INCOME TAX APPELLATE TRIBUNAL (MUMBAI BENCH)

Shri Sakthijit Dey, VP, Ms Padmavathy S, AM

GIA India – Appellant

Versus

The Income Tax Officer – Respondent

Income Tax Appeal

| Table of Content |

|---|

| 1. facts regarding the appellant's educational activities (Para 1 , 2) |

| 2. arguments regarding the nature of educational activities (Para 3 , 4 , 5 , 6) |

| 3. court's observations on educational qualifications and provisions (Para 8 , 9 , 10 , 11) |

| 4. clarification on the definition of education as per law (Para 12 , 13 , 14) |

| 5. key conclusions on educational status for tax exemption (Para 15) |

| 6. final decision and directions for appealed issues (Para 18 , 19 , 21) |

ORDER

Per Bench:

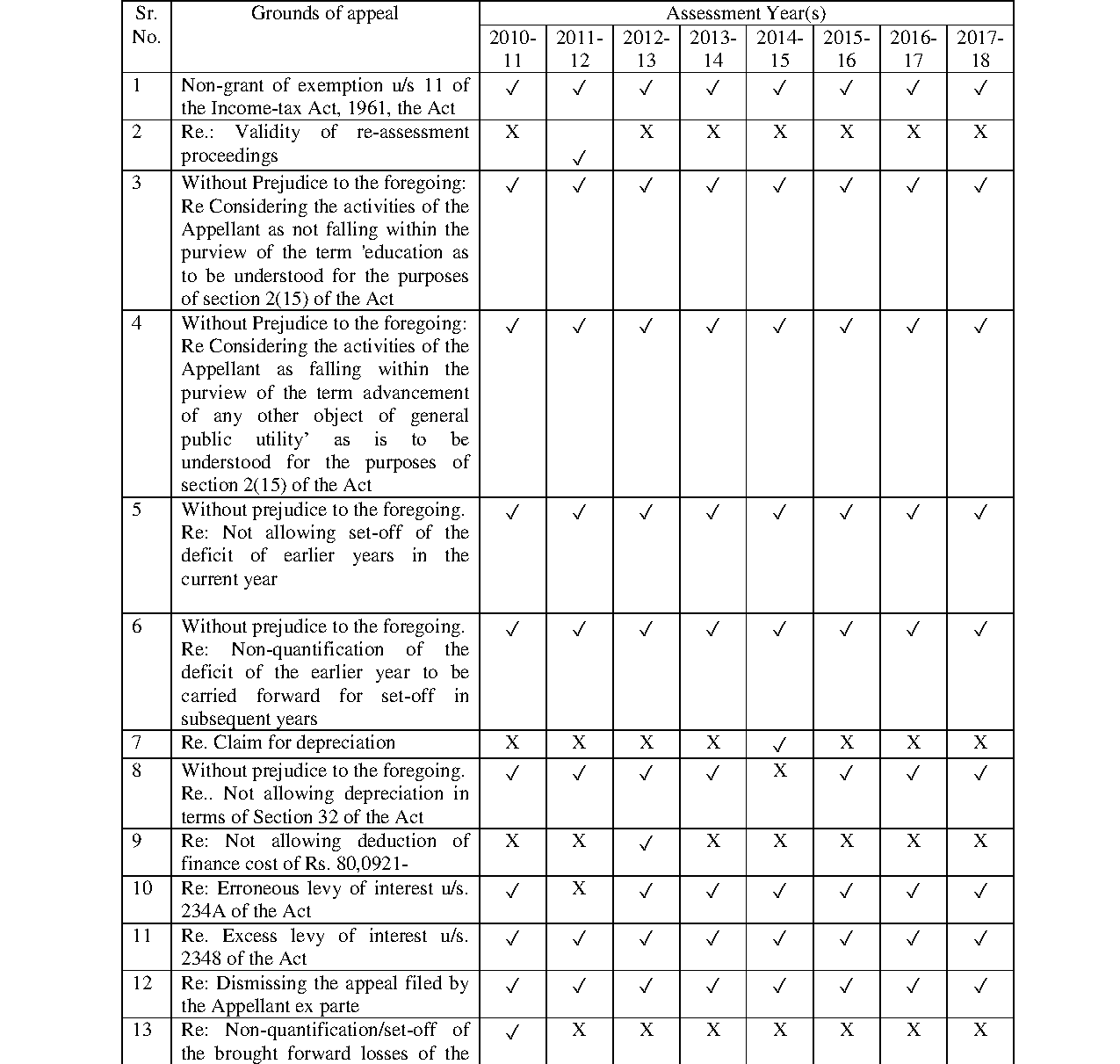

These appeals by the assessee are against the separate orders of the Commissioner of Income Tax Appeals/National Faceless Appeal Centre (NFAC), Delhi passed u/s. 250 of the Income Tax Act, 1961 (the 'Act') for AYs 2010-11 to 2017-18. The issues contended by the assessee in all these appeals are common and therefore these appeals are heard together and disposed of through this common order. For the purpose of adjudication AY 2010-11 is considered as the lead case.

2. The assessee is a company registered u/s. 25 of the Companies Act, 1956 and is a non-profit entity setup for imparting education in the field of gemmology, applied jewellery arts, jewellery design and manufacturing arts of diamond jewellery, coloured stones or other specialities and gems and jewellery business management through schools/institutes or otherwise. The assessee filed the return of income for AY 2010-11 on 13.10.2010 declaring a loss of Rs. 2,65,30,349/-. The case was selected for scrutiny and the statutory notices were duly served on the assessee. During the course of hearing the AO called on the assessee to furnish details of courses conducted during the FY 2009-10 and the fees received against it. The AO further required the assessee to furnish details regarding the duration of the courses and other information in relation to the courses conducted by the assessee. After perusing the various details furnished by the assessee the AO held that the activities of the assessee are for advancement of general public utility in nature and is hit by the First Proviso to Section 2 (15) of the Act,as the assessee has undertaken activities in the nature of business and the services in relation to business industry of gems and jewellery. The AO issue a show cause notice requiring the assessee to explain as to why its case is not hit by Section 11 (4) and First Proviso to (15) of the Act. The assessee submitted before the AO that the activities undertaken are for "imparting education" amongst the students in the field of gemmology, applied jewellery arts, jeweller design etc., and cannot fall within the purview of the term "advancement of any other object of general public utility" where by the proviso to (15) is not applicable. The AO did not accept the submissions of the assessee and held that the assessee is not conducting any course in formal education nor it is affiliated to any registered authority. The AO further held that the assessee has not conducted any composite or integrated courses of organised and systematic training and the duration of the course range from 1 day to 6 months which are basically professional and industrial training and skill courses for wholesale and retail manufacturers sales persons etc. The AO also held that the assessee is not authorised to issue any degree or diploma certificate upon completion of the course and even no formal examination is conducted. Accordingly, the AO held that the activities of the assessee cannot be held as "imparting of education" and that the assessee has carried on commercial activities in the name of education. The AO assessed the total income based on the income and expenditure account amounting to Rs. 2,41,61,700/-. Aggrieved the assessee filed further appeal before the ld. CIT(A). The assessee submitted before the ld. CIT(A) that the activities carried on by the assessee are in the field of education and the same is carried out on a systematic and organised manner. The assessee made a detailed submission tabulating

An indispensable Tool for Legal Professionals, Endorsed by Various High Court and Judicial Officers

Please visit our Training & Support

Center or Contact Us for assistance

Scan Me!

India’s Legal research and Law Firm App, Download now!

For Daily Legal Updates, Join us on :