INCOME TAX APPELLATE TRIBUNAL (MUMBAI BENCH)

(RETD.) C V BHADANG, PRESIDENT, MS PADMAVATHY S, AM

Mrs. Snehlata Goel – Appellant

Versus

DCIT-3(3)(1) – Respondent

I.T.A. No. 1793/Mum/2024

| Table of Content |

|---|

| 1. background of appeal and basic facts (Para 1 , 2) |

| 2. arguments presented by the assessee regarding land classification (Para 3 , 4) |

| 3. arguments from the revenue focusing on non-agricultural use (Para 5 , 6 , 7 , 8) |

| 4. court's observations on necessary evidence and legal dimensions surrounding agricultural status (Para 9 , 10 , 11 , 12 , 13 , 14) |

ORDER

Per Padmavathy S, AM:

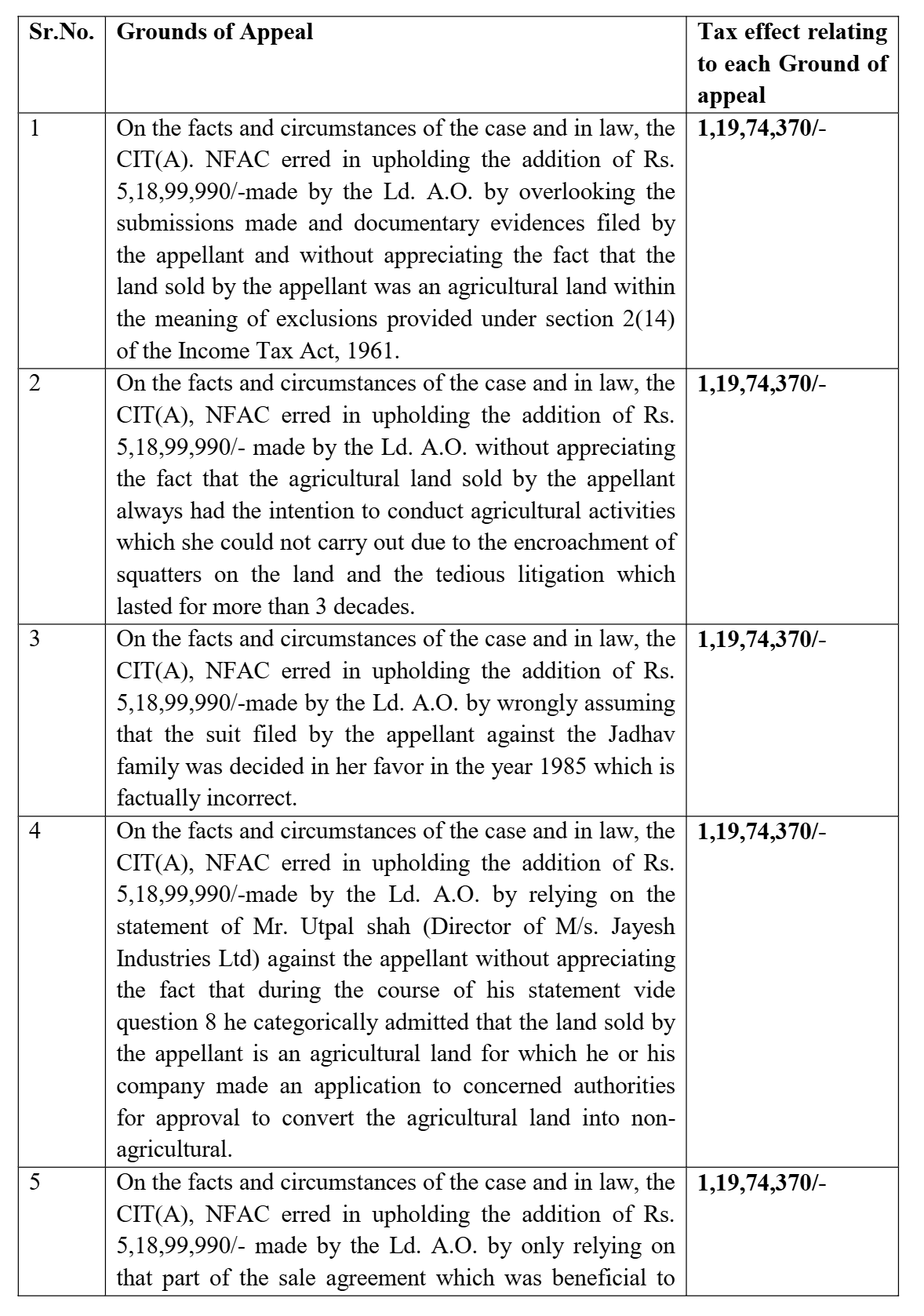

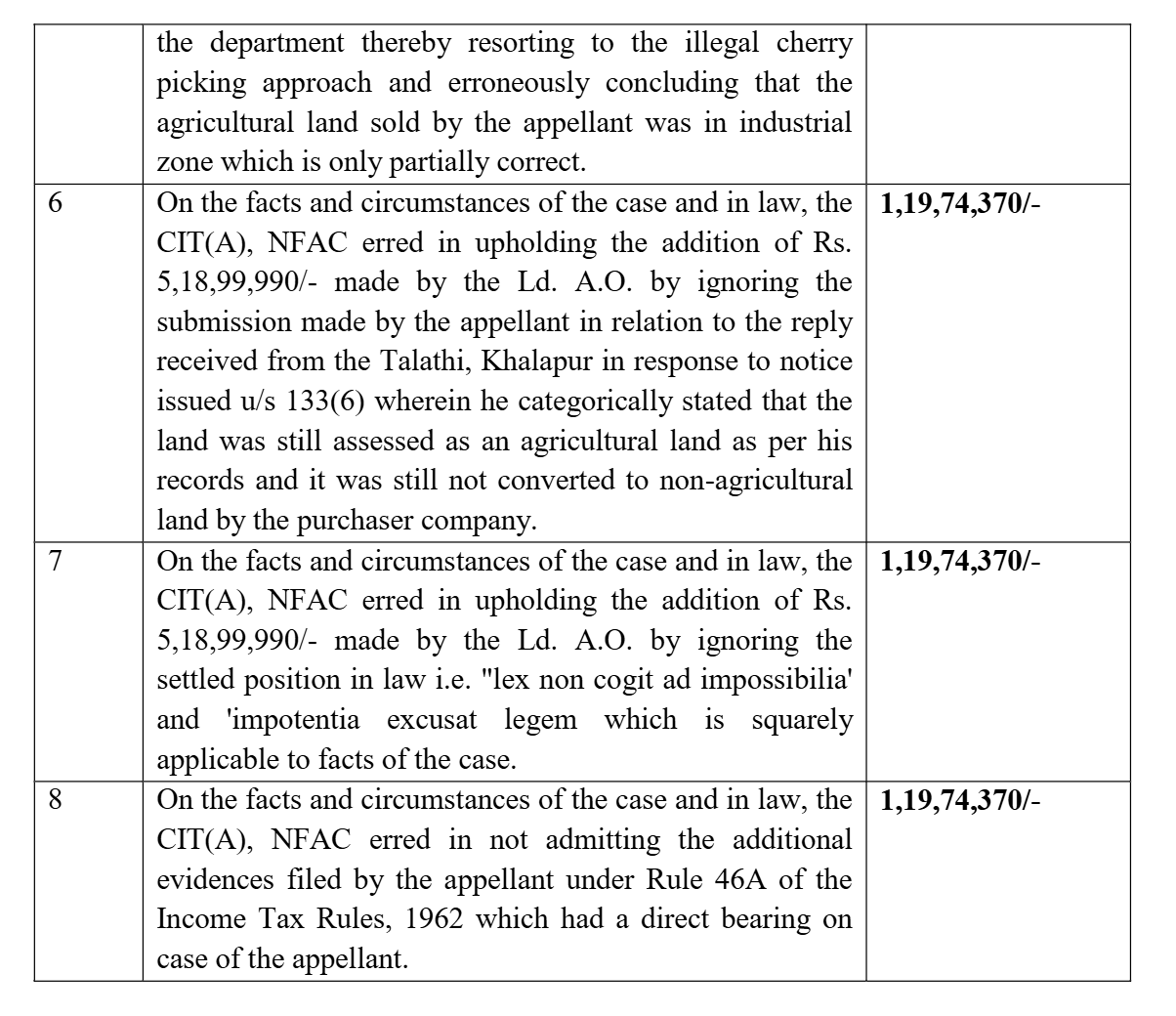

This appeal by the assessee is against the order of the Commissioner of Income Tax (Appeals) / National Faceless Appeal Centre (NFAC), Delhi [In short 'CIT(A)'] passed under section 250 of the Income Tax Act, 1961 (the Act) dated 01.03.2024 for Assessment Years (AY) 2016-17. The assessee raised the following grounds of appeal:

2. The assessee is an individual and filed the return of income for AY 2016-17 on 04.08.2016 declaring a total income of Rs. 25,58,120,/-. The assessee's case was selected for scrutiny and the statutory notices were duly served on the assessee. The Assessing officer (AO) during the course of assessment noticed that during the year under consideration, the assessee has sold a land bearing survey No.132/2A lying at Village Tambati, Taluka Khalapur, Raigad District, Maharashtra to M/s Jayesh Industries