INCOME TAX APPELLATE TRIBUNAL (DELHI BENCH)

ARGOS HOLDINGS PTE. LTD. SINGAPORE – Appellant

Versus

DEPUTY COMMISSIONER OF INCOME TAX CIRCLE INT TAX 1(1)(1) DELHI DELHI – Respondent

ITA 3632/DEL/2025[2015-16]

| Table of Content |

|---|

| 1. introduction to appeals and assessment order. (Para 1 , 2) |

| 2. legal grounds for additional appeal. (Para 3 , 5 , 6) |

| 3. evidence of foreign company status. (Para 10 , 18) |

| 4. jurisdictional issues and statutory obligations. (Para 20 , 21) |

| 5. conclusion and resolution of appeal. (Para 22 , 23) |

ORDER

PER S. RIFAUR RAHMAN, ACCOUNTANT MEMBER :

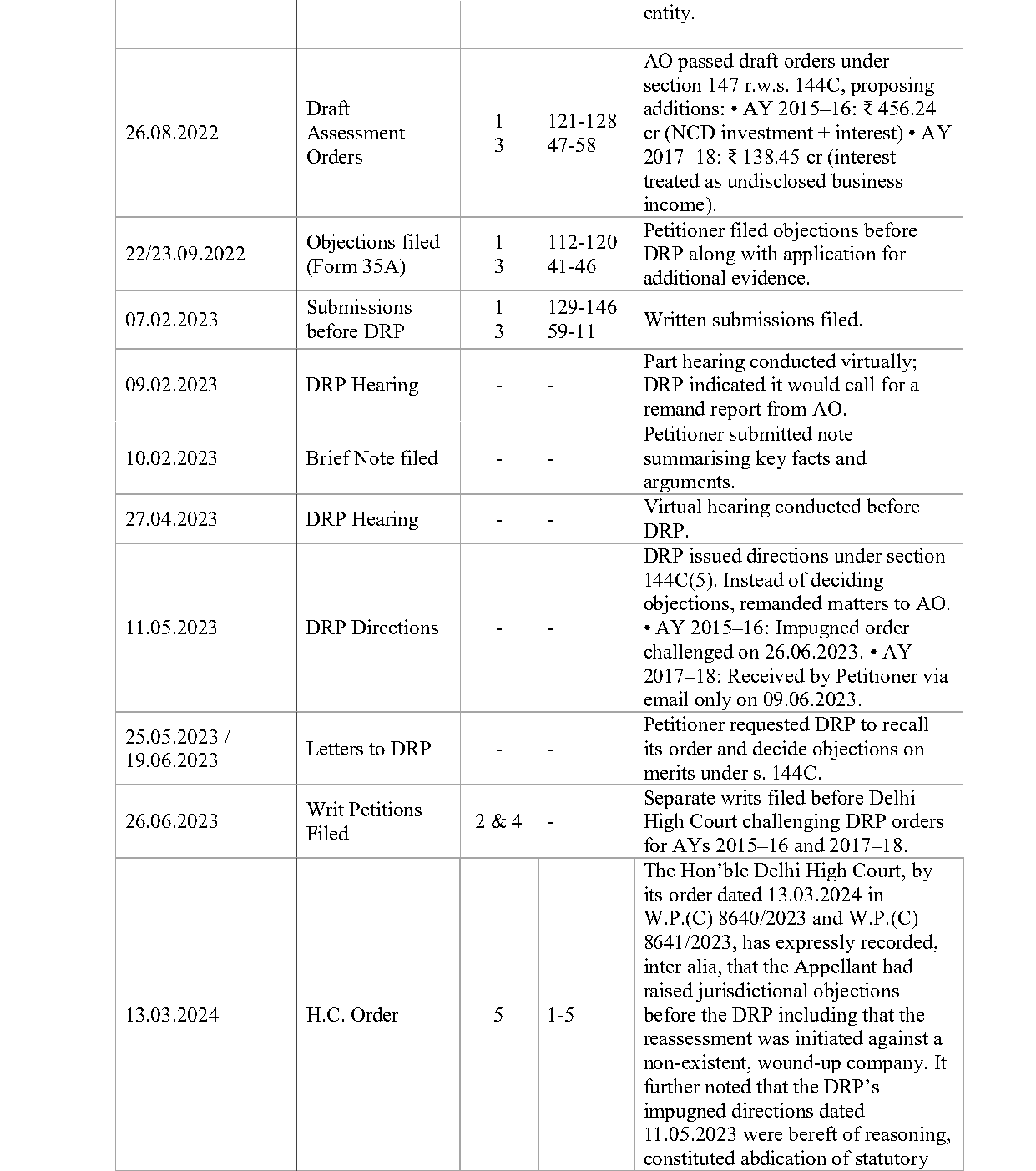

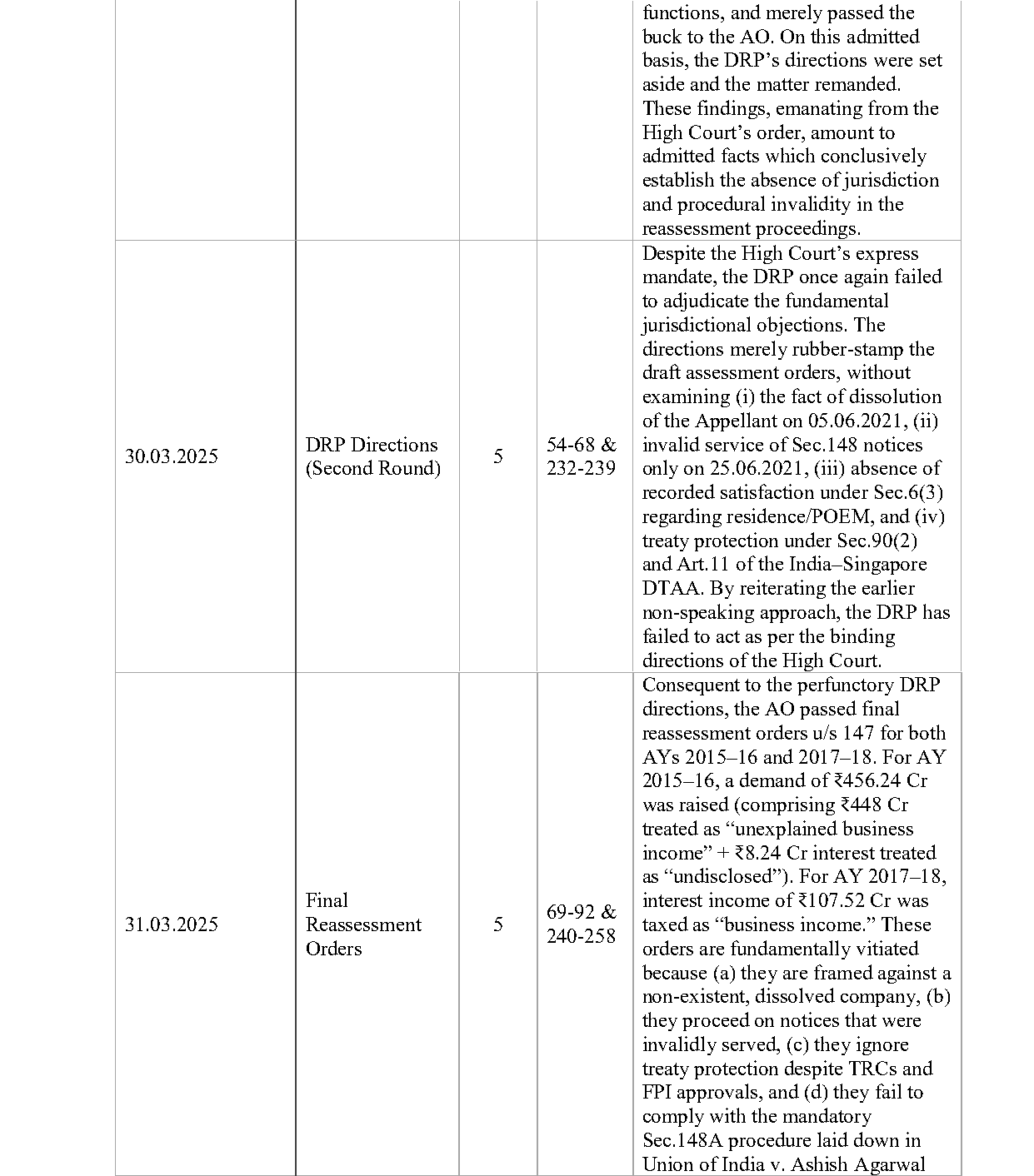

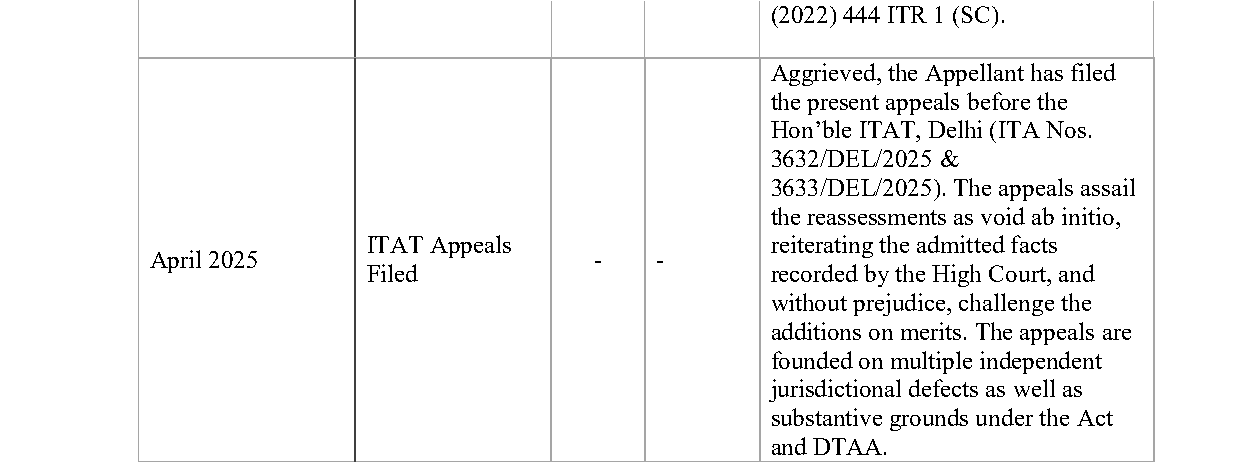

1. These appeals preferred by the assessee are directed against the assessment order dated 31.03.2025 passed by the DCIT, Circle Int. Tax 1(1)(1), Delhi under section 147 read with section 260 of the Income-tax Act, 1961 (for short ‘the Act”) for Assessment Years 2015-16 & 2017- 18pursuant to the directions of the Dispute Resolution Panel u/s 144C(5) of the Act.

2. Since the issues are common and the appeals are connected, hence the same are heard together and being disposed off by this common order. First, we take up AY 2015-16 as the lead case.

3. At the outset of the hearing, ld. AR submitted that assessee has filed additional grounds of appeal under Rule 11 of the Income Tax (Appellate Tribunal) Rules and it is purely legal issue and the same is reproduced below :-

