INCOME TAX APPELLATE TRIBUNAL (DELHI BENCH)

C.N. PRASAD, Judicial Member, M. BALAGANESH, Accountant Member

Shayam Gupta – Appellant

Versus

DCIT – Respondent

ITA No.3134 to 3137/Del/2025

| Table of Content |

|---|

| 1. assessee appeals against cit(a) orders for ay 2018-19 to 2021-22. (Para 1 , 2) |

| 2. satisfaction note under s.153c lacks bearing on total income determination. (Para 3 , 4 , 5 , 6 , 9 , 10) |

| 3. revenue defends satisfaction note as properly recording unaccounted transactions. (Para 7 , 8) |

| 4. invalid s.153c satisfaction quashes assessments following precedents. (Para 11 , 12) |

| 5. assessments quashed for all years; appeals partly allowed. (Para 13 , 14 , 15) |

ORDER

PER C.N. PRASAD, JM,

These appeals are filed by the assessee against different orders of the Ld.Commissioner of Income Tax (Appeals)-30, New Delhi for the A.Y’s 2018-19 to 2021-22.

2. We first take the appeal for the A.Y. 2018-19 and the grounds of appeal are as under :-

1. On the facts and circumstances of the case and in law, the notice u/s 153C issued by the assessing officer is bad- in-law, barred by limitation and without jurisdiction and, therefore, the said notice along with the assessment order passed on the foundation of such notice are liable to be quashed and CIT(A) erred in not holding so.

2.On the facts and circumstances of the case and in law, the notice u/s 153C issued by the assessing officer is illegal and without jurisdiction. The assessing officer has not allied provisions for complied with the provisions of section 153C and other notice. Accordingly, the notice u/s 153C along with the issuance of such assessment order passed on the foundation of such notice are liable to be quashed and CIT(A) erred in not holding so.

3. On the facts and circumstances of the case and in law, the satisfaction note(s) recorded u/s 153C of the Act are bad-in-law and without jurisdiction and, accordingly, the assessment proceedings initiated on the foundation of such satisfaction note(s) and also the consequent assessment order passed are liable to be quashed and CIT(A) erred in not holding so.

4. On the facts and circumstances of the case and in law, the addition of Rs. 2,86,98,205/- made by the assessing officer on account of disallowance of purchases u/s 37 of the Act, is beyond the scope/jurisdiction of provisions of section 153C read with section 153A of the Income Tax Act, 1961 and CIT(A) erred in not holding so.

5. On the facts and circumstances of the case and in law, the Id. CIT(A) erred in confirming the addition made by the assessing officer of Rs. 2,86,98,205/- on account of disallowance of purchases u/s 37 of the Act.

6. On the facts and circumstances of the case and in law, the assessment order passed by the assessing officer is non-est as it does not have DIN on the body of the assessment order and CIT(A) erred in not holding so.

7.On the facts and circumstances of the case and in law, the assessment order passed by the assessing officer is contrary to the provisions of section 153D of the Income Tax Act, 1961 and CIT(A) erred in not holding so.

8. On the facts and circumstances of the case and in law, the CIT(A) erred in passing ex-parte order without giving proper opportunity of being heard and is against the principles of natural justice.

3. The Ld. Counsel for the assessee at the outset submitted that the satisfaction recorded by the AO in the case of the assessee for initiating proceedings u/s.153C r.w.s. 153A of the Act is bad in law and consequentially the assessment framed pursuant to such satisfaction note is also bad in law and void ab initio. The Ld. Counsel for the assessee referring to the satisfaction note recorded in the case of the assessee, submitted that the AO nowhere in the satisfaction note stated that the materials seized and belonging to the assessee would have a bearing on determination of the total income of the assessee. Therefore, in the absence of such recording of satisfaction as contemplated under the provisions of section 153C of the Act the satisfaction note recorded by the AO is bad in law.

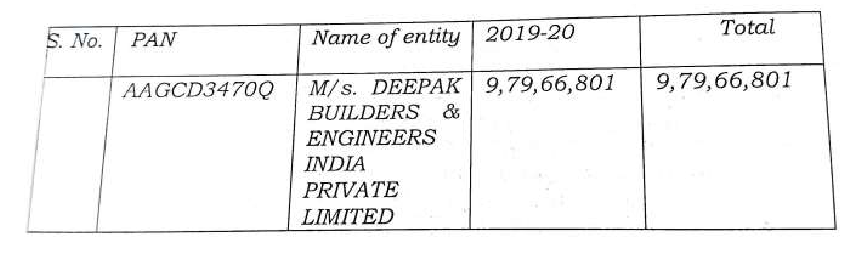

4. The Ld. Counsel for the assessee further placing reliance on the decision of the coordinate bench in the case of M/s. Deepak Builders an

An indispensable Tool for Legal Professionals, Endorsed by Various High Court and Judicial Officers

Please visit our Training & Support

Center or Contact Us for assistance

Scan Me!

India’s Legal research and Law Firm App, Download now!

For Daily Legal Updates, Join us on :