INCOME TAX APPELLATE TRIBUNAL (BANGALORE BENCH)

WEBEX COMMUNICATIONS INDIA PRIVATE LIMITED BANGALORE – Appellant

Versus

DCIT BANGALORE – Respondent

ORDER

PER BENCH :

These are seven appeals arising out of separate orders of the CIT (A), dt.27.11.2012, for AYs.2001-02, 2003-04, 2005-06, and orders dt.30.11.2012, for AYs.2002-03, 2004-05, 2006-07 and 2007-08, respectively.

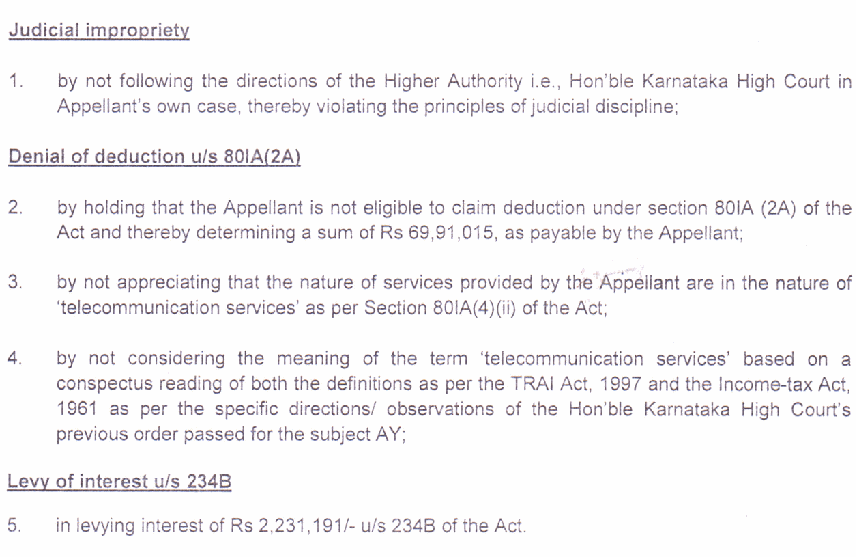

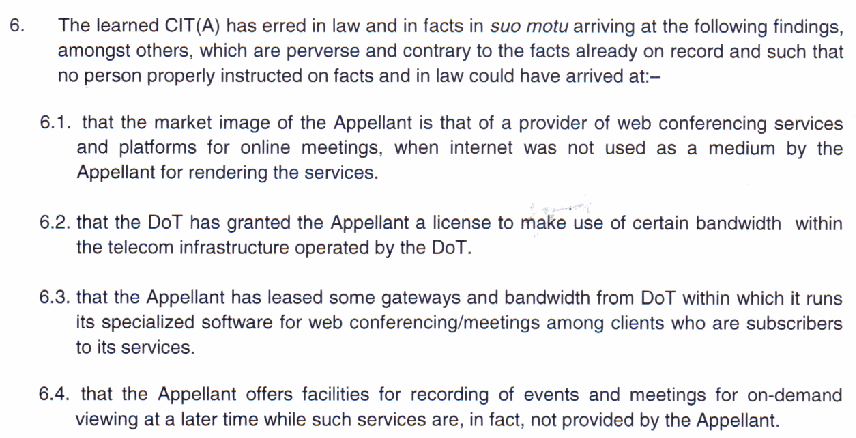

02. The common grounds of appeal raised by the assessee, are as under :

The assessee has also raised additional grounds as under :

02. The Ld. AR had submitted before us that this is the second round of litigation and has submitted that the Honourable High Court vide its order in I.T.A. No.2775/2005, dated 12.04.2010, in para 9 to 11, reproduced hereinbelow, had remanded the matter back to the AO for deciding this issue in terms of the observation made by the Honourable High Court :

9. Further the question as to whether the services rendered by the assessee comes within the definition of ‘telecommunication service' has also not been taken into consideration in its proper perspective and it has been answered that the assessee's service does not come within the scope of telecommunication service. Though the Income Tax Act does not define as to what telecommunication service, nevertheless, it would be appropriate to re(cid:1)er to the definition of teleco(cid:2)(cid:2)

An indispensable Tool for Legal Professionals, Endorsed by Various High Court and Judicial Officers

Please visit our Training & Support

Center or Contact Us for assistance

Scan Me!

India’s Legal research and Law Firm App, Download now!

For Daily Legal Updates, Join us on :