for a consideration of Rs. 5,20,00,000/-. The AO further noticed that the assessee has claimed the Capital Gain arising out of the said sale as exempt stating that the land sold is an agricultural land. The AO also noticed that the land sold is falling in the Industrial Zone of sanctioned Pen, Panvel, Khalapur Growth Centre of Raigad Regional Development Plan. Accordingly, the AO issued a show-cause notice to the assessee as to why the land sold should not treated as capital asset and taxed accordingly. The assessee in response filed various details and explanations as summarised below:

“1. The referred land parcel sold by the assesse was purchased as agricultural land.

2. The land parcel satisfies all the conditions of being an agricultural land as per definition u/s. 2(14)

3. The area in which land parcel was situated was designated as Industrial Zone by the Government of Maharashtra subsequently.

4. The mentioning of land numbers in 7/12 extracts itself substantiate that it was agricultural land parcel.

5. The land parcel was never used for any industrial purpose by the assessee and had actually used for agricultural purposes as substantiated by 7/12 extracts submitted.

6. The purchaser has done its due diligence before registering the agreement and obtained confirmations that the land is covered under the Industrial Zone so that it can it can put industry thereon.

7. The land parcel was sold by the assessee as agricultural land.

8. The conversion of land has been done by the purchaser after purchasing the land parcel who also paid the premium amount “Nazarana Fees” for conversion as required under the Rules prescribed in this regard.”

3. The AO issued a summons under section 131 to the Director of M/s Jayesh Industries and based on the statements recorded held that the purchaser would not have purchased the land if the land did not fall in the Industrial Zone and therefore the land sold is not an agricultural land. The AO further held that though the 7 /12 extracts mentioned the land as agricultural land, the assessee has not carried out any agricultural activity from 1997-98 and therefore there is no intention of the assessee to carry on any agricultural activity. The AO also deployed Inspector to proceed to impugned land and from the report of the inspector the AO recorded a finding that the entire belt comprises of 7 industrial set up and that M/s Jayesh Industries has constructed industrial unit therein. The AO further recorded a finding that the assessee has sold a land for non-agricultural purposes i.e. to be used for industrial purposes. Accordingly, the AO held that the land sold by the assessee is not an agricultural land and therefore the gain arising from the sale of the land cannot be exempt.

4. Aggrieved assessee file

An indispensable Tool for Legal Professionals, Endorsed by Various High Court and Judicial Officers

Please visit our Training & Support

Center or Contact Us for assistance

Scan Me!

India’s Legal research and Law Firm App, Download now!

For Daily Legal Updates, Join us on :