INCOME TAX APPELLATE TRIBUNAL (MUMBAI BENCH)

SHRI AMIT SHUKLA, J, SHRI ARUN KHODPIA, ACJ

M/s. Oceanic Marketing – Appellant

Versus

DCIT (OSD) Agencies India Ltd. – Respondent

| Table of Content |

|---|

| 1. delay in filing appeal due to lack of awareness of appellate order. (Para 1 , 2 , 3 , 4 , 5) |

| 2. justification for delays in filing appeals must consider all involved circumstances. (Para 10 , 11) |

| 3. assessee demonstrated intentions in holding shares as investments. (Para 12 , 20) |

| 4. investment versus trading is determined by the intention and actions of the assessee. (Para 13 , 14 , 15 , 16 , 18) |

| 5. appeal allowed and evaluated on merits. (Para 22) |

आदेश/ORDER

PER AMIT SHUKLA (J.M):

These appeals have been preferred by the assessee challenging the order dated 23 January 2012 passed by the learned Commissioner of Income Tax Appeals- 5 Mumbai for assessment year 2008-09. Two appeals had inadvertently been filed against the same order. At the very outset the learned counsel for the assessee fairly submitted that one of them was filed by mistake and may be treated as withdrawn. Accordingly ITA No. 4542 Mum 2025 is dismissed as withdrawn and only No. 4777 Mum 2025 survives for adjudication.

