonetization period”. Accordingly, the AO issued notices u/ s 1

An indispensable Tool for Legal Professionals, Endorsed by Various High Court and Judicial Officers

Please visit our Training & Support

Center or Contact Us for assistance

Scan Me!

India’s Legal research and Law Firm App, Download now!

For Daily Legal Updates, Join us on :