INCOME TAX APPELLATE TRIBUNAL (BANGALORE BENCH)

Prashant Maharishi, Vice President, Soundararajan K., Judicial Member

Primary Agricultural Credit Co-operative Society – Appellant

Versus

Principal Commissioner of Income Tax – Respondent

| Table of Content |

|---|

| 1. assessee's s.80p deduction on interest income allowed by ao post scrutiny. (Para 1 , 2 , 3 , 4 , 5) |

| 2. pcit invokes s.263 deeming ao order erroneous on interest classification. (Para 6 , 7 , 8 , 9 , 10) |

| 3. parties argue conflicting high court views on deductibility. (Para 11 , 12) |

| 4. 'attributable to' includes bank interest from credit business funds. (Para 13 , 14 , 15 , 16) |

| 5. s.263 quashed; two views possible, ao view sustainable. (Para 17 , 18 , 19) |

ORDER

Per Prashant Maharishi, Vice President

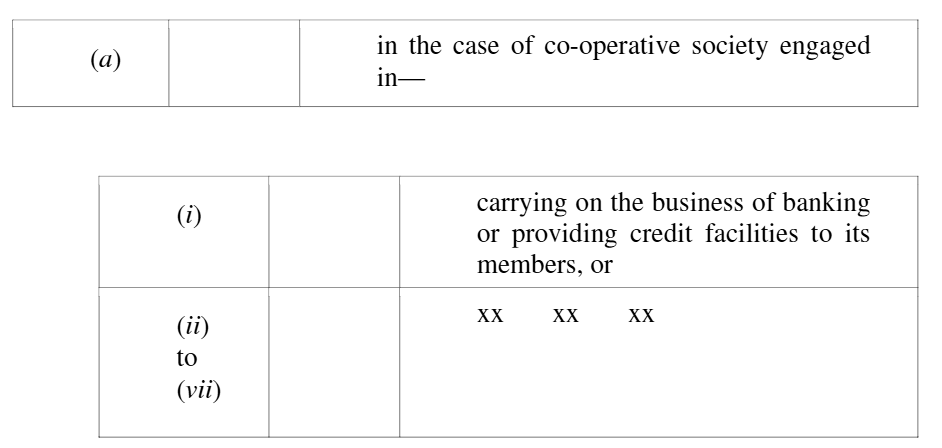

1. This appeal is filed by Primary Agricultural Credit Co-operative Society, Balele Village, Balele Post, (the assessee/appellant) for the assessment year 2020-21 against the revisionary order passed u/s. 263 of the Income Tax Act, 1961 [the Act] by the ld. Principal Commissioner of Income Tax, Bengaluru-3, Bangalore [PCIT] dated 27.03.2025 holding that the assessment order passed u/s. 143 (3) r.w.s. 144B the [the Act] on 5.9.2022 by the Assessment Unit, Income Tax Department (the ld. AO) is erroneous and prejudicial to the interests of the Revenue to the extent that interest income of ₹ 2,580,032/– on fund deposits made in various banks are allowed as deduction u/s. 80P(2)(a

An indispensable Tool for Legal Professionals, Endorsed by Various High Court and Judicial Officers

Please visit our Training & Support

Center or Contact Us for assistance

Scan Me!

India’s Legal research and Law Firm App, Download now!

For Daily Legal Updates, Join us on :