INCOME TAX APPELLATE TRIBUNAL (CHENNAI BENCH)

ABY T. VARKEY, Judicial Member, PADMAVATHY. S, Accountant Member

Southern Enterprises – Appellant

Versus

ACIT – Respondent

ITA No.2941/Chny/2017

| Table of Content |

|---|

| 1. challenge to reopening beyond 4 years without non-disclosure finding. (Para 2 , 3) |

| 2. ao's reasons on improper closing stock allocation examined. (Para 4 , 5) |

| 3. original scrutiny covered all material facts supplied. (Para 6) |

| 4. reopening quashed for lacking jurisdictional fact. (Para 7) |

| 5. assessee's appeal allowed. (Para 8) |

आदशे/ORDER

PER ABY T. VARKEY, JM:

This is an appeal preferred by the assessee against the order of the Learned Commissioner of Income Tax (Appeals)-10, (hereinafter referred to as ‘Ld.CIT(A)‘), Chennai, dated 15.09.2017 for the Assessment Year (hereinafter referred to as ‘AY‘) 2009-10.

2. At the outset, the Ld.AR of the assessee has assailed the action of the AO reopening of assessment after expiry of four (4) years from the end of the relevant assessment year without satisfying the condition precedent specified in the first proviso to Section 147 of the Income Tax Act, 1961 (hereinafter referred to as ‘the Act‘) i.e. there was a failure on the part of the assessee to disclose fully and truly all material facts necessary for his assessment for that assessment year.

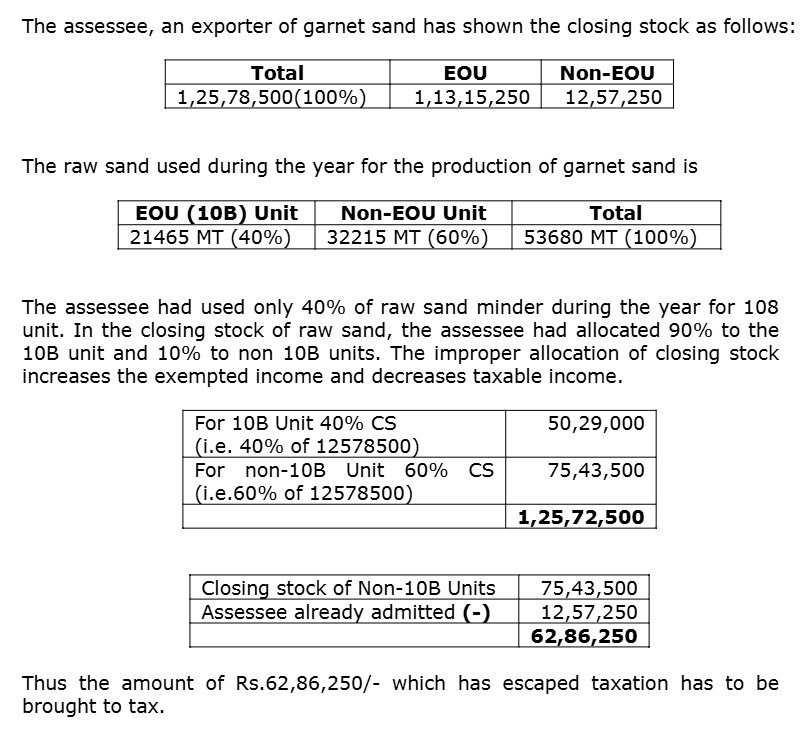

3. The brief facts relevant for adjudication of the aforesaid legal issue are that the assessee is a Garnet Sand Exporter and during the year filed its return of income (RoI/ITR) on 25.09.2009 declaring total income at ₹44,24,420/-. The RoI was selected for scrutiny under CASS and the AO issued notices u/s.143(2) of the Act dated 19.08.2010, and notice u/s.142(1) of the Act dated 29.09.2011 and the assessee had participated in the original assessment proceedings, wherein, the AO asked the assessee inter-alia to give details of the deduction claimed by the assessee u/s.10B of the Act to the extent of ₹2,71,88,706/- of its Export Oriented Unit (EOU). And the assessee is noted to have furnished the details sought by the AO in respect of its EOU Unit as well as that of the other non-EOU Unit. The AO is noted to have verified the exemption claimed u/s.10B of the Act on the profits accrued from the EOU Unit and noted to have called for the financials of both the Units (EOU Unit & non- EOU Unit) and after examining the expenditure claimed by the assessee in respect of ‘mining lease expenses’ & bank charges, the AO is noted to have allowed only deduction u/s.10B of the Act at ₹2,58,09,970/- in respect of the assessee claim of ₹2,71,88,706/- and in that process, allocated expenditure of ₹13,78,736/- from non-EOU Unit to EOU Unit. Thus, he reduced the profit of the EOU Unit by the said sum of ₹13,78,736/- and allowed the deduction at ₹2,58,09,970/- by framing the original assessment order u/s.143(3) of the Act on 23.12.2011.

4. Thereafter, the AO is noted to have issued notice u/s.148 of the Act on 05.12.2014 conveying his desire to reopen the assessment dated 23.12.2011 for AY 2009-10, which we note was an event after expiry of four (4) years from the end of the relevant assessment year and therefore, as rightly asserted by the Ld.AR, the proviso to Section 147 of the Act would come into play and hence, before the AO assumes the reopening jurisdiction, he (AO) has to satisfy the additional condition- precedent i.e. ‘the assessee failed to disclose fully and truly all material facts necessary for his assessment for that assessment year’ which is a jurisdictional fact essential for usurping the reopening jurisdiction for the relevant AY 2009-10. Here in this case, as noted supra the ITR of the assessee was earlier selected for scrutiny mainly for examining the claim of deduction u/s.10B of the Act for its EOU Unit of ₹2,71,88,706/- and expenditure incurred by the EOU Unit & non-EOU Unit. The AO is noted to have reduced the claim of the assessee u/s.10B of the Act at ₹2,58,09,970/- by passing the assessment order on 23.12.2011 u/s.143(3) of the Act; and after expiry of four (4) years from the end of the relevant assessment year, he (AO) has issued the notice u/s.148 of the Act on 05.12.2014 on the strength of the reasons recorded by him as given b

An indispensable Tool for Legal Professionals, Endorsed by Various High Court and Judicial Officers

Please visit our Training & Support

Center or Contact Us for assistance

Scan Me!

India’s Legal research and Law Firm App, Download now!

For Daily Legal Updates, Join us on :