INCOME TAX APPELLATE TRIBUNAL (HYDERABAD BENCH)

SHRI VIJAY PAL RAO, VP, SHRI MADHUSUDAN SAWDIA, AM

Praveen Kumar – Appellant

Versus

The Income Tax Officer – Respondent

| Table of Content |

|---|

| 1. challenging reassessment validity (Para 1 , 2) |

| 2. arguments on authority for reassessment (Para 3 , 4) |

| 3. court findings on compliance with law (Para 5 , 6) |

| 4. final ruling on appeal outcome (Para 7 , 8) |

आदेश/ORDER

PER VIJAY PAL RAO, VICE PRESIDENT :

This appeal by the Assessee is directed against the order dated 30.06.2025 of learned CIT(A)-National Faceless Appeal Centre [in short “NFAC], Delhi, for the assessment year 2017-2018.

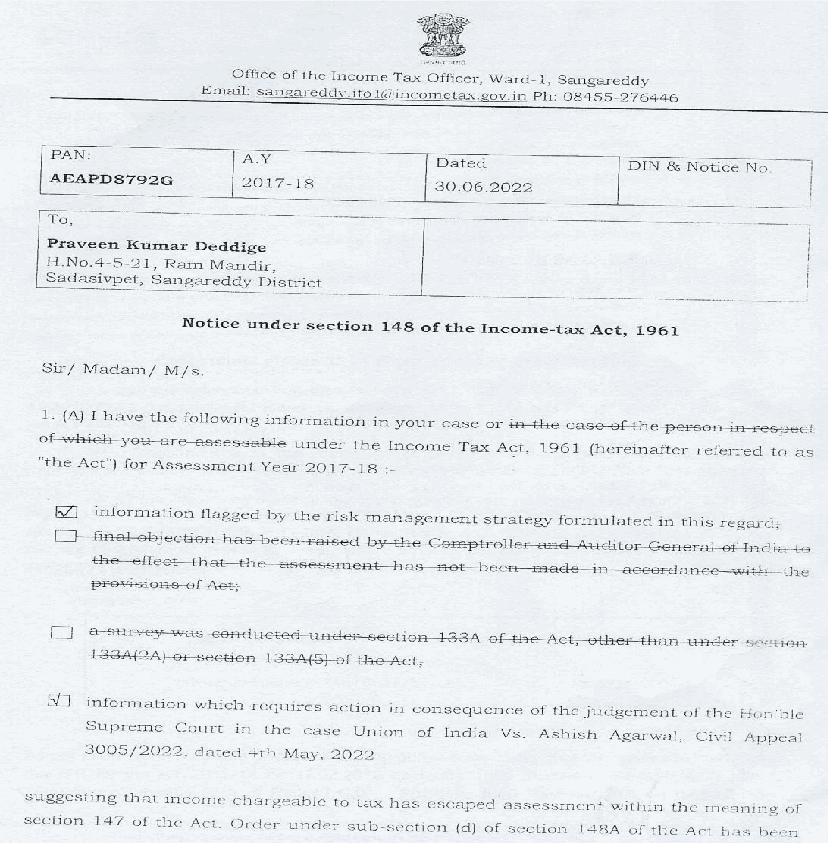

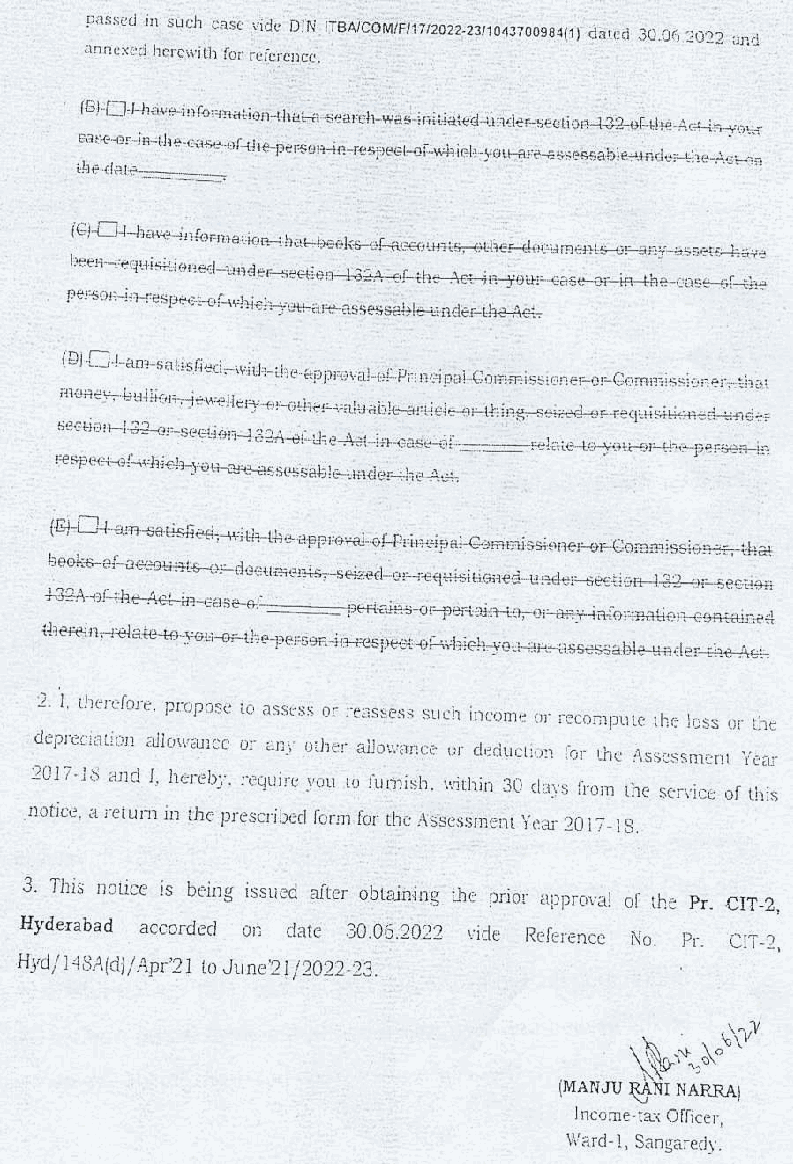

2. The assessee has raised the following grounds : 1. “The learned CIT(A) failed to consider the additional ground and submissions filed on 17.06.2025, wherein the appellant challenged the validity of reassessment u/s 147, since the notice u/s 148 was issued without the valid sanction mandated u/s 151, rendering the reassessment void ab initio.

2. The learned CIT(A) failed to appreciate that the notice u/s 148 issued by the Jurisdictional AO was in contravention of the Faceless Assessment/ Reassessment Scheme notified by CBDT, thereby rendering the reassessment void ab initio.

3. The learned CIT(A) failed to appreciate the fact that the notice u/s.148 did not contain a valid Document Identification Number (DIN) as mandated by CBDT Circular No.1

An indispensable Tool for Legal Professionals, Endorsed by Various High Court and Judicial Officers

Please visit our Training & Support

Center or Contact Us for assistance

Scan Me!

India’s Legal research and Law Firm App, Download now!

For Daily Legal Updates, Join us on :