INCOME TAX APPELLATE TRIBUNAL (AHMEDABAD BENCH)

Sanjay Garg, Judicial Member

Revenue – Appellant

Versus

Unicorn Packaging LLP – Respondent

ITA No.893/Ahd/2025|ITA Nos.894/Ahd/2025|ITA No.896/Ahd/2025|ITA No.895/Ahd/2025|ITA No.897/Ahd/2025|ITA No.898/Ahd/2025

| Table of Content |

|---|

| 1. corporate restructuring via amalgamations and conversion to llp (Para 1 , 3) |

| 2. depreciation allowable on amalgamation goodwill as intangible asset (Para 2 , 4 , 5) |

| 3. revenue appeals dismissed following prior bindings precedents (Para 6 , 7 , 9 , 13 , 20 , 21 , 22) |

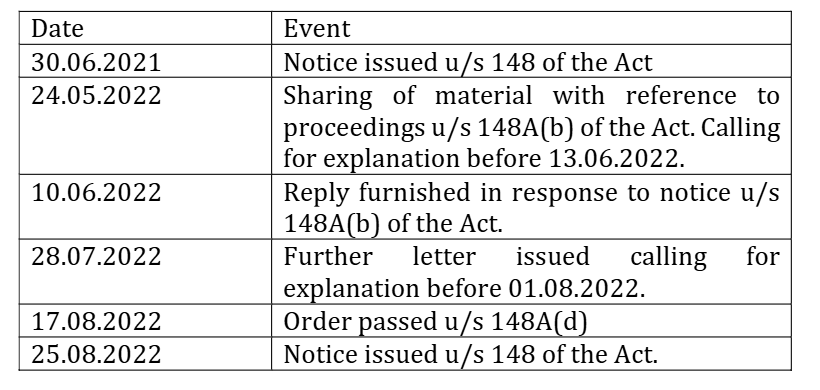

| 4. section 148 notice time-barred under tola and ashish agarwal (Para 8) |

| 5. assessment invalid in name of non-existing converted entity (Para 10 , 11 , 12) |

| 6. no 14a disallowance without recorded dissatisfaction before rule 8d (Para 14 , 15 , 16 , 17 , 18) |

Per Sanjay Garg, Judicial Member:

The captioned appeals have been preferred by the Revenue against the separate orders of the learned Commissioner of Income Tax (Appeals)-11, Ahmedabad [hereinafter referred to as “(CIT(A)”] Since identical facts and issues are involved in these appeals, hence the same were heard together and are being disposed of by this common order. ITA No.893/Ahd/2025 preferred against the order of the CIT(A) dated 24.02.2025 for the assessment year 2016-17 is taken as the lead case for the purpose of narration of facts.

ITA 893/AHD/2025:

2. The Revenue in this appeal has taken the following Grounds of Appeal:

1) "The Ld. CIT(A) has erred in deleting the disallowance of Rs.2,64,14,409/- on account of deprecation on goodwill without appreciating the facts of the case and reasons elaborated by the A.O. in the assessment order."

2) "The Ld. CIT(A) has ignored the intricacies of 6th proviso to section 32(1), section 49(1)(iii)(e), Explanation 7 to section 43(1) and/or Explanation 2(b) to section 43(6)(c) and section 55(2)(a)(ii) which established that Depreciation cannot be claimed on goodwill arising out of amalgamation under the existing provision of the Income-tax Act."

3) "The Revenue craves leave to add/alter/armed and/or substitute any or all of the grounds of appeal."

3. The brief facts of the case, as culled out from the assessment order and the impugned order of the CIT(A), are that the assessee is a limited liability partnership firm which filed its return of income for A.Y. 2016-17 on 16.10.2016 declaring total income of Rs.1,42,588/-. The entity has undergone a series of restructuring events: Unicorn Packers Pvt. Ltd. was amalgamated with Urmin Marketing Pvt. Ltd. with appointed date 01.04.2014 pursuant to a scheme of amalgamation approved by the Hon’ble Gujarat High Court vide order dated 27.07.2015; thereafter Urmin Marketing Pvt. Ltd. was amalgamated with Urmin Flavoroma Pvt. Ltd. with appointed date 01.04.2015 in a scheme approved by the Hon’ble Gujarat High Court vide order dated 05.01.2016; subsequently, with effect from 01.03.2016, the name of Urmin Flavoroma Pvt. Ltd. was changed to Unicorn Packaging Pvt. Ltd.; and finally, with effect from 21.03.2016, Unicorn Packaging Pvt. Ltd. was converted into Unicorn Packaging LLP, the present assessee.

3.1. In the first amalgamation, all the assets and liabilities of Unicorn Packers Pvt. Ltd. became the assets and liabilities of Urmin Marketing Pvt. Ltd., and, as recorded both in the assessment for A.Y. 2015-16 and in the present CIT(A) order, the purchase consideration for Unicorn Packers Pvt. Ltd. was determined on the basis of a valuation report of RBSA Capital Advisors LLP, a Category-I merchant banker registered with SEBI. Under the approved scheme, Urmin Marketing Pvt. Ltd. issued 4,50,00,000 equity shares of Rs.10 each at a premium of Rs.113.50 per share (issue price Rs.123.50 per share) against 90,000 equity shares of Unicorn Packers Pvt. Ltd., i.e. in the ratio of 500:1, and the excess of the purchase consideration of Rs.555.75 crores over the net book value of assets and liabilities of Rs.87.01 crores of Unicorn Packers Pvt. Ltd. amounting to Rs.468.73 crores was recorded as goodwill in the books of Urmin Marketing Pvt. Ltd. and depreciation at 25% thereon was claimed for A.Y. 2015-16. In the subsequent amalgamation of Urmin Marketing Pvt. Ltd. with Urmin Flavoroma Pvt. Ltd., and the eventual change of name to Unicorn Pack

An indispensable Tool for Legal Professionals, Endorsed by Various High Court and Judicial Officers

Please visit our Training & Support

Center or Contact Us for assistance

Scan Me!

India’s Legal research and Law Firm App, Download now!

For Daily Legal Updates, Join us on :