INCOME TAX APPELLATE TRIBUNAL (DELHI BENCH)

Yogesh Kumar U.S., J, Shri Manish Agarwal, ACJ

Tayal Sons Private – Appellant

Versus

DCIT – Respondent

ORDER

PER YOGESH KUMAR, U.S. JM:

The captioned two appeals are filed by the Assessee and two Appeals are filed by the Revenue aggrieved by the orders dated 29/03/2025 for Assessment Year 2018-19 and dated 30/03/2025 for Assessment Year 2019-20challenging the orders of National Faceless Appeal Centre (‘NFAC/Ld. CIT(A)’ for short).

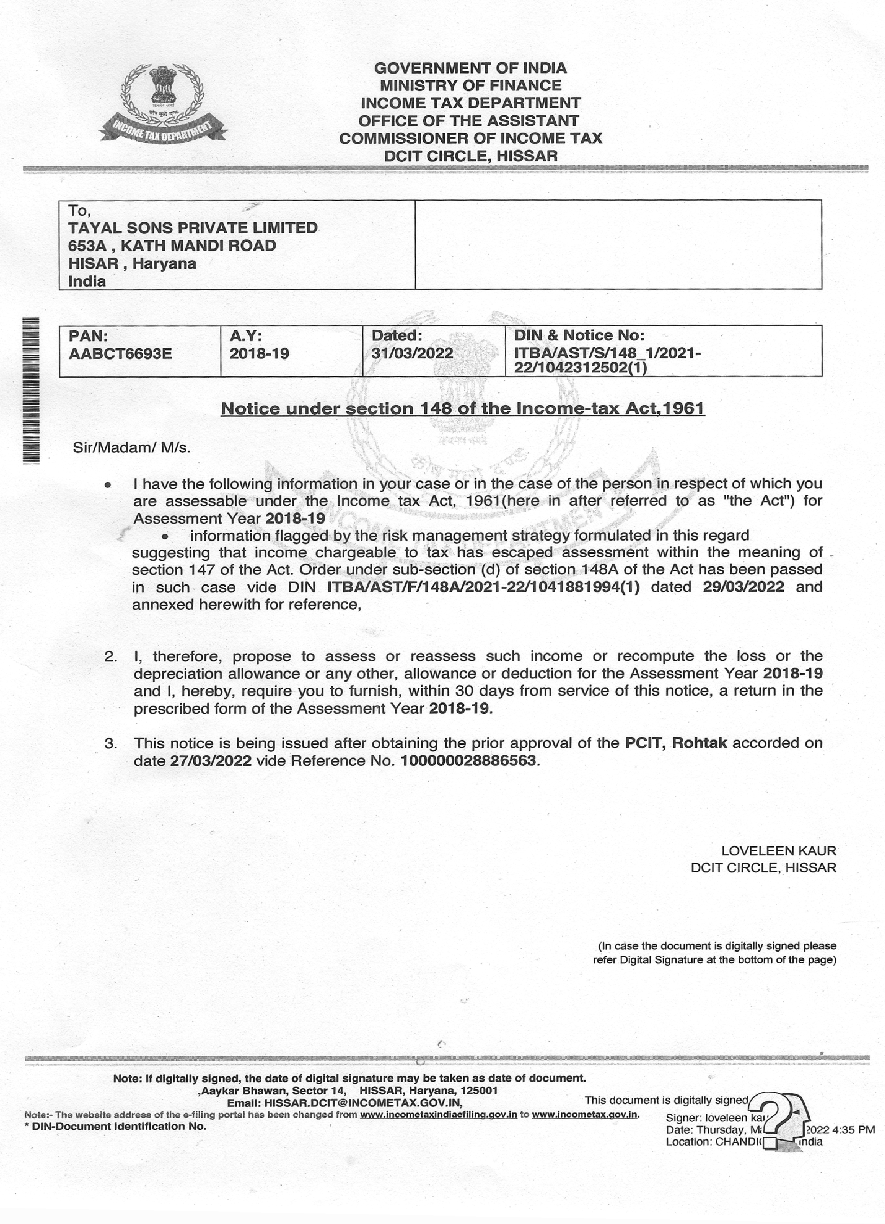

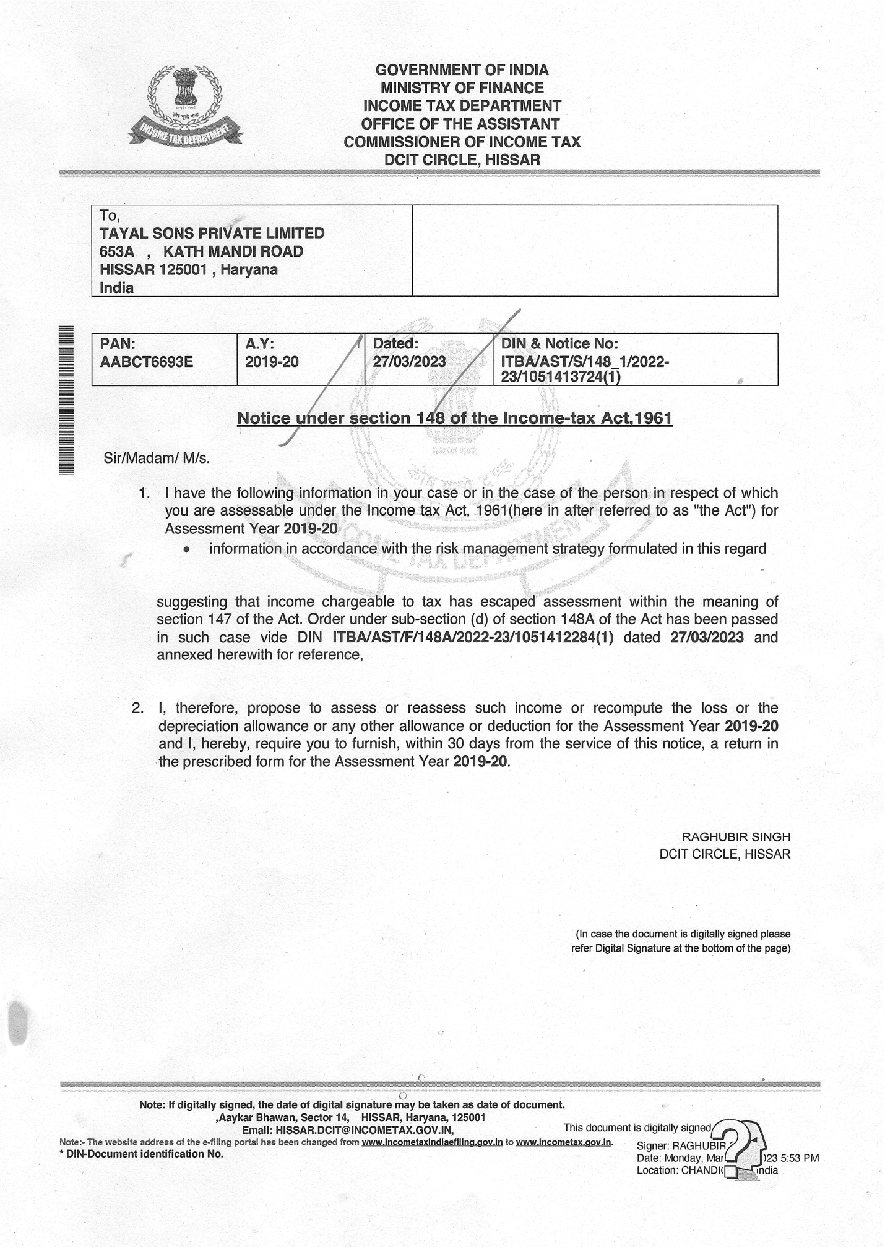

2. The Ld. Assessee's Representative at the outset submitted that notices dated 11/03/2022 for Assessment Year 2018-19 and notice dated 08/03/2023 issued u/s 148A(b) of the Income Tax Act, 1961 ('Act' for short) by the Jurisdictional A.O. and the order dated 29/03/2022 and 27/03/2023 u/s 148A(b) of the Act are bad in law. Therefore submitted that the consequential assessment orders deserves to be set aside. The Ld. Counsel has also relied on the order of the Co-ordinate Bench of the Tribunal in the case of Chirag Kirpal Vs. ACIT in ITA No. 656/Del/2025 dated 30/09/2025 and also the Judgment of Jurisdictional High Court i.e. High Court of Punjab and Haryana in CWP-15745-2-24 in the case of Jatinder Singh Bhangu Vs. Union of India vide Judgment dated 19/07/2024.

3. Per contra Ld. DR submitted that as against the Order of the Tribunal and the Judgment of the Ju

An indispensable Tool for Legal Professionals, Endorsed by Various High Court and Judicial Officers

Please visit our Training & Support

Center or Contact Us for assistance

Scan Me!

India’s Legal research and Law Firm App, Download now!

For Daily Legal Updates, Join us on :