INCOME TAX APPELLATE TRIBUNAL (DELHI BENCH)

Vikas Awasthy, Judicial Member, Sanjay Awasthi, Accountant Member

The Bank of Tokyo-Mistubishi UFJ Ltd. – Appellant

Versus

Deputy Commissioner of Income-Tax – Respondent

ITA No. 1014/Del/2018(A.Y 2012-13)|ITA No. 4894/Del/2018(A.Y 2012-13)|CO No. 224/Del/2018

| Table of Content |

|---|

| 1. cross appeals against assessment order under section 144c. (Para 1) |

| 2. assessee argues assessment barred by limitation per 144c r.w.s 153. (Para 2) |

| 3. revenue objects to hearing due to pending supreme court reference. (Para 3) |

| 4. tribunal rejects revenue's objection to proceed with hearing. (Para 4) |

| 5. revenue argues 144c independent timelines exclude section 153. (Para 5) |

| 6. sections 144c and 153 mutually inclusive for limitation. (Para 6 , 7) |

| 7. timeline shows assessment order beyond limitation period. (Para 8) |

| 8. assessment quashed; appeals disposed on jurisdictional ground. (Para 9 , 10 , 11 , 12 , 13) |

आदेश/ORDER

PER VIKAS AWASTHY, JM:

These cross appeals by the assessee and the Revenue for AY 2012-13 are directed against the Assessment Order dated 10.05.2016 passed u/s.143(3) r.w.s. 144C(13) of the Income Tax Act,1961(hereinafter referred to as ‘the Act’). The assessee in appeal has challenged validity of the final assessment order on the ground of limitation under section 144C(13) r.w.s. 153 of the Act. The assessee has raised this legal ground by way of additional ground of appeal vide application dated 26.05.2023.

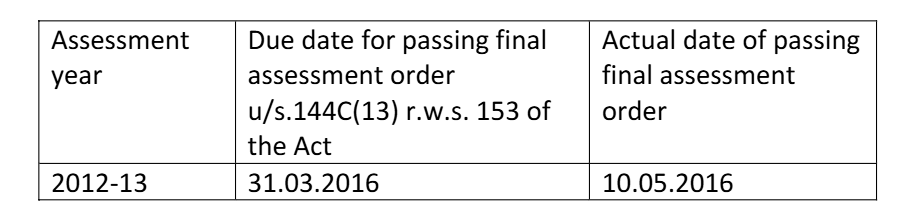

2. The ld. Counsel for the assessee placing reliance on the decision rendered in the case of CIT vs. Roca Bathroom Products P Ltd. reported as 140 taxmann.com 304 (Mad.), submits that the assessment order in the impugned assessment year is barred by limitation. He submitted that for determining the period of limitation for passing final assessment order the provisions of section 144C of the Act, are to be read with section 153 of the Act. He furnished the date chart tabulating the relevant dates for ascertaining the period of limitation within which the final assessment order was required to be passed and also the dates on which the final assessment orders for respective assessment years were actually passed by the Assessing Officer (AO). The ld. Counsel submits that various Benches of the Tribunal have taken a consistent view and have quashed final assessment order passed beyond the period of limitation as per section 144C(13) r.w.s. 153 of the Act. To further buttress his submissions, he placed reliance on the Tribunal orders in the case of Aveva Solutions India LLP v ITO [2025], 180 taxmann.com 731 (Hyd-Trib.) & Superbrands Ltd. (UK) vs DCIT (ITA No.332/Del/2021) decided on 29.09.2022.

3. Shri Dharam Veer Singh representing the department at the outset raised objection for taking up these appeals for adjudication. He submitted that the issue is now sub judice before the Hon’ble Apex Court. The Division Bench of Hon’ble Supreme Court of India in the case of Shelf Drilling Ron Tappmeyer Ltd. has examined the issue but due to divergent opinions expressed by the Hon’ble Judges, the issue is now referred to the Hon’ble Chief Justice of India for constituting a Larger Bench. Even otherwise the Hon’ble Apex Court in the case of Shelf Drilling Ron Tappmeyer Ltd. (supra), vide interim order dated 22.09.2023 has held that the operative part of the impugned judgment shall not be cited as a precedent in other subsequent matters. Thus, in light of the said order passed by the Hon’ble Apex Court it would not be in judicial propriety to proceed with the identical matter. He further referred to the judgement of Hon’ble Bombay High Court in the case of PayPal Payments P. Ltd. vs ACIT in Writ Petition (L) No. 30944 of 2023 decided on 13.08.2024, to contend that even the Hon’ble Bombay High Court, after taking note of the fact that the Hon’ble Supreme Court has stayed the operative part of the judgment in the case of Shelf Drilling Ron Tappmeyer Ltd. (supra), has refused to entertain the Writ Petition involving identical issue. The ld. DR further referred to the decision of Hon’ble Supreme Court of India in the case of UP Rashtriya Chini Mill Adhikari Parishad, Lucknow Vs. State of U.P. and Others reported as (1995) AIR SC 2148, to contend that when the issue is referred to a Larger Bench, during the pendency of such

An indispensable Tool for Legal Professionals, Endorsed by Various High Court and Judicial Officers

Please visit our Training & Support

Center or Contact Us for assistance

Scan Me!

India’s Legal research and Law Firm App, Download now!

For Daily Legal Updates, Join us on :