INCOME TAX APPELLATE TRIBUNAL (JAIPUR BENCH)

DCIT CIRCLE-2 JAIPUR – Appellant

Versus

SMT. VEENA GOAYAL JAIPUR – Respondent

ORDER

PER: R.C. SHARMA, A.M.

These are the appeals filed by the revenue against the separate orders of ld. CIT(A)-I, Jaipur dated 19/11/2019 for the A.Y. 2013-14 in the matter of order passed U/s. 143(3) r.w.s. 147 of the Income Tax Act, 1961 (in short, the Act).

2. Common grounds have been taken by the revenue in both these appeals and both the assessees are related persons, therefore both these appeals are heard together and disposed of by this consolidated order.

3. The hearing of the appeal was concluded through video conference in view of the prevailing situation of Covid-19 Pandemic.

4. Firstly, we take ITA No. 75/JP/2020.

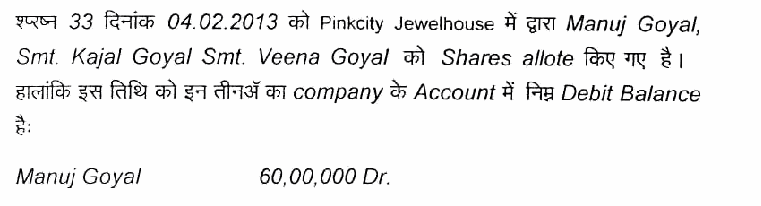

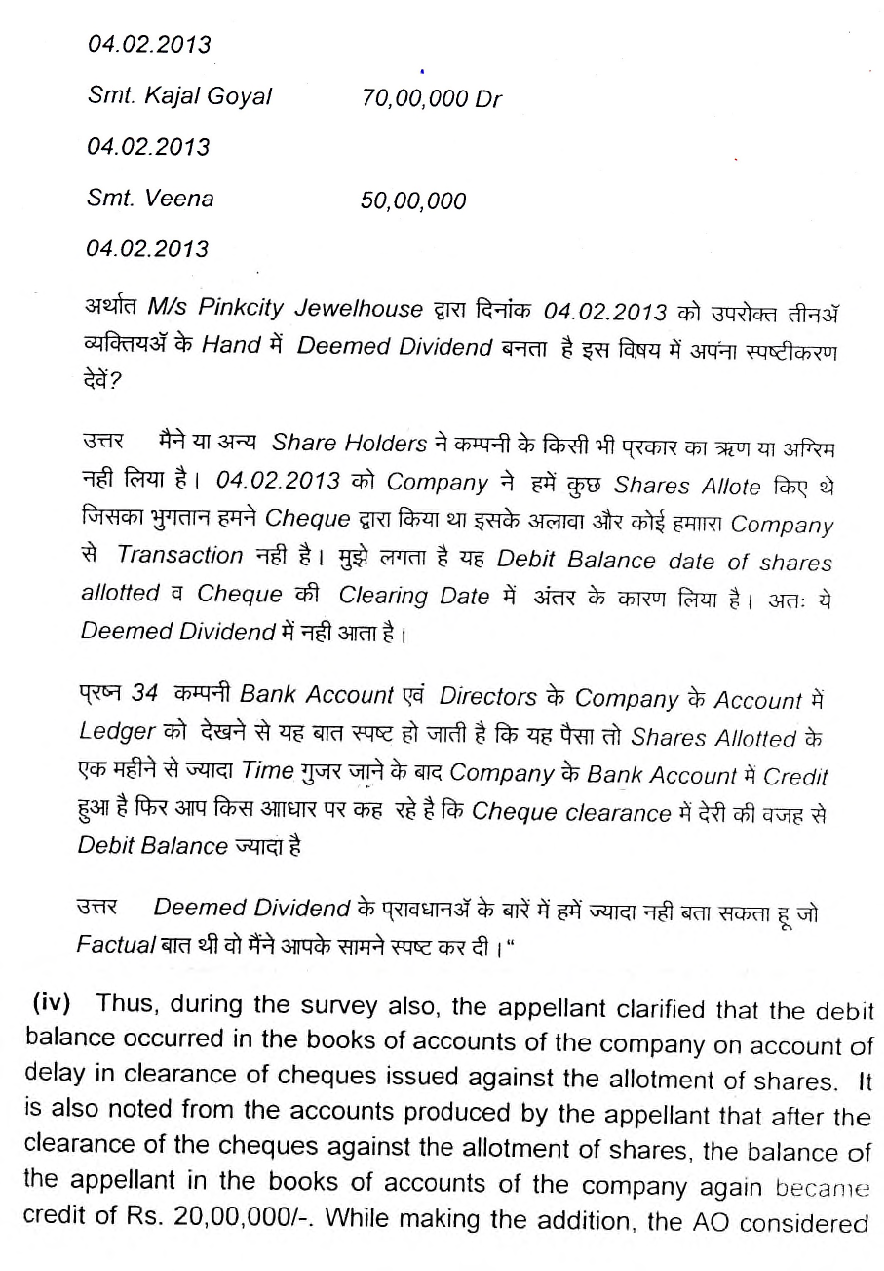