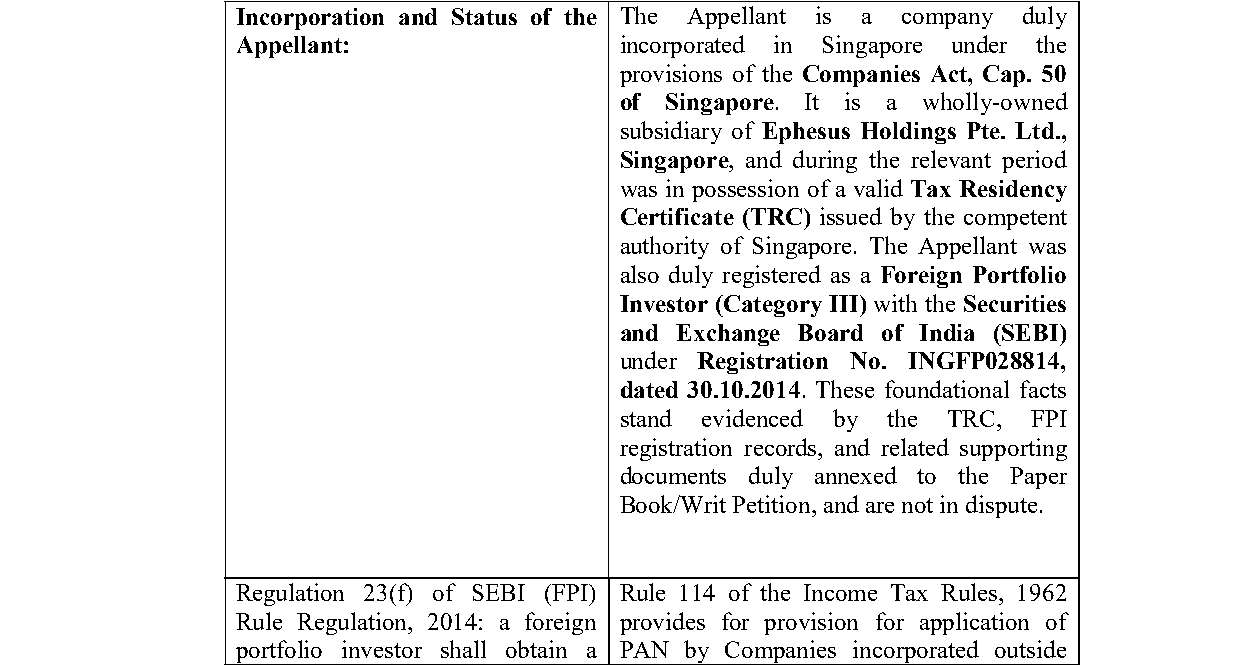

“1. That the Appellant being a foreign company having no Permanent Establishment (P.E.) in India for A.Y. 2015-16, the provisions of section 6(3) were consequently inapplicable, warranting that the Ld. Assessing Officer had no jurisdiction to assess income in India; consequently, there could not have been any escapement of income under section 148 of the Act.

2. That the Ld. Assessing Officer misdirected himself by alleging 'Place of Effective Management' (POEM) in India, whereas the unamended section 6(3)(ii) applied for A.Y. 2015-16, thereby rendering the action of the Ld. Assessing Officer ultra vires to the provisions of the Act.

3. That the Appellant company being a foreign company and a SEBI-registered Foreign Portfolio Investor (Category III) had no income chargeable to tax other than interest income on which tax under section 194LD had been duly withheld, thus warranting no requirement to file a return of income under section l115(S) of the Income Tax Act, 1961.

4. That the entire action of the Ld. Assessing Officer in invoking section 148 on the alleged ground of "information flagged on Non-Filers Management System" is contrary to the express provisions of law contained in section 1ISA(S) of the Act.

