INCOME TAX APPELLATE TRIBUNAL (HYDERABAD BENCH)

SHRI RAVISH SOOD, JM, SHRI MADHUSUDAN SAWDIA, AM

Income Tax Officer – Appellant

Versus

Venkata Ramanamma – Respondent

Income Tax Appeal No.482/Hyd/2025

| Table of Content |

|---|

| 1. assessment initiated due to significant financial transactions. (Para 1 , 2 , 3) |

| 2. arguments on procedural lapses in notice issuance. (Para 4 , 5) |

| 3. consequences of failing to obtain valid authority sanction. (Para 11 , 16) |

| 4. importance of proper authority for notice approval. (Para 12 , 13) |

| 5. final ruling dismissing the appeal due to invalid proceedings. (Para 18) |

ORDER

PER RAVISH SOOD, JM:

The present appeal filed by the revenue is directed against the order passed by the Commissioner of Income Tax (Appeals), National Faceless Appeal Centre, Delhi, dated 31/12/2024, which in turn arises from the order passed by the Assessing Officer (for short, “AO”) under section 147 r.w.s 144 r.w.s 144B of the Income Tax Act, 1961 (for short, “the Act”), dated 19/02/2024 for the Assessment Year 2018–19. The revenue has assailed the impugned order on the following grounds of appeal before us:

(i) Whether the Ld. CIT(A) is correct in allowing the assessee's appeal on 31.12.2024 relying on the order dated 01.10.2024 of the Hon'ble ITAT, Mumbai, which in turn relied on the judgement of Hon'ble Bombay High Court in Siemens Financial Services (P.) Ltd. v/s DCIT, (2023) 457 ITR 647 (Bom.), which was overturned by the Hon'ble Supreme Court vide judgement dated 03.10.2024 in TOLA case in Civil Appeal No. 8629 of 2024?

(ii) Whether the order of the Ld. CIT(A) is correct in quashing the notice u/s. 148 of the Act when the show cause notice u/s. 148A(b) was issued before 31.03.2022 and order u/s 148A(d) & notice u/s 148 were also issued on 07-04-2022 ie. within the time limits prescribed by the Act, with the prior approval of the Pr. Commissioner of Income Tax, Tirupati, being Specified Authority u/s. 151 of the Act?

(iii) Whether the order of the Ld. CIT(A) is correct in violating the Rule 46 of Income Tax Rules, 1962, by not calling for Remand Report even though the assessee filed new submissions during the appellate proceedings which were not furnished before the AO?

(iv) In this case as the show cause notice u/s 148A(b) was issued within three years from the end of the relevant A.Y. 2018-19 and the specified Authority is the Pr. CIT, Tirupati only and not the Pr. CCIT/CCIT as mentioned in the order. Hence the order of the CIT(A) in quashing notice uls 148 on the ground that it is not approved by the specified authority is not acceptable.

(v) Any other additional ground that may be urged at the time of the appeal hearing.

