INCOME TAX APPELLATE TRIBUNAL (MUMBAI BENCH)

Shri Amit Shukla, J, Shri Girish Agrawal, ACJ

Lloyds Metals And Energy Limited – Appellant

Versus

Dy. Commissioner of Income Tax, Central Circle 7(1), Mumbai – Respondent

| Table of Content |

|---|

| 1. identification of identical issues from related cases (Para 1 , 2) |

| 2. revenue's contentions against cit(a)'s relief (Para 3 , 4) |

| 3. factual background from the search actions (Para 5 , 6 , 8) |

| 4. estimation methodology for additional income (Para 11 , 12 , 14 , 24) |

| 5. substantiation of claims regarding alleged bogus transactions (Para 15 , 18 , 20 , 22) |

| 6. final decision on appeal outcomes (Para 27 , 30) |

ORDER

PER BENCH:

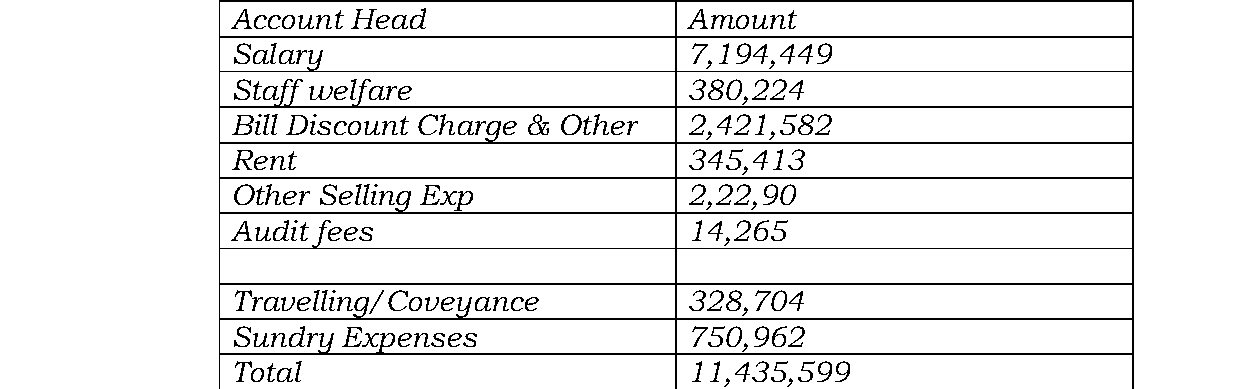

These cross appeals by the assessees as well as by the Revenue arise from separate but materially similar orders passed by the learned Commissioner of Income Tax (Appeals)– 49, Mumbai, in the cases of Lloyds Metals and Energy Limited and Lloyds Enterprises Limited, for Assessment Years 2013– 14 to 2019–20. The assessments in all these years have been framed under section 143(3) read with section 153C of the Income Tax Act, 1961 , pursuant to search and seizure action in a connected group case, and the impugned orders deal with common issues concerning the nature of alleged bogus purchases and sales, rejection of books, estimation of additional income, and disallowance of indirect expenditure.

2. At the very threshold, it was fairly admitted by both sides

An indispensable Tool for Legal Professionals, Endorsed by Various High Court and Judicial Officers

Please visit our Training & Support

Center or Contact Us for assistance

Scan Me!

India’s Legal research and Law Firm App, Download now!

For Daily Legal Updates, Join us on :