INCOME TAX APPELLATE TRIBUNAL (DELHI BENCH)

Yogesh Kumar, Judicial Member, Krinwant Sahay, Accountant Member

DENSO INDIA PRIVATE LIMITED DELHI – Appellant

Versus

ACIT CIRCLE-7(1) DELHI – Respondent

ITA Nos.1484 to 1485/Del/2022 | ITA No.1486/Del/2022

| Table of Content |

|---|

| 1. appeals challenge time-barred assessment orders. (Para 1 , 2) |

| 2. additional limitation ground admitted as legal issue. (Para 3 , 4) |

| 3. reject deferral; follow coordinate bench precedent. (Para 5 , 6) |

| 4. orders beyond s.153 limit; s.144c inclusive. (Para 7 , 8 , 9) |

| 5. quash orders following binding precedents. (Para 10 , 11 , 12) |

| 6. liberty to revive post-supreme court decision. (Para 13 , 14) |

ORDER

PER KRINWANT SAHAY, AM,

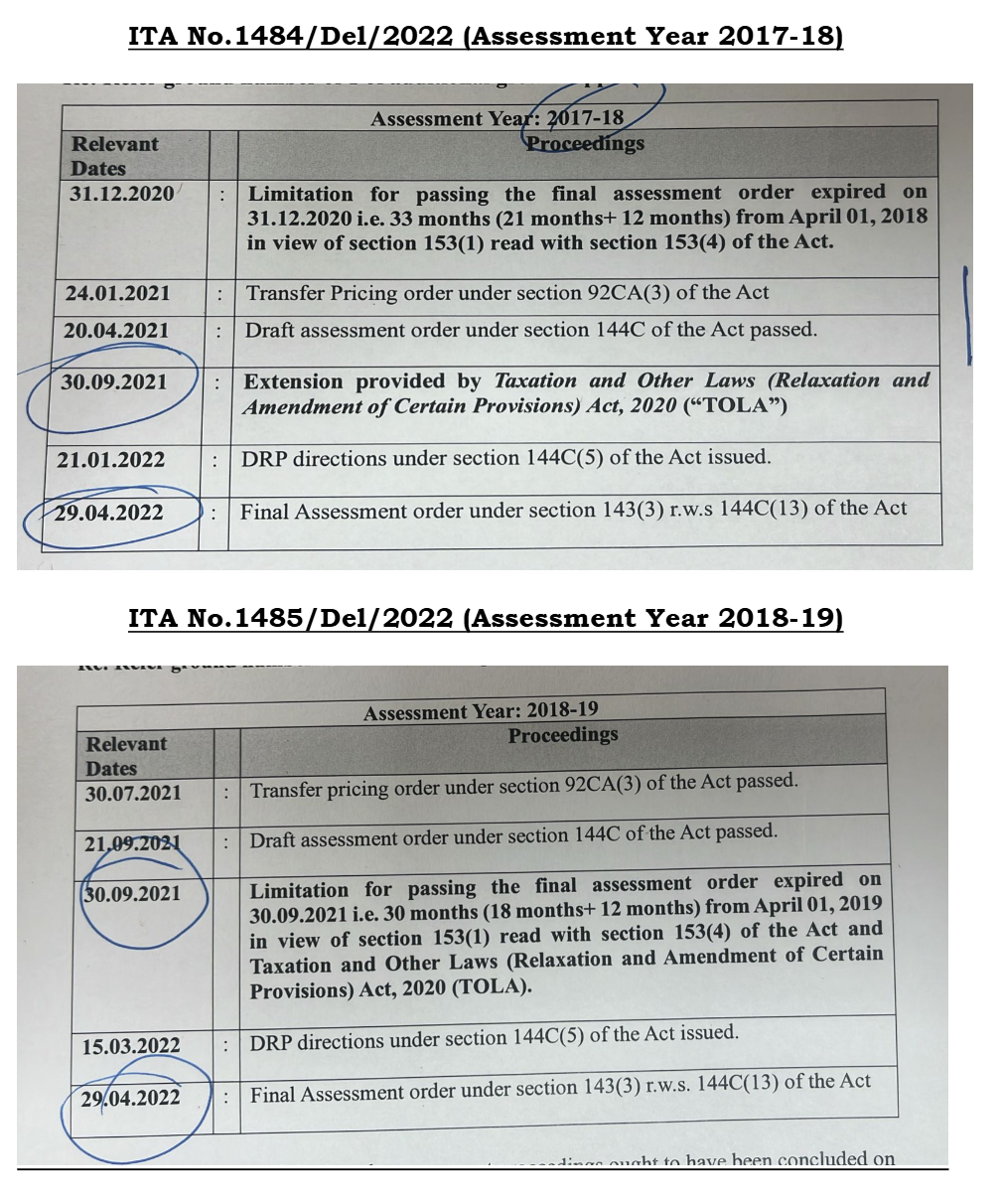

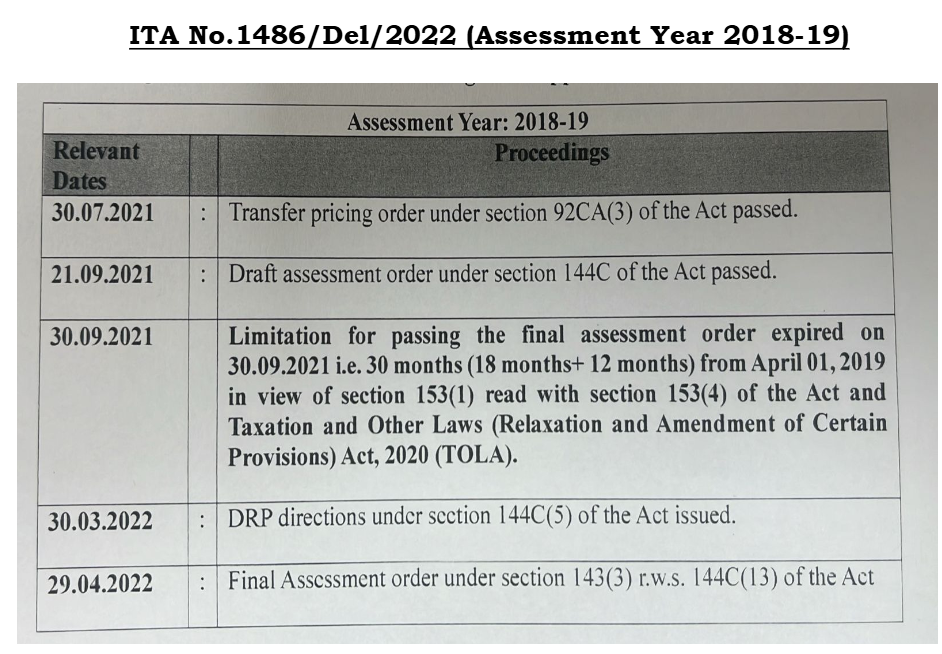

These three appeals are filed by the Assessee challenging the Final Assessment Orders passed u/s 143(3) r.w.s. 144C(13) r.w. Section 144B of the Income Tax Act, 1961 (the Act in short) all dated 29.04.2022 pertaining to the Assessment Years 2017-18 and 2018-19 respectively.

2. The Assessee raised additional ground No.1 in all the appeals contending that the Final Assessment order all dated 30.04.2022 passed by the A.O. is time barred by limitation and is bad in law, as it has been passed beyond the time frame prescribed under section 153(1) read with section 153(4) of the Income Tax Act, 1961 ('Act' for short).

3. We have heard both parties and have perused material available on the record. A perusal of substantive ground of appeal and the application for admission of additional ground clearly indicate that this is legal ground assailing the validity of the assessment order and the order of the Ld. TPO. The Hon'ble Supreme Court of India in the case of National Thermal Power Company, 229 ITR 383 has held that the Tribunal has jurisdiction to examine a question of law which arises from the facts on record and have a bearing on the tax liability of the assessee. In all the appeals, the additional grounds of appeal raised by the assessee challenges the validity of assessment order and the order of the Ld. TPO on the ground of limitation. No further documentary evidence is required to be adduced for adjudicating these grounds. We; therefore, admit the said additional grounds of all the appeal for adjudication.

