INCOME TAX APPELLATE TRIBUNAL (DELHI BENCH)

SHRI ANUBHAV SHARMA, J, SHRI MANISH AGARWAL, ACJ

M/s. Ace Mega Structures Pvt. Ltd. – Appellant

Versus

DCIT – Respondent

ITA No. 4067/Del/2025 | ITA No. 4115/Del/2025

| Table of Content |

|---|

| 1. cross-appeals are linked due to common issues. (Para 1 , 2) |

| 2. revenue's reliance on past statements is inadequate without corroboration. (Para 4 , 5 , 19) |

| 3. assessment conclusions must be based on verified evidence. (Para 6 , 7 , 30) |

| 4. assessor's procedural adherence is crucial for validity of findings. (Para 12 , 28) |

| 5. strong evidentiary basis is needed for tax assessments. (Para 20 , 21) |

ORDER

PER MANISH AGARWAL, AM:

The captioned cross-appeal filed by the Revenue and assessee are arising from order dated 15.04.2025 of the Ld. Commissioner of Income Tax (Appeals)-3, Noida [“Ld. CIT(A)”] passed under s. 250 of the Income Tax Act, 1961 [the Act] emanating from the assessment orders dated 31.03.2024 passed u/s 147 r.w.s. 143(3) of the Act by the Assessing Officer [“AO”] pertaining to AY 2019-20.

2. As the captioned cross-appeals filed by the Revenue and the assessee are having common issues of addition made u/s 68 of the Act, wherein in all the entries of loans received from one company M/s Hallow Securities Pvt Ltd. was doubted and addition was made thus, the issues involved in both appeals are inter-linked, inter-connected. This fact has been admitted by both the parties during the course of hearing before us, therefore, both cross- appeal filed by the Revenue and the assessee are decided by a common order.

ITA No. 4115/Del/2025 (Revenue’s Appeal) [AY 2019-20]

