INCOME TAX APPELLATE TRIBUNAL (MUMBAI BENCH)

SHRI OM PRAKASH KANT, ACM, SHRI RAJ KUMAR CHAUHAN, J

Mr. Bhausaheb B. Pansare – Appellant

Versus

Revenue – Respondent

| Table of Content |

|---|

| 1. factual background regarding income and disputed transactions. (Para 2) |

| 2. arguments related to improper notification and verification. (Para 3) |

| 3. consideration of evidence and verification by authorities. (Para 4) |

| 4. need for comprehensive verification based on presented evidence. (Para 5) |

ORDER

This appeal by the Assessee is directed against the order dated 31st July, 2025 passed by the Ld. Commissioner of Income-Tax (Appeals)-National Faceless Appeal Centre, Delhi (in short the Ld. CIT (A)), for Assessment Year 2023-24, raising following grounds:-

“GROUND NO. 1:

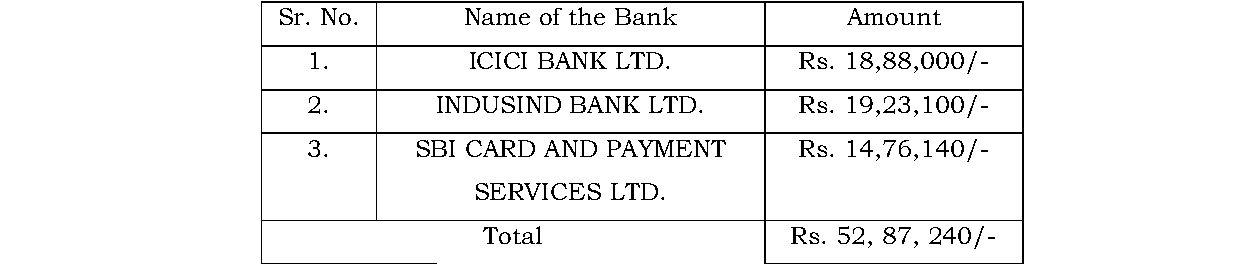

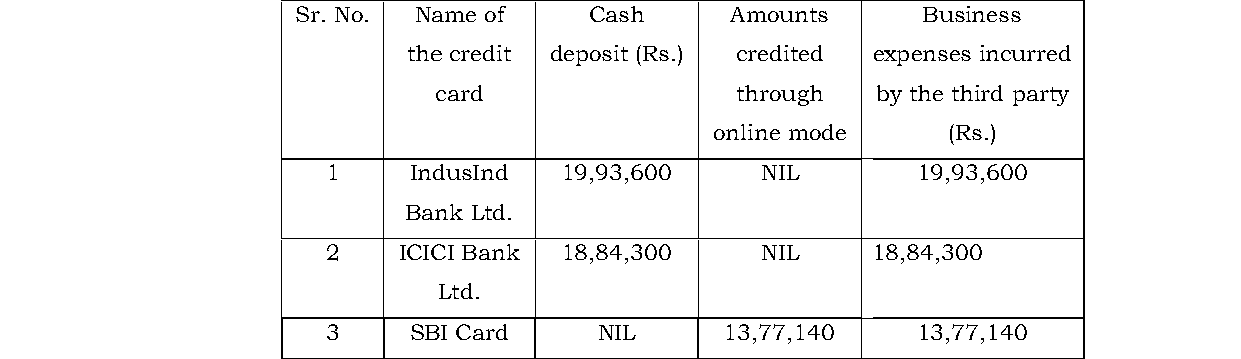

The Commissioner of Income Tax (Appeals), National Faceless Appeal Centre (hereinafter referred to as the CIT(A)NFAC] erred in confirming the addition of Rs. 52,87,240/- made by the AO under section 69C of the Act.

The Appellant submits that the CIT(A) confirmed the said addition made by the AO without appreciating the fact that the Appellant had sufficiently explained with supporting documentary evidences and third-party undertaking/confirmations to prove the genuinity of his claim that the said credit card transactions aggregating to Rs. 52,87,240/- were not carried out by him but were carried out by one of

An indispensable Tool for Legal Professionals, Endorsed by Various High Court and Judicial Officers

Please visit our Training & Support

Center or Contact Us for assistance

Scan Me!

India’s Legal research and Law Firm App, Download now!

For Daily Legal Updates, Join us on :