INCOME TAX APPELLATE TRIBUNAL (DELHI BENCH)

Shri Challa Nagendra Prasad, J, Shri Avdhesh Kumar Mishra, ACJ

Aarti Bansal – Appellant

Versus

Income Tax Officer – Respondent

I.T.A No.5942/Del/2024

| Table of Content |

|---|

| 1. assessee appeals against the validity of reassessment. (Para 1) |

| 2. arguments on procedural errors and notice issuance. (Para 2 , 3 , 4) |

| 3. court discusses the parameters of legal compliance. (Para 5 , 6 , 7) |

| 4. court rules on validity based on limitation. (Para 8) |

| 5. conclusion on the appeal's outcome. (Para 9 , 10) |

आदेश /ORDER

PER C.N. PRASAD, J.M.

This appeal is filed by the Assessee against the order of the Ld. CIT(Appeals)-NFAC, dated15.10.2024 for the AY 2014-15. Assessee has raised the following grounds in her appeal: -

1. “On facts and circumstances of the case, the reassessment proceedings-initiated u/s 147 of IT Act by issue of notice dated 22.07.2022 u/s 148 of IT Act is barred by limitation and therefore, the reassessment proceedings and consequent reassessment order are void-ab-initio.

2. On the facts and circumstances of the case and also in law, the assessment proceedings and the assessment order both are bad in law and need to be quashed as no notice u/s 143(2) of IT Act was issued by the AO before completion of assessment proceedings against the return of income filed in response to notice u/s 148 of IT Act.

3. On facts and circumstances of the case, the reassessment proceedings have been initiated u/s 147/148/148A of IT Act without making compliance of provisions of sec 149(1) of IT Act and therefore, the reassessment proceedings and consequent reassessment order are needs to be quashed.

4. The impugned assessment is invalid and without jurisdiction as the said assessment has been initiated and completed without complying with legal requirements of the provisions of section 147/148/148A/15I of the Income Tax Act, therefore such assessment is void ab initio and liable to be quashed.

5. The Ld. AO has erred both in law and circumstances of the case in initiating action u/s 147/148A of IT Act ignoring the fact that the proceedings have been initiated without application of independent mind on the material, if any, available. In view of the above defects in the compliances the resultant reassessment proceedings are required to be set aside.

6. The Ld. AO has erred both in law and circumstances of the case in initiating action u/s 147/148/148A of IT Act ignoring the fact that the proceedings have been initiated by mechanical approval accorded by the Pr CCIT, Delhi and such approval vitiates the assessment.

7. On facts and circumstances of the case, the Ld AU has erred in making addition of Rs.59,64,116/- u/s 69C of IT Act ignoring the fact that the above provision has no application when the requirement of said section is not complied with.

8. The appellant craves leave to add, delete, modify / amend the above grounds of appeal with the permission of the Hon’ble appellate authority.”

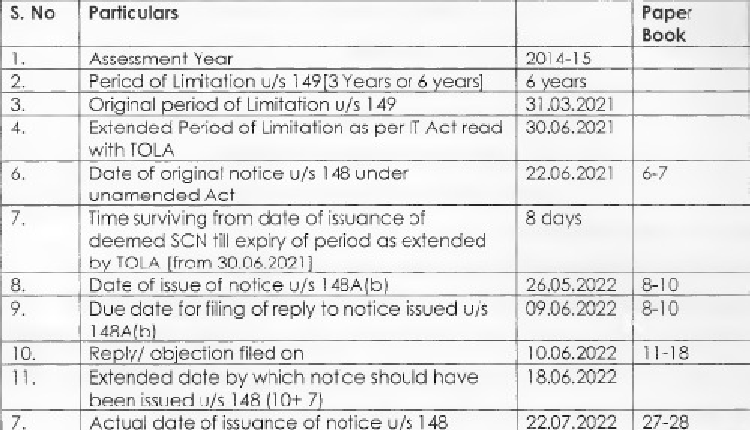

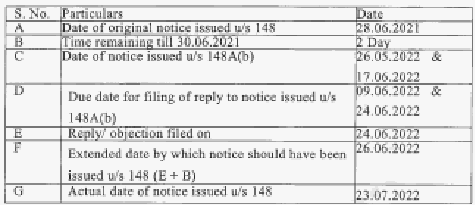

2. The Ld. Counsel for the assessee, at the outset, submitted that the reassessment proceedings are barred by limitation as the notice u/s 148 of the Act was issued under un-amended act to the assessee on 22.06.2021 (PB 6-7). However, the above notice was uploaded on e-portal on 30.06.2021 but was never served upon the appellant as evident from screenshot at pages 3 to 5 and 6. Ld. Counsel submitted that section 148 of the Act has been substituted by Finance Act, 2021 w.e.f. 01.04.2021 wherein notice u/s 148 of the Act as per the old provisions of section 148 of the Act applicable upto 31.03.2021 could not have been issued after 31.03.2021. This issue per se was subject matter of various writ petitions filed in various High Courts and ultimately got settled by the Hon'ble Supreme Court in the case of Union of India Vs. Ashish Agarwal reported in 444 ITR 1 (SC) dated 04.05.2022. Thereafter, the Id AO issued letter u/s 148A(b) of the Act on 26.05.2022 (PB 8-10). The assessee filed its reply on 10.06.2022 (PB 11-18). The Id AO passed an order u/s 148A(d) of the Act on 22.07.2022 (PB 19-26) rejecting the objections of the assessee and proceeded to issue notice u/s 148 of the Act on 22.07.2022 (PB 27-28).

3. Ld. Counsel submitted that

An indispensable Tool for Legal Professionals, Endorsed by Various High Court and Judicial Officers

Please visit our Training & Support

Center or Contact Us for assistance

Scan Me!

India’s Legal research and Law Firm App, Download now!

For Daily Legal Updates, Join us on :