3. First, we are taking the appeal filed by the revenue in ITA No. 4115/Del/2025.

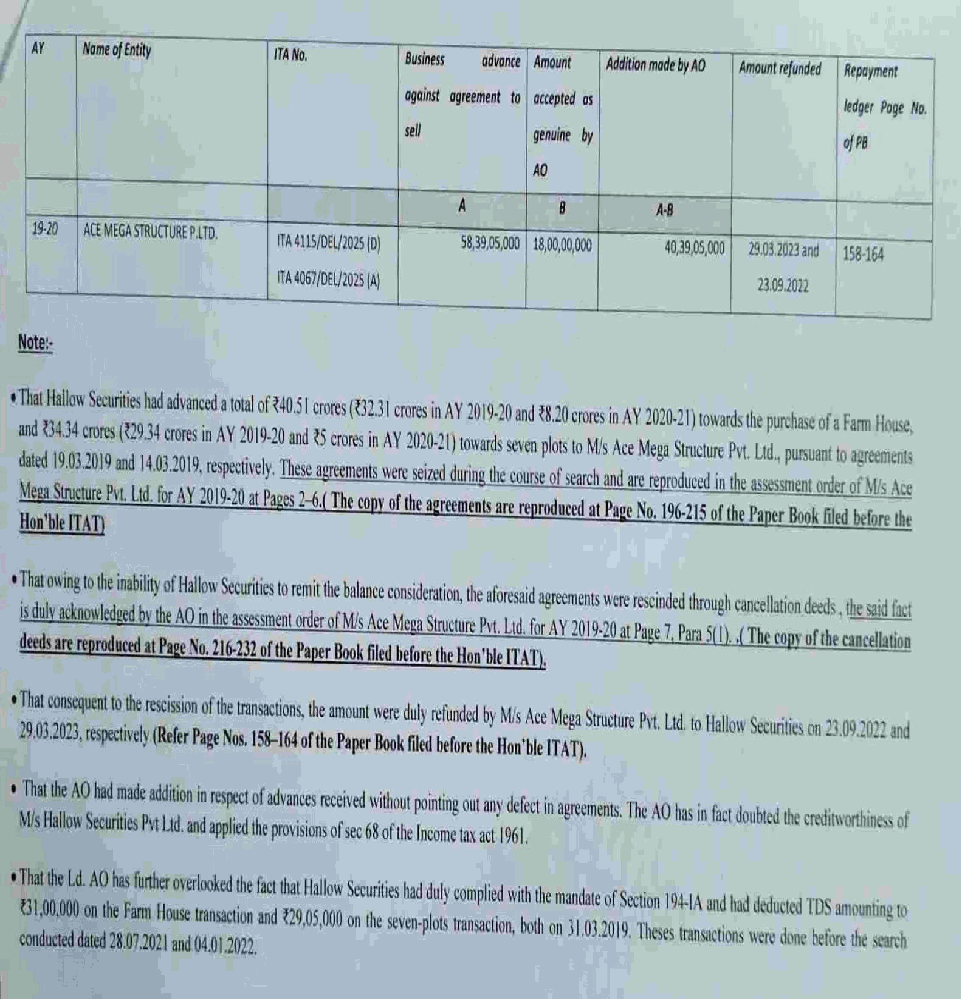

4. In all the grounds of appeal, the revenue has challenged the action of ld. CIT(A) in deleting the addition of Rs. 40,39,05,000/- made by AO towards the advances received on the sale of immovable assets owned by the assessee from M/s Hallow Securities Pvt. Ltd. treating the same as unexplained cash credits.

