INCOME TAX APPELLATE TRIBUNAL (DELHI BENCH)

SHRI MAHAVIR SINGH, VP, SHRI MANISH AGARWAL, AM

Mohd. Alam Quershi – Appellant

Versus

Income Tax Officer – Respondent

ITA No.3986/Del/2025

| Table of Content |

|---|

| 1. background of case reopening. (Para 2 , 3 , 4) |

| 2. arguments on compliance and procedural errors. (Para 6 , 7) |

| 3. court's validation of procedural limitations. (Para 8 , 9) |

| 4. final conclusion of appeal acceptance. (Para 10) |

ORDER

PER MANISH AGARWAL, AM:

This appeal is filed by the assessee against the order of Ld. Commissioner of Income Tax (Appeals), National Faceless Appeal Centre (NFAC), Delhi [CIT(A) in short], dated 17.02.2025 in Appeal No. NFAC/2014-15/10282979 arising out of the assessment order passed u/s 147 r.w.s. 144 dated 19.05.2023 for Assessment Year2015-16.

2. Brief facts of the case are that case of the assessee was reopened on the basis of information received that there were larger credits in the bank account of the assessee and there is mismatch in the income declared by the assessee and credits in the bank account and accordingly, notice u/s 148 was issued on 06.04.2021. Thereafter, in terms of the order of Hon’ble Supreme Court in the case of Union of India vs. Ashish Agarwal and Ors. in Civil Appeal No. 3005/2002, the said notice was treated as notice u/s 148A(2) of the Act. After passing the order u/s 148A(d) of the Act, a fresh notice u/s 148 was issued on 29.07.2022. In response, the assessee filed the return on 28.08.2022 declaring total income of Rs. 3,90,230/-. The assessment was completed u/s 147 r.w.s. 144B at an income of Rs. 58,64,382/- by making addition of Rs. 54,74,132/-.

3. Against the said order, the assessee filed an appeal before the Ld. CIT(A) who dismissed the appeal of the assessee.

4. Aggrieved by the said order, the assessee is in appeal before the Tribunal.

5. The appeal filed by the assessee is delayed by 49 days for which an application for condonation of delay was filed. As per said petition, it was stated that the assessee was engaged one Chartered Accountant for filing the appeal before the Ld. CIT(A) and was in continuous touch with the Counsel to find out the progress in the appeal. When in the month of April, the assessee approached the counsel, it was stated by that appeal was decided against the assessee and, further appeal is to be filed after payment of fees of Rs.10,000/-. Accordingly, the assessee has deposited appeal fees of Rs. 10,000/- on 21.04.2025 however, the appeal could only be filed on 18.06.2025 as the Counsel had got ill and could not filed appeal in time. In this respect, an affidavit was also filed re-affirming these facts and requested that delay be condoned and appeal be admitted. After considering the submissions of both parties, we finds that the reasons stated in the petition have not been found to be false and it is also a matter of fact that the assessee would not gain anything by filing the appeal late. There is no mala fide imputable to the assessee. Accordingly, we condoned the delay in the instant appeal and admit the same for adjudication.

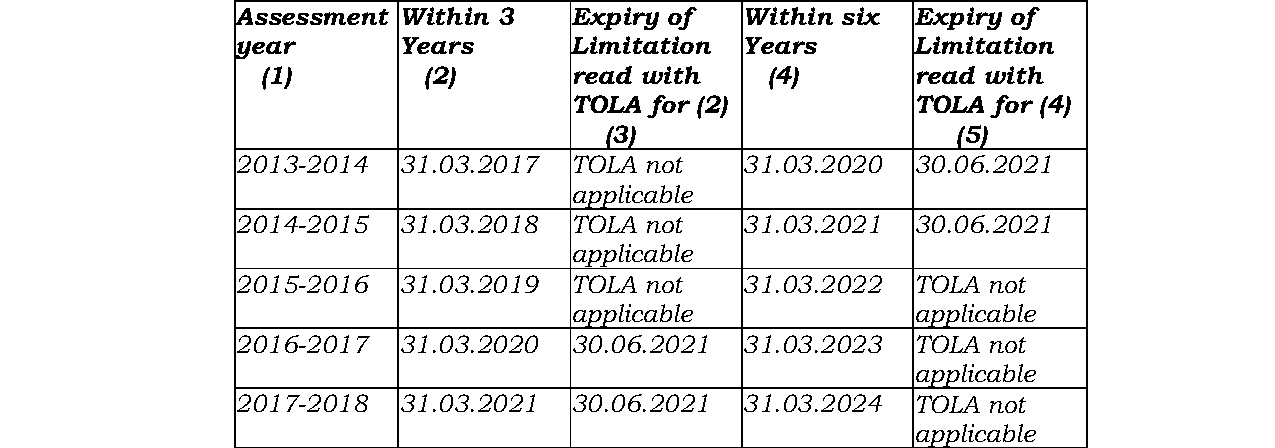

6. Before us, ld. AR for the assessee submits that first notice for reopening u/s 148 of the Act was issued on 06.04.2021 and thereafter in terms of the procedure laid down by the Hon’ble Supreme Court in the case of Union of India vs. Ashish Agarwal (supra), the said notice was treated as the notice issued u/s 148A(b) of the Act. Thereafter the order u/s 148A(d) was passed and fresh notice u/s 148 was issued on 29.07.2022. In the case of Rajiv Bansal vs. Union of India reported in [2024] 469 ITR 46 (SC), the Hon’ble Supreme Court in para 19 has observed that the Revenue has accepted that no notice was issued for reopening for Assessment Year 2015-16, however, the case of the assessee was reopened, accordingly, it is prayed that the notice issued u/s 148 is contrary to the undertaking given by the government before the Hon’ble Supreme Court and consequent reassessment order passed u/s 147 be quashed. Reliance is further placed on the following judgments:

1. UOI Vs. Rajeev Bansal (2024) 469 ITR 46 (SC)

2. IBIBO Group Private Ltd. Vs. ACIT in Delhi High Court order dated 13.12.2024 in W.P. (C) 17639/

An indispensable Tool for Legal Professionals, Endorsed by Various High Court and Judicial Officers

Please visit our Training & Support

Center or Contact Us for assistance

Scan Me!

India’s Legal research and Law Firm App, Download now!

For Daily Legal Updates, Join us on :