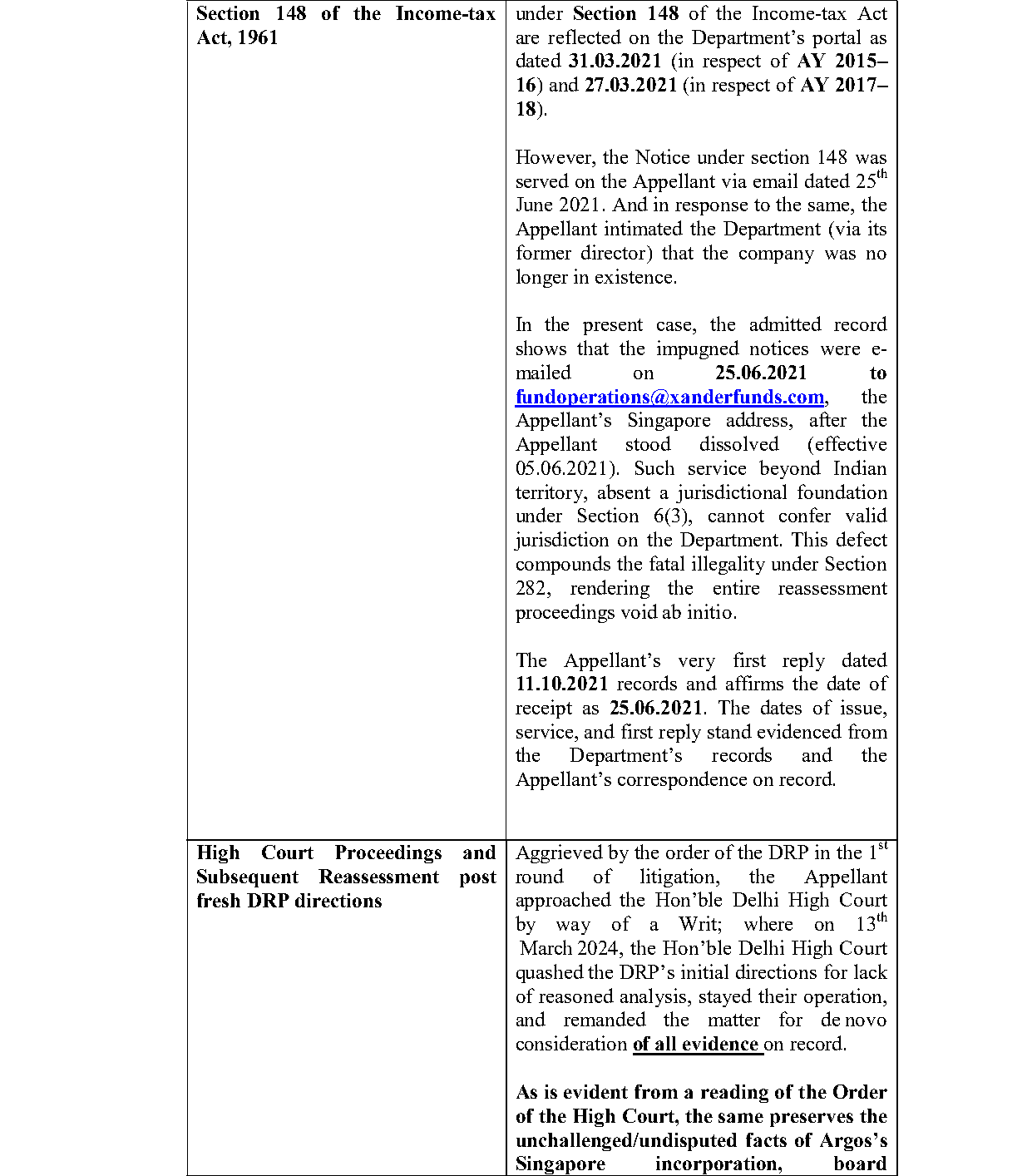

5. That the impugned notice under section 148 issued under the unamended provision of law as on 31.03.2021, but served on 25.06.2021, is contrary to the mandate of law as laid down by the Hon'ble Supreme Court in Union of India v. Ashish Agarwal [2022 SCC OnLine SC 543].

6. That the Revenue failed to initiate proceedings under section 148A for a notice issued under the old provisions of section 148 of the Act. The same cannot be upheld as the old provisions ceased to have force of law post 31.03.2021.”

4. Since the above grounds of appeal are purely legal, do not require fresh facts to be investigated and go to the root of the matter, ld. AR of the assessee prayed that the same may be admitted in view of the judgement of NTPC Ltd. vs. CIT, (1998) 229 ITR 383 (SC).

5. On the other hand, ld. DR for the Revenue has no objection of admitting the additional ground of appeal being purely legal issue.

6. In view of the reliance made by the ld. AR for the assessee on the judgment of Hon’ble Supreme Court in the case of NTPC Ltd. (supra) and issue being purely legal, we proceeded to admit the additional ground of appeal being a legal issue.

