INCOME TAX APPELLATE TRIBUNAL (MUMBAI BENCH)

Pawan Singh, Judicial Member, Girish Agrawal, Accountant Member

DEVANAND AMARNATH PARKAR JOGESHWARI EAST MUMBAI – Appellant

Versus

INCOME TAX OFFICER 41(4)(1) KAUTILYA BHAWAN BKC BANDRA EAST – Respondent

ITA No. 6462/MUM/2025

| Table of Content |

|---|

| 1. assessee challenges reassessment notice validity. (Para 1 , 2 , 3) |

| 2. notice u/s 148 beyond 3-year limitation. (Para 4) |

| 3. notice quashed as time-barred under new regime. (Para 5) |

| 4. appeal allowed; reassessment proceedings quashed. (Para 6) |

ORDER

PER GIRISH AGRAWAL, ACCOUNTANT MEMBER:

This appeal filed by the assessee is against the order of ld. CIT(A), National Faceless Appeal Centre (NFAC), Delhi, vide order no. ITBA/NFAC/S/250/2025-26/1080924932(1), dated 19.09.2025, passed against the assessment order by National Faceless Assessment Center, New Delhi, u/s. 147 r.w.s 144B of the Income-tax Act (hereinafter referred to as the “Act”), dated 22.05.2023 for Assessment Year 2017-18.

2. Grounds taken by the assessee are reproduced as under:

1. On the facts and circumstances of the case and law, the Ld CIT(A) grossly erred & failed to appreciate that the reopening of assessment vide notice u/s 148 of the Act dated 30/07/2022 i.e After expiry of three years from the end of the assessment year 2017-18 without appreciating that notice under section 148 can be issued beyond 3 years only if income escapement is above 50 lacs, in fact of present case the impugned notice issued for AY 2017-18 is for income escaped below 50 lacs i.e Rs.5,72,886/-, therefore reopening is bad in law.

2. On the facts and circumstances of the case and law, the Ld CIT(A) grossly erred in not appreciating the fact that Ld. JAO issued reopening notice beyond period of three years, approval was required to be taken as per provisions of amended section 151 of the Act from Principal Chief Commissioner or Principal Director General or Chief Commissioner or Director General however approval was taken from PCIT-2.

3. On the facts and circumstances of the case and law, the Ld CIT(A) grossly erred in not appreciating the fact that Ld JAO have no jurisdiction to issue Notice u/s 148 as same had to be done in faceless manner.

4. On the facts and circumstances of the case and law, the Ld CIT(A) grossly erred in not considering the fact that the assumption of Ld. AO in issuing notice under section 148 of Income Tax Act, 1961 without mentioning the DIN Number on notice itself which is violation of CBDT Circular No. 19 of 2019 dated 14.08.2019.

5. On the facts and in the circumstances of the case and in law, the learned Commissioner of Income Tax (Appeals) erred in not appreciating that the show cause notice issued under section 148A(b), the order passed under section 148A(d), and the consequential notice issued under section 148 were all issued by an officer who did not have jurisdiction over the assessee. Hence, the entire proceedings initiated and the reassessment made pursuant thereto are void ab initio and liable to be quashed for want of jurisdiction.

6. On the facts and in the circumstances of the case and in law, the learned Assessing Officer erred in making an addition of Rs.5,72,886/- on account of the difference between the stamp duty valuation and the actual purchase consideration under section 56(2)(viib) of the Income-tax Act, without properly appreciating and considering the independent valuation report submitted by the appellant. The addition so made is unjustified, excessive, and liable to be deleted.

2.1. In this appeal by the assessee, vide ground nos.1 essentially the issue to be decided is on legal ground, challenging the validity of notice issued u/s.148 on account of being barred by limitation and therefore, consequent reassessment order passed u/s. 147 r.w.s. 144C(3) being bad in law.

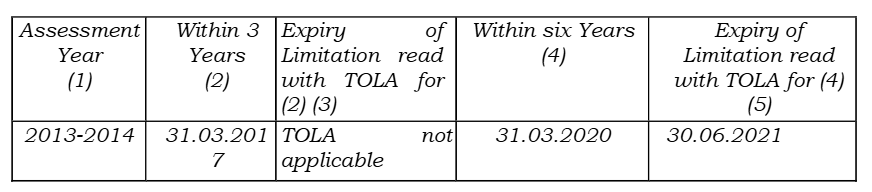

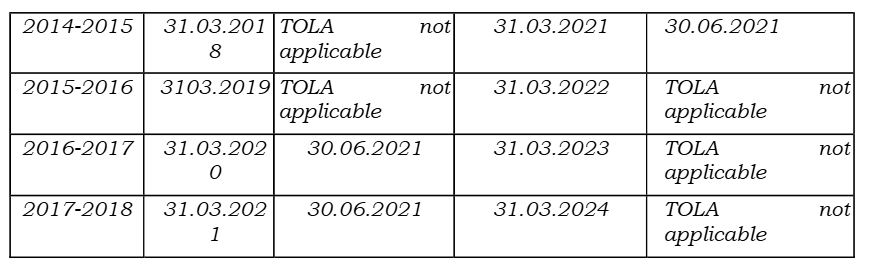

3. Since the impugned notice u/s. 148 was issued under the erstwhile regime of re-assessment as provided u/s.148 r.w.s. 147 which has undergone total revamp by the Finance Act, 2021, the amendments brought in by the Finance Act 2021 led to several jurisdictional issues in respect of reassessment proceeding for which the matter travelled up to the Hon'ble Supreme Court with the lead case of Union of India vs. Ashish Agarwal [2022] 130 taxmann.com 64 (SC) followed by t

An indispensable Tool for Legal Professionals, Endorsed by Various High Court and Judicial Officers

Please visit our Training & Support

Center or Contact Us for assistance

Scan Me!

India’s Legal research and Law Firm App, Download now!

For Daily Legal Updates, Join us on :