INCOME TAX APPELLATE TRIBUNAL (MUMBAI BENCH)

Shri Pawan Singh, J, Shri Prabhash Shankar, ACJ

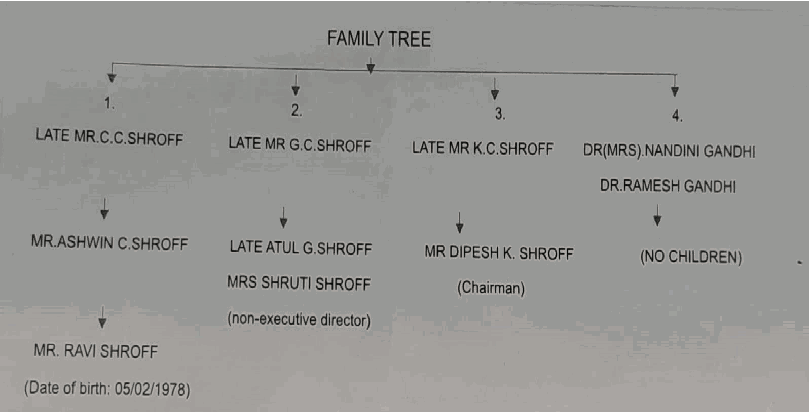

Ravi Shroff – Appellant

Versus

Assistant Commissioner of Income Tax- Circle 32(1), Mumbai – Respondent

1. This appeal by the assessee is directed against the order of NFAC/Learned Commissioner of Income Tax [Ld. CIT(A)] dated 22.09.2023 for A.Y. 2015-16. The assessee in its appeal has raised following ground of appeal:-

“Based on the facts and circumstances of the case, the Appellant respectfully craves to prefer an appeal against the order dated 22 September 2023 passed under section 250 of the Income-tax Act, 1961 (the Act), by the Commissioner of Income-tax (Appeals), National Faceless Appeal Centre, Delhi [CIT(A)] in respect of the appeal filed against the assessment order dated 27 December 2017 passed under section 143(3) of the Act, on the following grounds, each of which are without prejudice to one another

1. Consideration received in respect of sale of shares taxed as business income:

1.1. On the facts and in the circumstances of the case and in law, the CIT(A) erred in upholding the action of the Assessing Officer (AO) in taxing the entire consideration received on sale of shares of Hyderabad Chemicals Lid (HCL) held as an investment since the last 35 years to Nihon Nohyaku Co. Ltd (NNCL) pursuant to a Share Purchase Agreement (SPA) under the head "Profits and Gains of Busine

An indispensable Tool for Legal Professionals, Endorsed by Various High Court and Judicial Officers

Please visit our Training & Support

Center or Contact Us for assistance

Scan Me!

India’s Legal research and Law Firm App, Download now!

For Daily Legal Updates, Join us on :