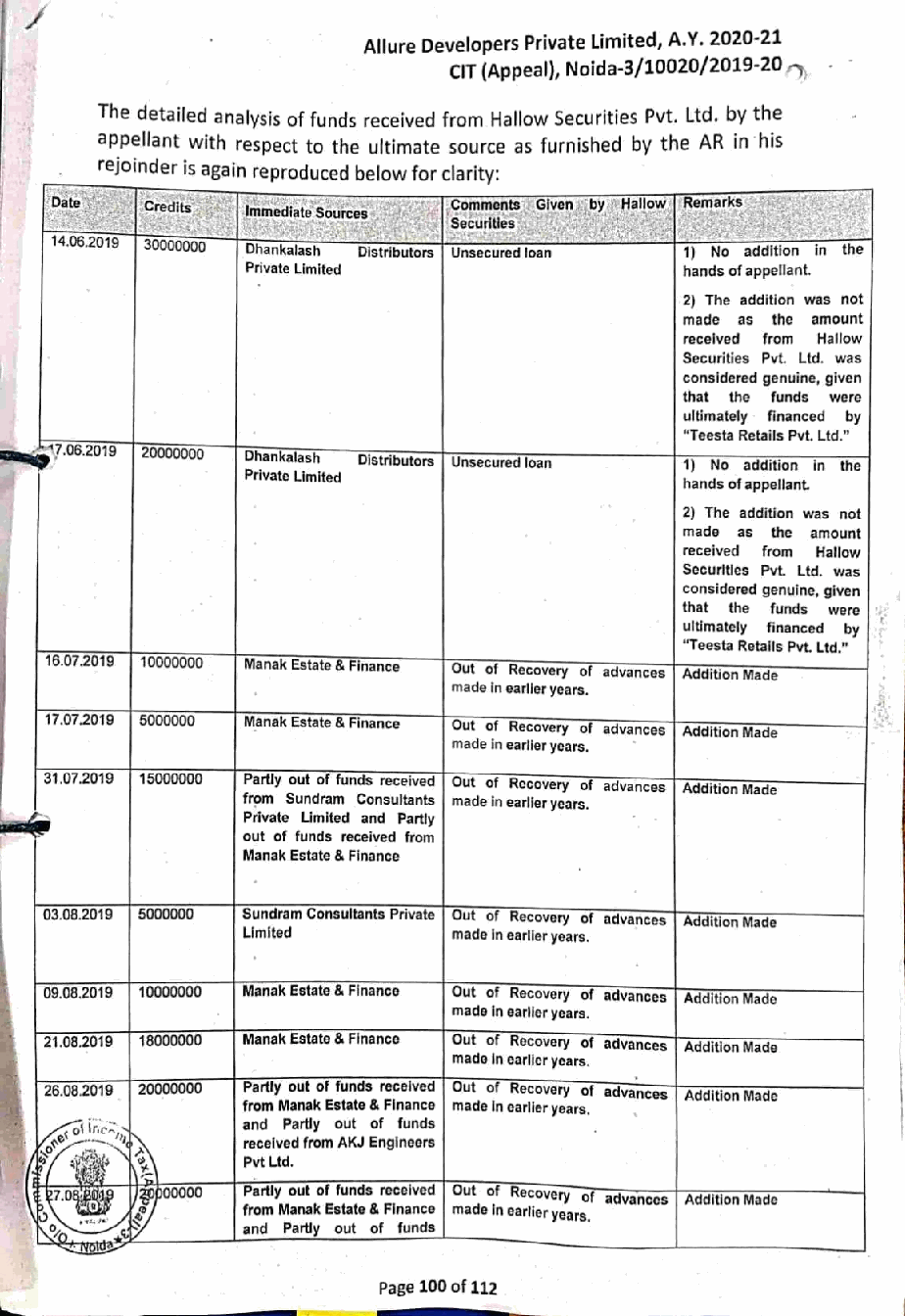

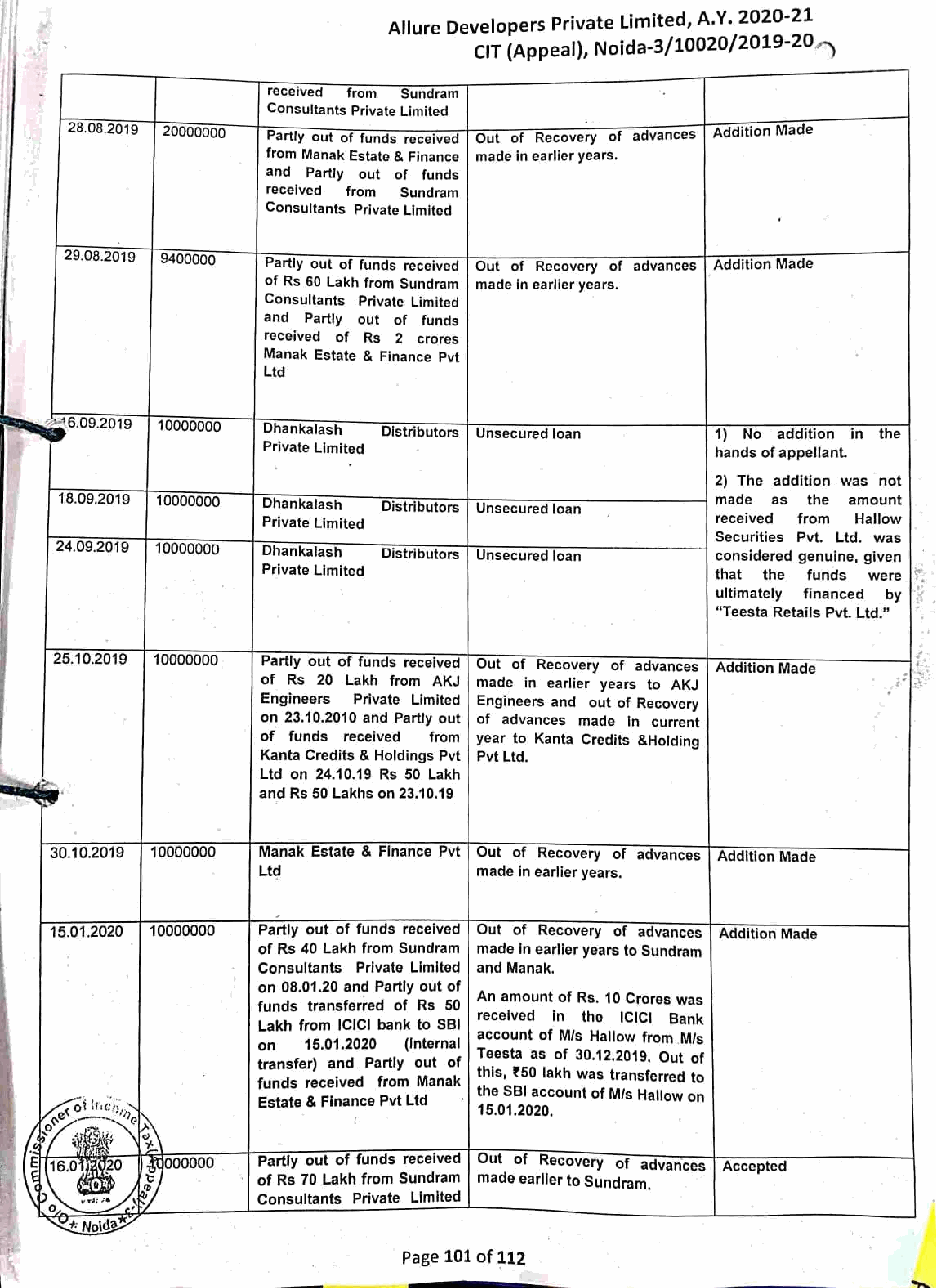

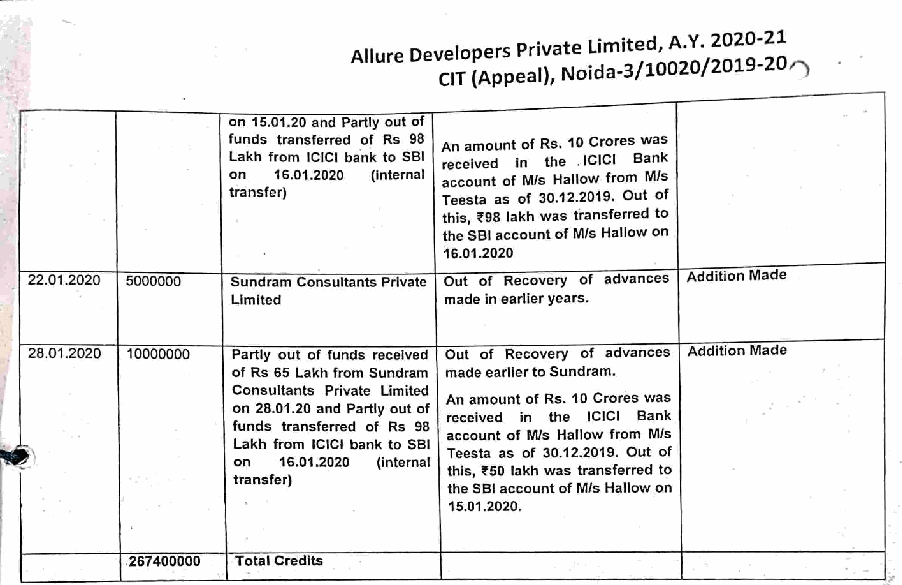

5. We have heard the rival contentions and perused the material available on record. From the perusal of the assessment and appellate order, it is seen that on the issue of receipts from M/s Hallow Securities Pvt. Ltd., all the observations and allegations made by AO are same as were made in the case of M/s Allure Developers Pvt. Ltd. for Assessment Year 2020-21 & Others in ITA No. 3559/Del/2025 & Others vide order dated 26.11.2025. The relevant observations by the Tribunal in deciding the appeal in No.3559/Del/2025 are as under:-

19. “Heard the parties and perused the material available on records. In the present case the sole issue before us is the addition made of Rs. 17,74,00,000/- made by AO by holding the loans taken from M/s Hallow Securities Pvt. Ltd as unexplained u/s 68 of the Act which stood deleted by ld. CIT(A). Before going further, the facts leading to the issue are summarized as under:

“A search action us/ 132 was carried out on ACE group of cases on 28.07.2021 and further on 04.01.2022. During the year assessee received loan of Rs. 26,74,00,000/- from a company M/s Hallow Securities Pvt. Ltd. which is a NBFC. The AO examined the genuineness of loan and after considering the financials of the lender company M/s Hallow Securities Pvt. Ltd., observed its financial position is not satisfactory to grant such a huge loan to the assessee.”

20. The AO has referred the statements of Sh. Nishant Chajjar, Director assessee company who was also the director of lender company M/s Hallow Securities Pvt. Ltd. who in reply to Q. NO. 14 stated that the cash/Hawala Transaction were handled by the other director of assessee company Sh. Prakash Kumar Jha. AO further observed that Shri Nishant is also directors of many companies managed and controlled by one Shri Ashish Begwani who alleged the key person and engaged in providing accommodation loans to assessee. The also referred the statements of Shri Ashish Begwani, recorded in the year 2017 wherein he explained the modus opernadi for providing accommodation entries to various beneficiaries.

21. During the course of assessment proceedings, assessee had submitted copy of ITR, bank statement, Audited Balance Sheet of M/s H

An indispensable Tool for Legal Professionals, Endorsed by Various High Court and Judicial Officers

Please visit our Training & Support

Center or Contact Us for assistance

Scan Me!

India’s Legal research and Law Firm App, Download now!

For Daily Legal Updates, Join us on :