In this appeal, the revenue is aggrieved for deleting the addition of Rs. 50.00 lacs made by the A.O. U/s 2(22)(e) of the Act for deemed dividend.

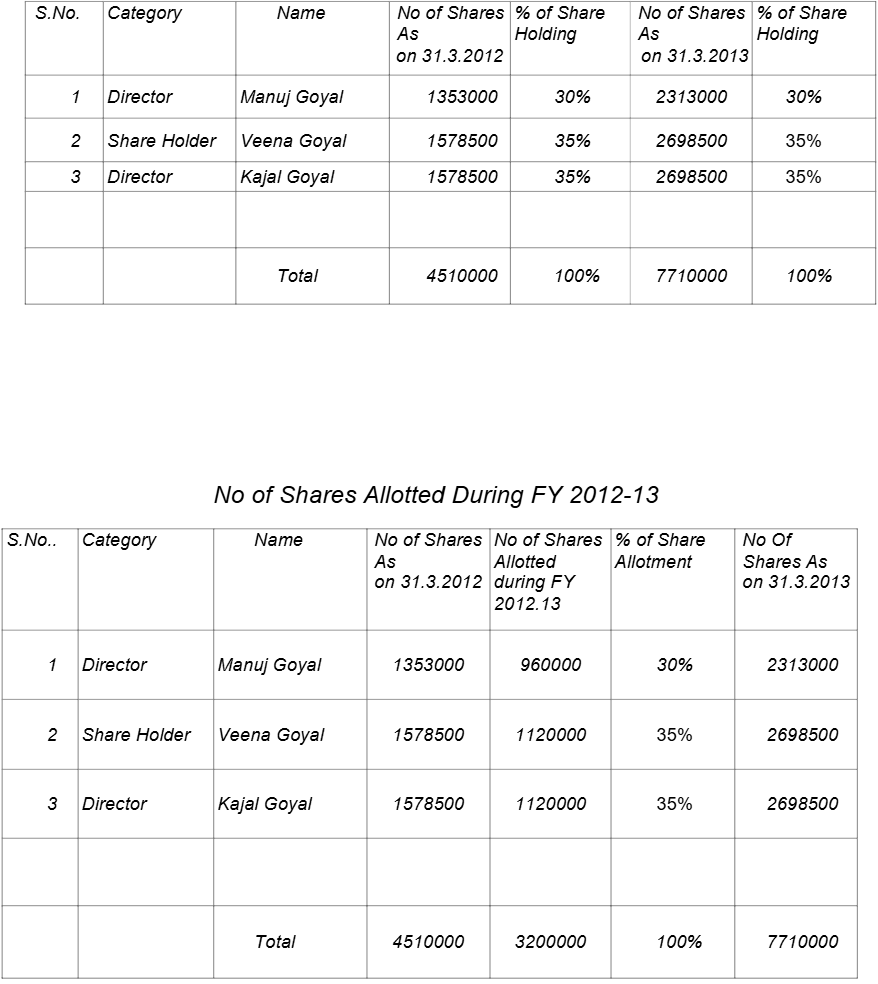

5. Rival contentions have been heard and record perused. The brief facts of the case are that the assessee who is a Share Holder in M/s Pinkcity Jewelhouse Pvt. Ltd. having more than 10% voting power had applied for allotment of shares of the Company Pinkcity jewel House Pvt Ltd. The assessee accepted the offer and applied for allotment of 11,20,000 shares and paid the value of shares amounting to Rs. 1,12,00,000/- thro

An indispensable Tool for Legal Professionals, Endorsed by Various High Court and Judicial Officers

Please visit our Training & Support

Center or Contact Us for assistance

Scan Me!

India’s Legal research and Law Firm App, Download now!

For Daily Legal Updates, Join us on :