4. The Assessee raised additional ground No.1 in all the appeals contending that the Final Assessment order all dated 30.04.2022 pertaining to Assessment Years 2017-18 and 2018-19 passed by the A.O. is time barred by limitation and is bad in law, as it has been passed beyond the time frame prescribed under section 153(1) read with section 153(4) of the Income Tax Act, 1961 ('Act' for short). The Ld. Assessee's Representative relying on the ratio laid down by the Hon'ble High Court of Madras in the case of Commissioner of Income- tax Vs. Roca Bathroom Products (P.) Ltd. [2022] 445 537 (Madras) and also plethora of orders passed by the Co-ordinate Bench of the Tribunal, Hyderabad Bench sought for allowing the Additional ground- 1 of the Assessee.

5. Per contra, the Ld. Department's Representative submitted that the issue of limitation arising from the interplay between Section 144C and Section 153 of the Act is presently unsettled and pending adjudication before the Hon'ble Supreme Court in the case of ACIT Vs. Shelf Drilling Ron Tappmeyer Ltd. in Special Leave to Appeal (C) Nos. 20569-20572/2023 therefore, deciding the very same issue by this Tribunal at this stage would be premature, thus submitted that the Tribunal cannot decide the issue of limitation in terms of the ratio laid down by the Hon'ble High Court of Madras in the case of Roca Bathroom Products (P) Ltd. (supra). Accordingly, the Ld. Department's Representative sought for deferral of adjudication of the present Appeal and also the issue of limitation. The Ld. Department's Representative has also filed detail written submission.

6. The identical submissions of the parties have been considered by us in the case of Teva Pharmaceutical & chemical Industries India Private Limited Vs. Assessment Unit, Income Tax Department/DCIT in ITA No. 4197/Del/2024 vide order dated 19/01/2026. The Co- ordinate Bench of the Tribunal while and rejected the preliminary objection raised by the Revenue and also the request of the Department for deferring the hear

An indispensable Tool for Legal Professionals, Endorsed by Various High Court and Judicial Officers

Please visit our Training & Support

Center or Contact Us for assistance

Scan Me!

India’s Legal research and Law Firm App, Download now!

For Daily Legal Updates, Join us on :