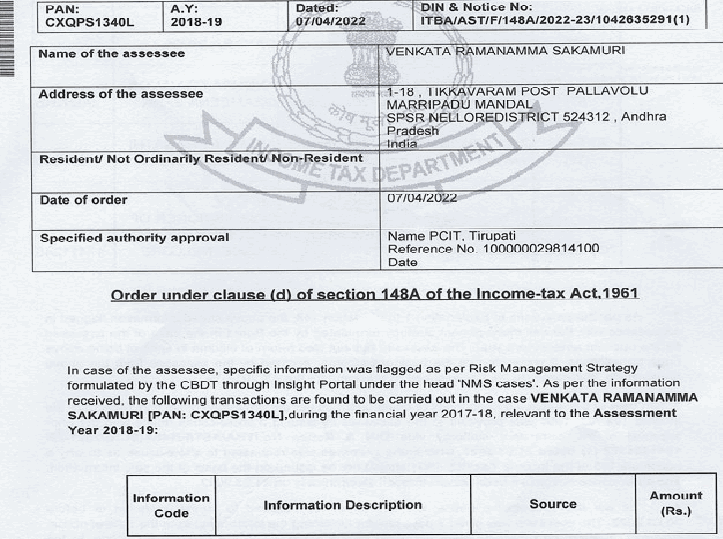

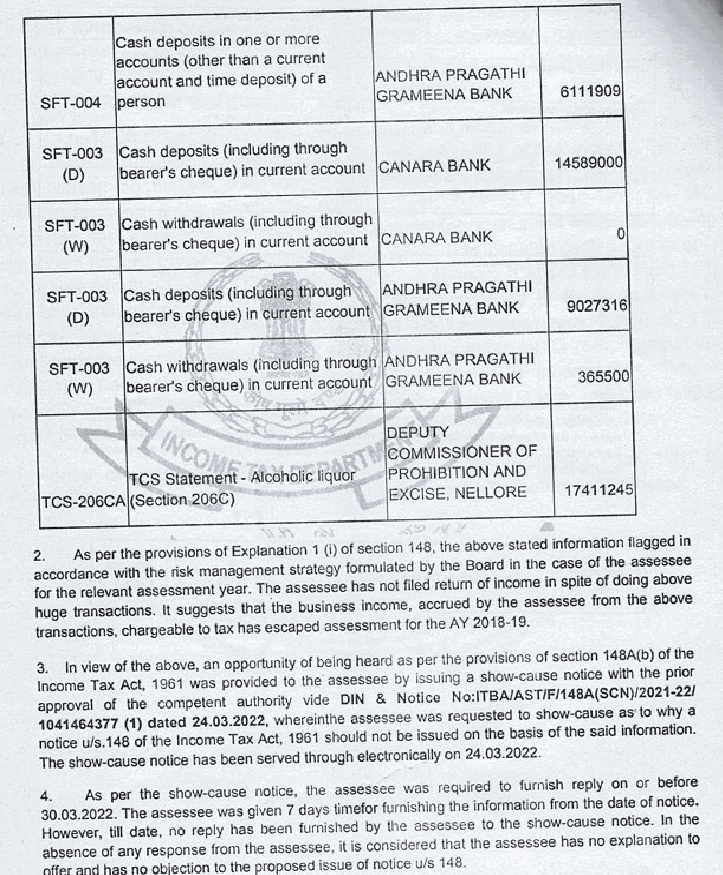

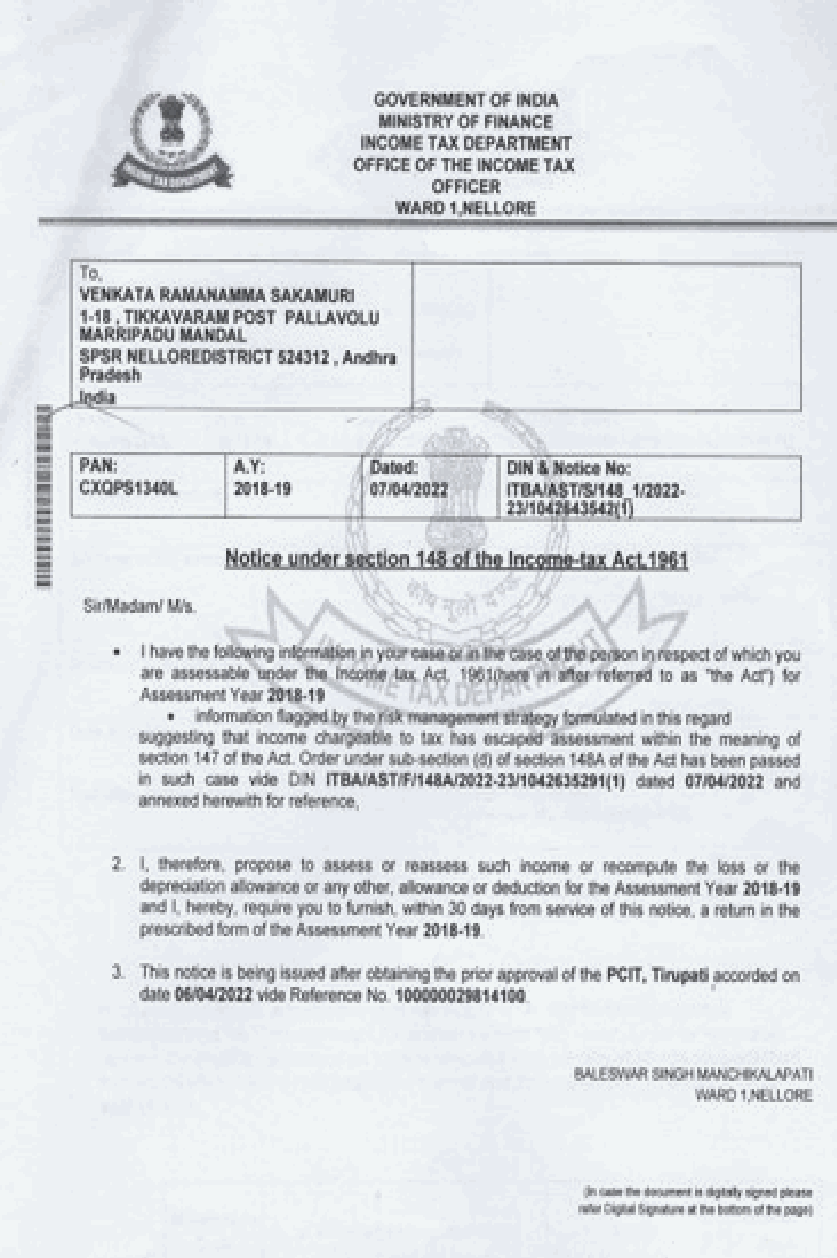

2. Succinctly stated, the AO based on information that the assessee during the subject year had carried out financial transactions of cash deposit, cash withdrawals and purchases of liquor, viz., (i) Cash deposits in bank account maintained with Andhra Pragati Grameena Bank: Rs.1,51,39,225/-; (ii) cash deposits in bank account with Canara Bank: Rs.1,45,89,000/-; (iii) cash withdrawals from bank account maintained with Andhra Pragati Grameena Bank: Rs. 3,65,500/-; and (iv) tax collected at source (TCS) on transaction of liquor with DEP Commissioner of Prohibition and Excise, Nellore: Rs.1,74,11,245/-, but had not filed his return of income for the subject year, issued notice under section 148 of the Act.

3. Thereafter, the AO vide his order passed under section 147 r.w.s.144 r.w.s. 144B of the Act, dated 19/02/2024 determined the income of the assessee at Rs. 3,53,21,425/- after making certain additions, viz., (i) addition on account of cash deposits/cash withdrawals made in bank accounts: Rs.3,35,80,300/-; and (ii) addition from business or profession: Rs.17,41,125/-.

4. Aggrieved, the assessee carried the matter in appeal before the CIT(A). It was, inter alia, the claim of the assessee before the CIT(A) that as the AO had reopened his case vide notice issued under section 148 of the Act, dated 07/04/2022 i.e., beyond the period of three years from the end of the relevant assessment year without obtaining the approval of the appropriate authority as envisaged under section 151(ii) of the Act, therefore, the impugned asse

An indispensable Tool for Legal Professionals, Endorsed by Various High Court and Judicial Officers

Please visit our Training & Support

Center or Contact Us for assistance

Scan Me!

India’s Legal research and Law Firm App, Download now!

For Daily Legal Updates, Join us on :