INCOME TAX APPELLATE TRIBUNAL (DELHI BENCH)

SHRI ANUBHAV SHARMA, JM, SHRI MANISH AGARWAL, AM

Shokeen Construction Co. – Appellant

Versus

DCIT – Respondent

| Table of Content |

|---|

| 1. procedural integrity in initiation of income assessments. (Para 4 , 5 , 8) |

| 2. judicial requirement for independent judgment in satisfaction recording. (Para 10 , 13 , 18) |

| 3. final ruling on appeals allowed based on procedural invalidity. (Para 19 , 22 , 26) |

ORDER

PER MANISH AGARWAL, AM :

The captioned appeals are filed by assessee against the different orders, all dated 16.12.2024 passed by Ld. Commissioner of Income Tax (A)-30, New Delhi [“Ld. CIT(A)”] in Appeal No. 30/10343/2017-18; Appeal No.30/10575/2018-19; and Appeal No. 30/10736/2019-20 passed u/s 250 of the Income Tax Act, 1961 [“the Act”] arising out of assessment orders, all dated 20.03.2023 passed u/s 153C r.w.s. 143(3) of the Act pertaining to assessment year 2018-19 to 2020-21 respectively.

2. As these captioned appeals filed by the assessee have similar issues which are inter-linked, inter-connected and this fact has been admitted by both the parties during the course of hearing before us, therefore, these three appeals filed by the assessee are decided by a common order.

3. First we take up the appeal of assessee in ITA No.5971/Del/2024 for Assessment Year 2018-19.

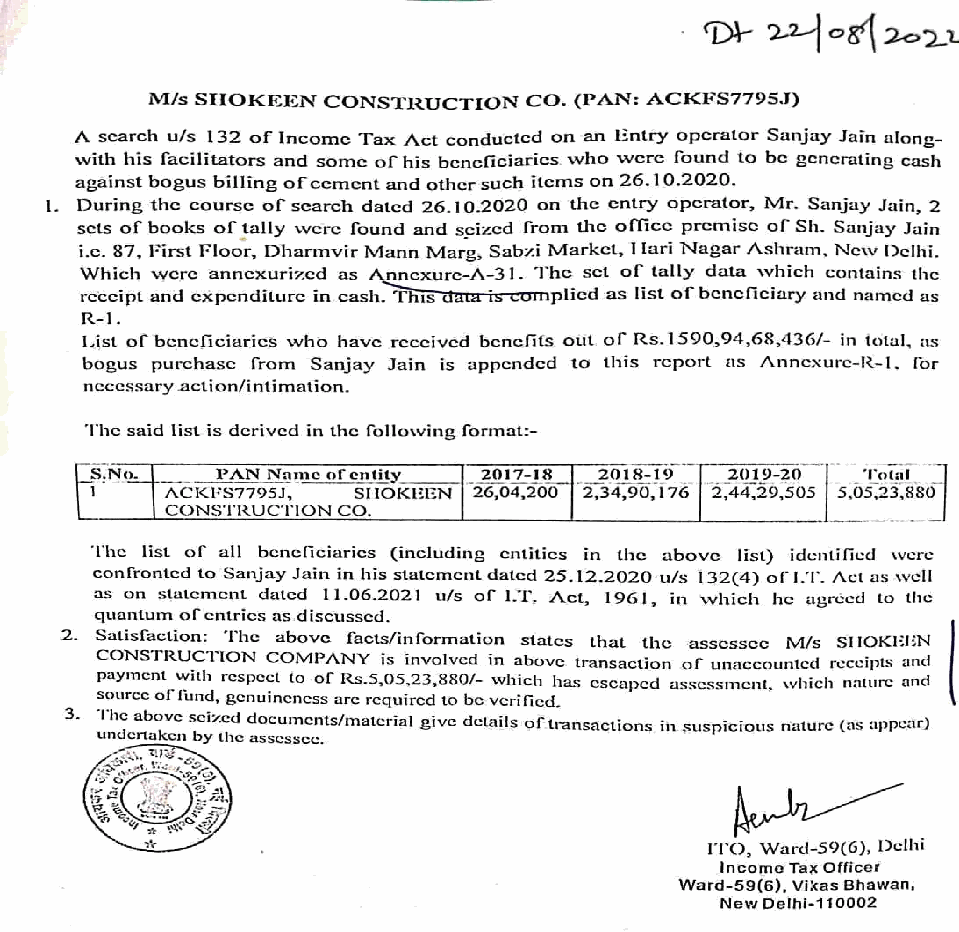

4. Brief facts of the case are that a

An indispensable Tool for Legal Professionals, Endorsed by Various High Court and Judicial Officers

Please visit our Training & Support

Center or Contact Us for assistance

Scan Me!

India’s Legal research and Law Firm App, Download now!

For Daily Legal Updates, Join us on :