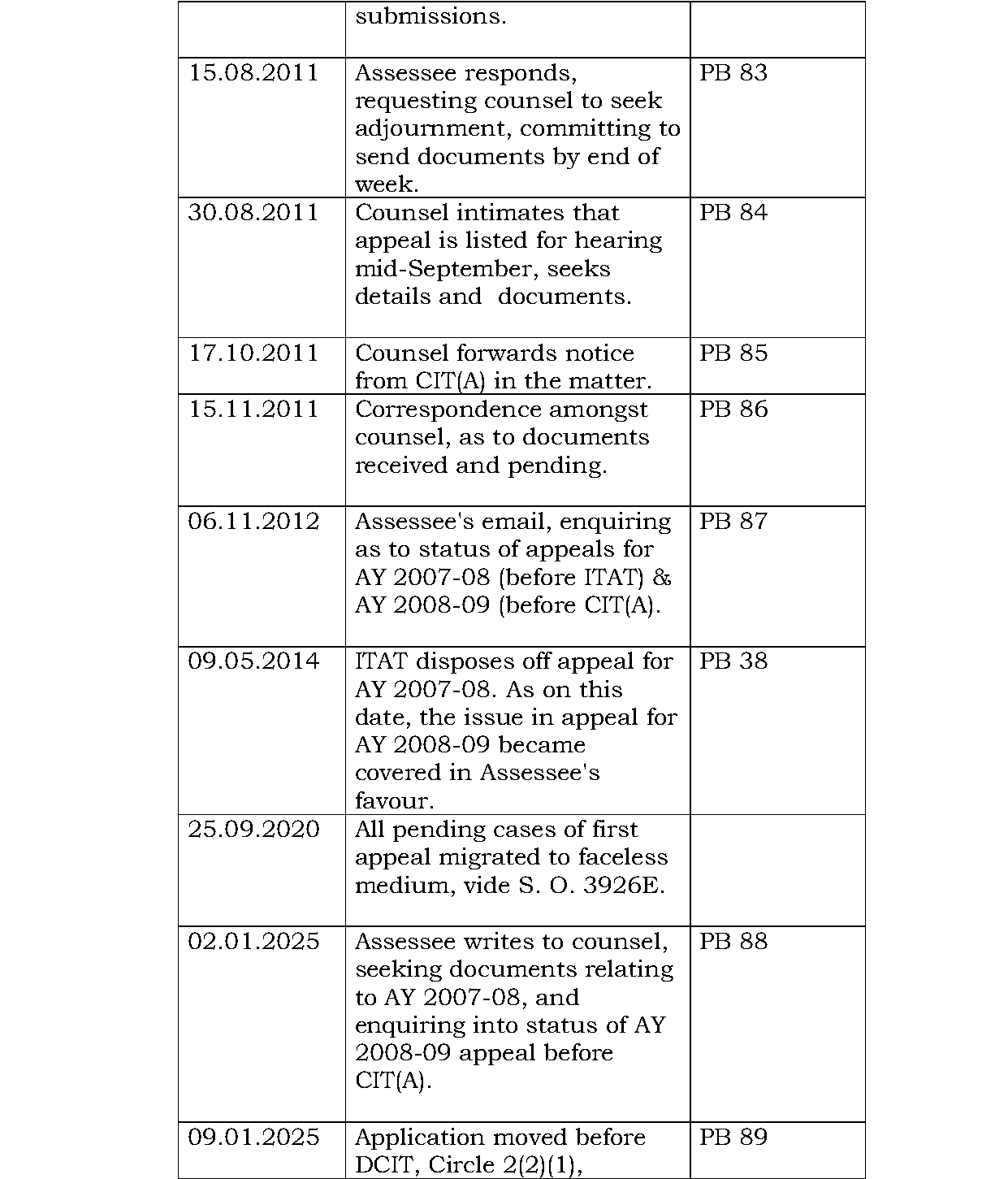

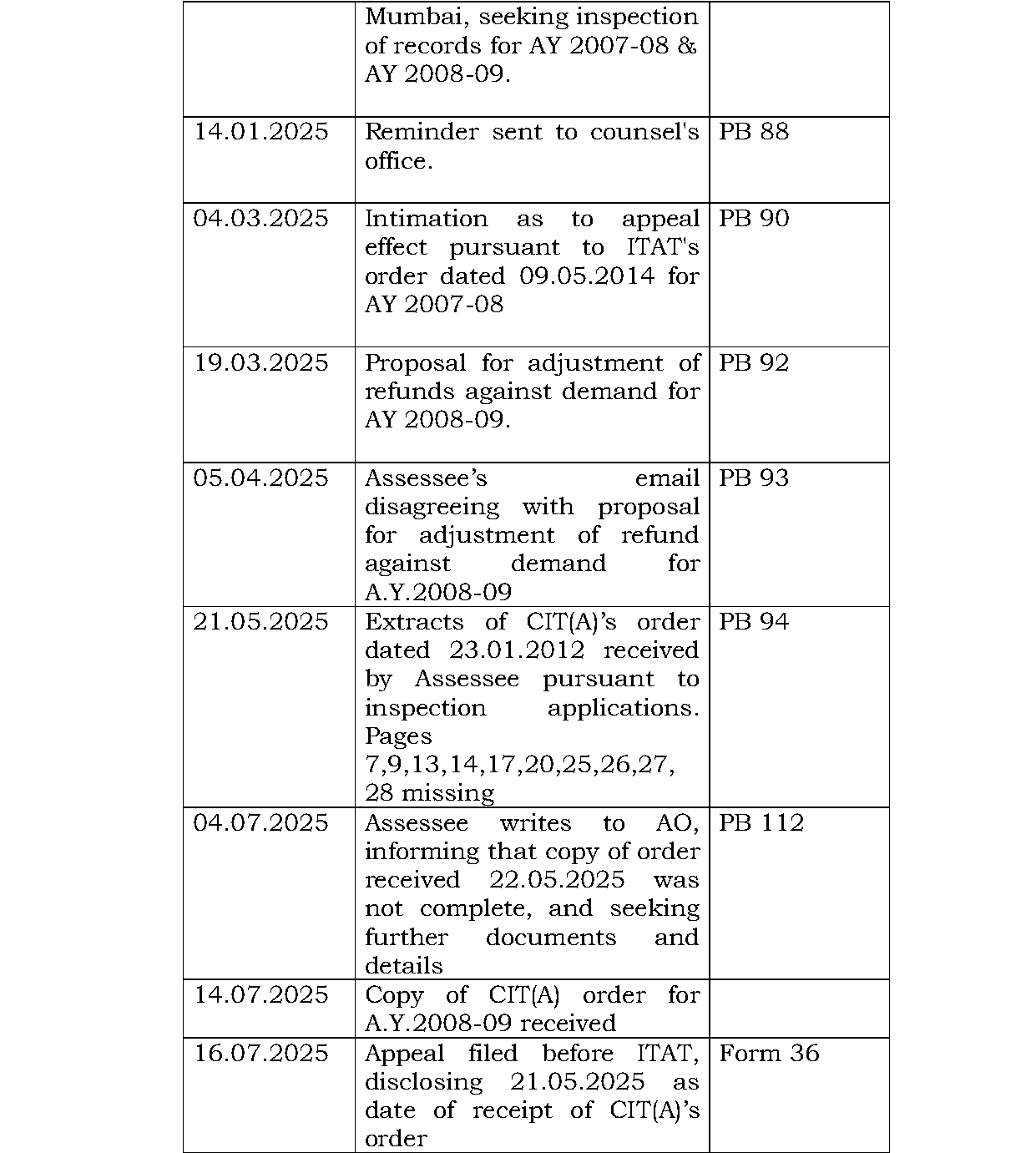

2. The assessee seeks condonation of delay of 4855 days in filing the surviving appeal. The learned counsel for the assessee submitted that the assessee was never aware that the order

An indispensable Tool for Legal Professionals, Endorsed by Various High Court and Judicial Officers

Please visit our Training & Support

Center or Contact Us for assistance

Scan Me!

India’s Legal research and Law Firm App, Download now!

For Daily Legal Updates, Join us on :