INCOME TAX APPELLATE TRIBUNAL (MUMBAI BENCH)

KISHORE ANAND SHETTY MUMBAI – Appellant

Versus

CIRCLE-32(2) MUMBAI – Respondent

आदेश/ORDER

PER AMIT SHUKLA (J.M):

These two appeals have been preferred by the assessee against separate orders dated 24.07.2025 passed by the National Faceless Appeal Centre, Delhi, one arising out of the quantum assessment framed under section 143(3) of the Income-tax Act, 1961 for Assessment Year 2014-15 and the other arising out of the penalty proceedings initiated and levied under section 271(1)(c) of the Act for the same assessment year. Since the penalty proceedings are purely consequential and arise directly out of the additions made in the quantum assessment, both the appeals were heard together and are being disposed of by this consolidated order.

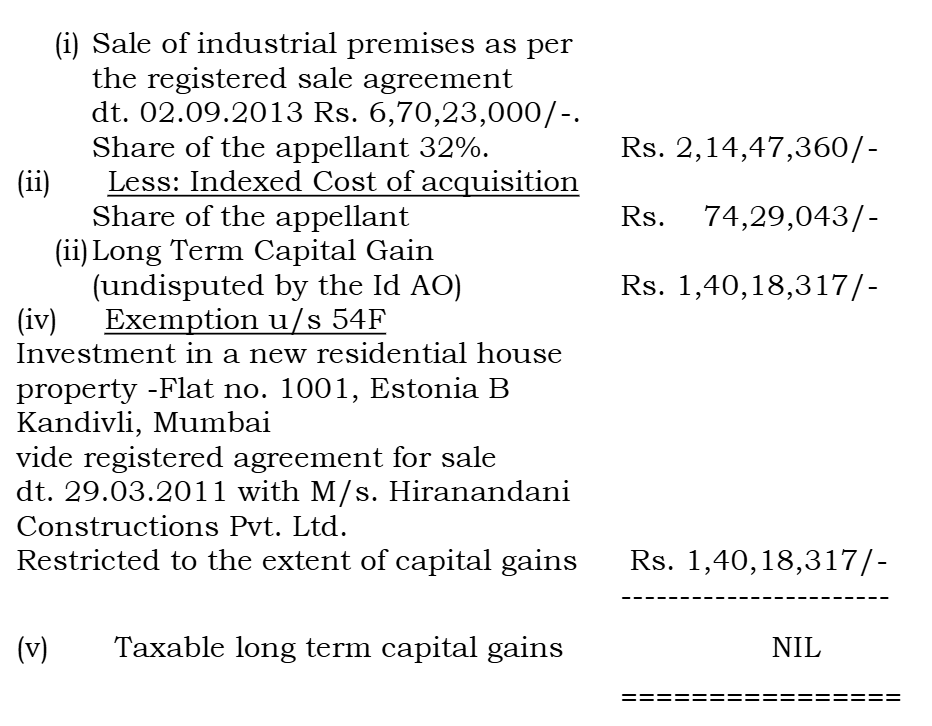

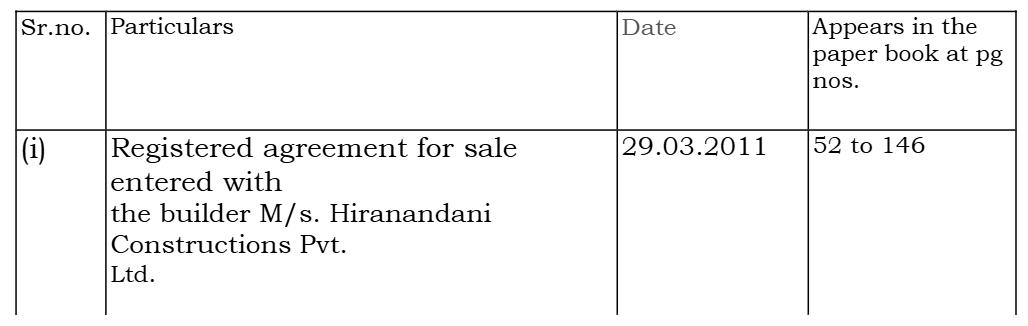

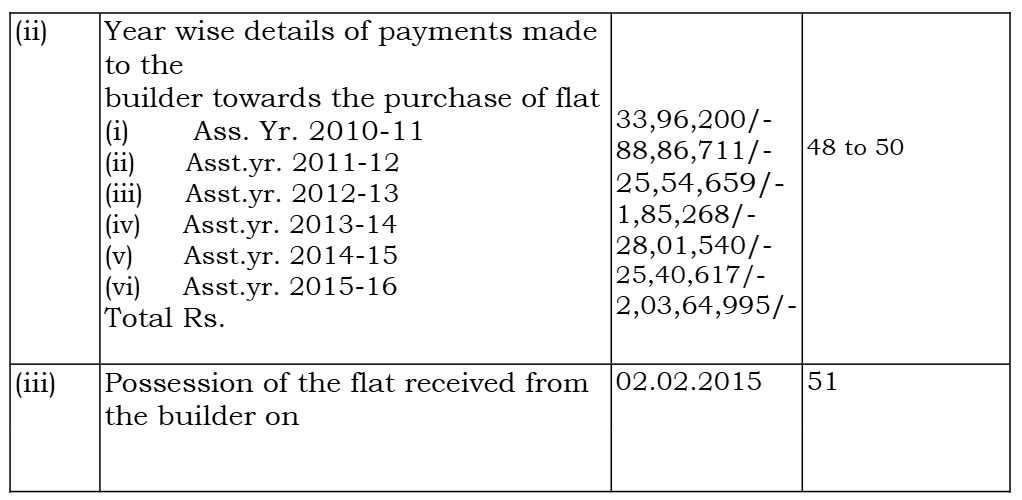

2. We shall first take up the quantum appeal in ITA No. 4975/Mum/2025. In this appeal, the assessee has challenged, firstly, the addition of ₹13,47,925/- made by invoking the provisions of section 50C of the Act and, secondly, the disallowance of exemption claimed under section 54F amounting to ₹1,12,30,723/-.

3. At the outset, it is noted that the ground relating to short-term capital gain of ₹19,06,317/- was expressly not pressed by the learned counsel for the assessee at the time of hearing. The same is accordingly dismissed as n

An indispensable Tool for Legal Professionals, Endorsed by Various High Court and Judicial Officers

Please visit our Training & Support

Center or Contact Us for assistance

Scan Me!

India’s Legal research and Law Firm App, Download now!

For Daily Legal Updates, Join us on :