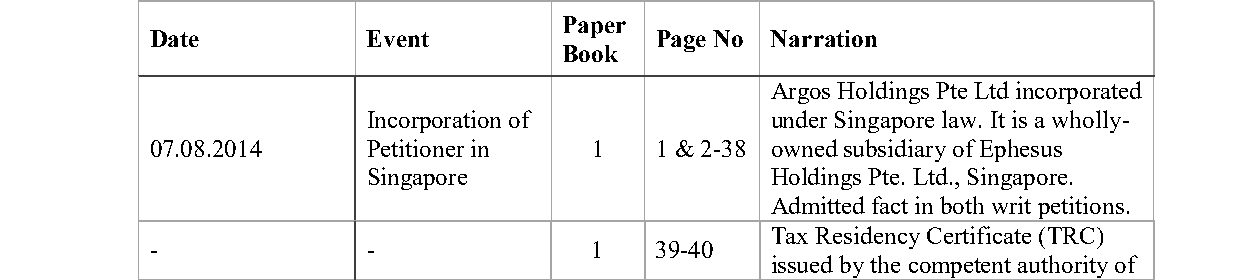

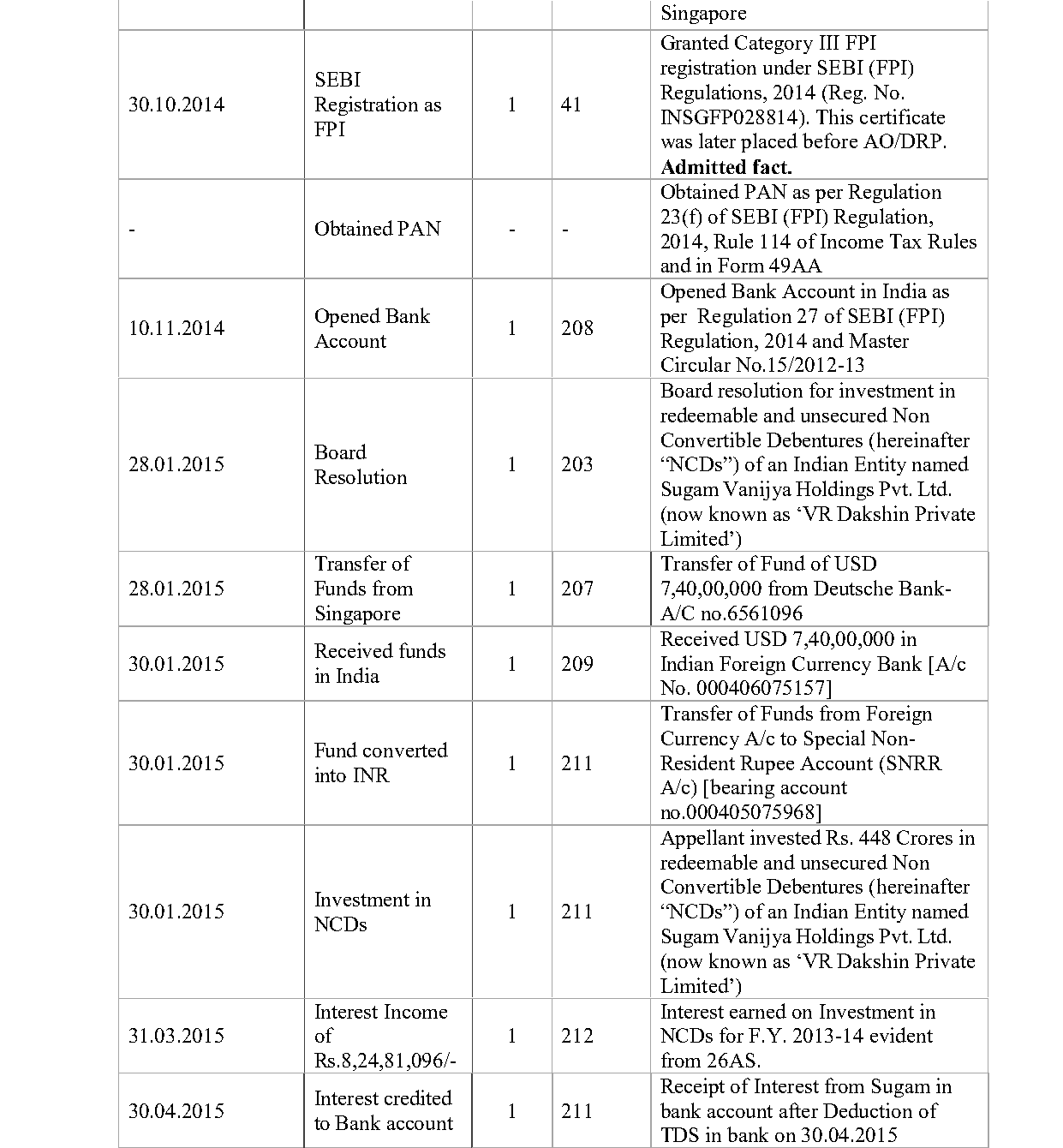

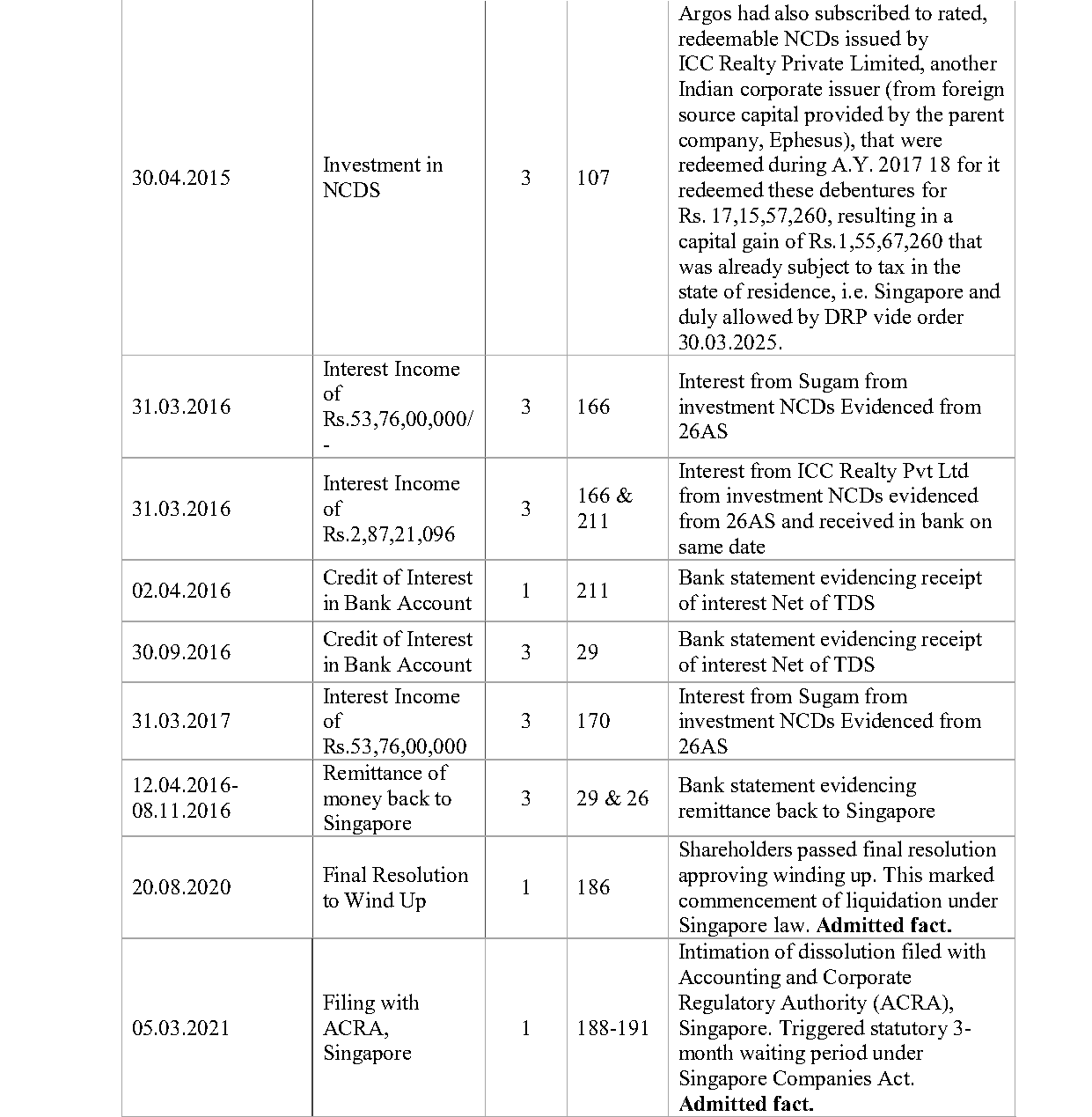

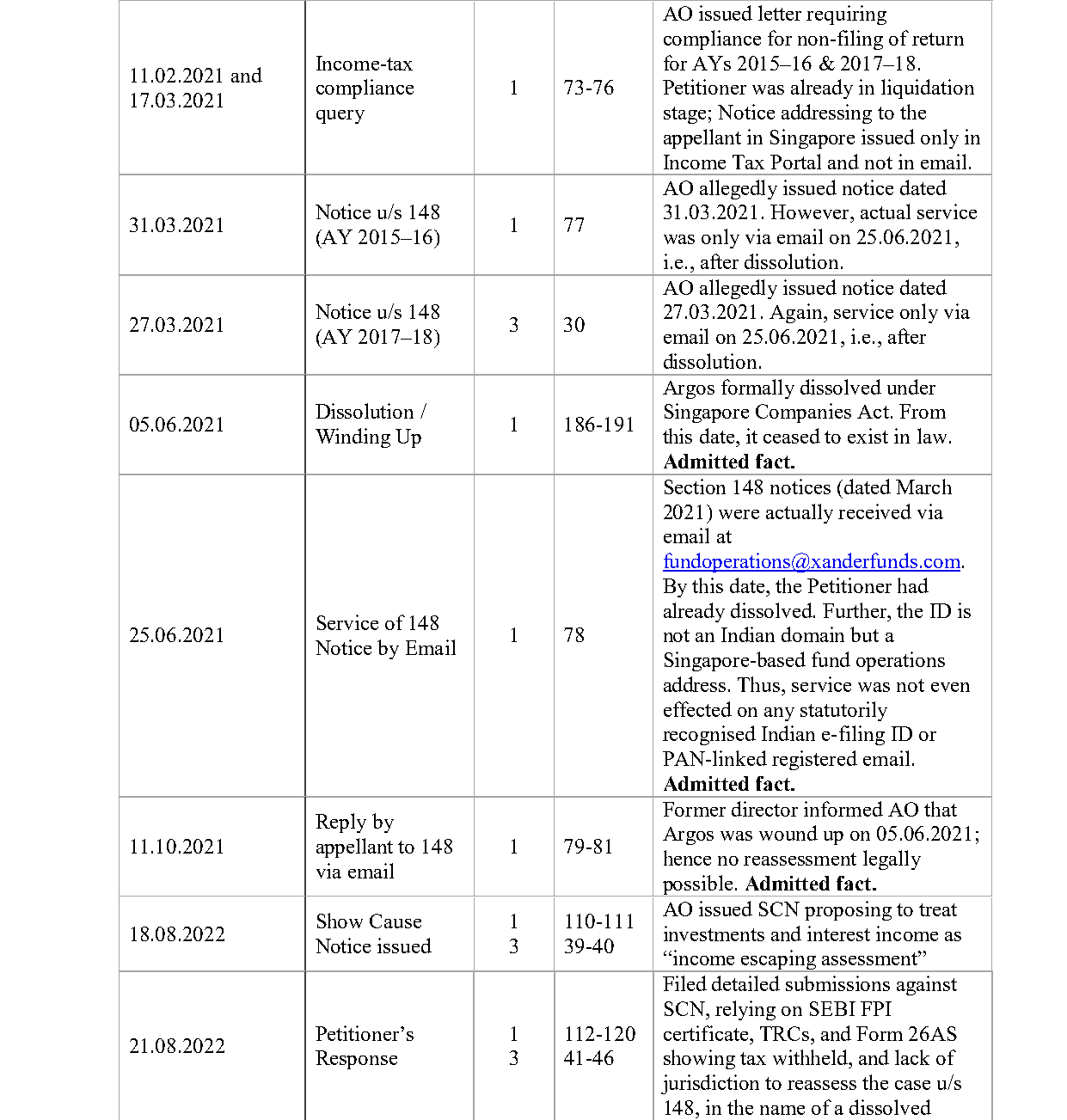

7. Brief facts of the case are, the Assessing Officer observed that the information was flagged on Non-filers Management System of the Income Tax Department. According to which the assessee has entered transactions during the FY 2014-15 relevant to AY 2015-16 as under:-

8. He observed that assessee had not filed the return of income for AY 2015-16, in view of the above, the Assessing Officer formed reason to believe that income had escaped assessment, accordingly, the case was reopened by issue of

An indispensable Tool for Legal Professionals, Endorsed by Various High Court and Judicial Officers

Please visit our Training & Support

Center or Contact Us for assistance

Scan Me!

India’s Legal research and Law Firm App, Download now!

For Daily Legal Updates, Join us on :