INCOME TAX APPELLATE TRIBUNAL (HYDERABAD BENCH)

Vijay Pal Rao, Vice-President, Manjunatha G., Accountant Member

Fayaz Mohammed – Appellant

Versus

Dy.CIT HYDERABAD Central Circle 2(4) – Respondent

| Table of Content |

|---|

| 1. introductory details and grounds of appeal. (Para 1 , 2) |

| 2. factual background of search and cash payment addition. (Para 3 , 4 , 5 , 6) |

| 3. assessee argues section 153c notice time-barred. (Para 7 , 8) |

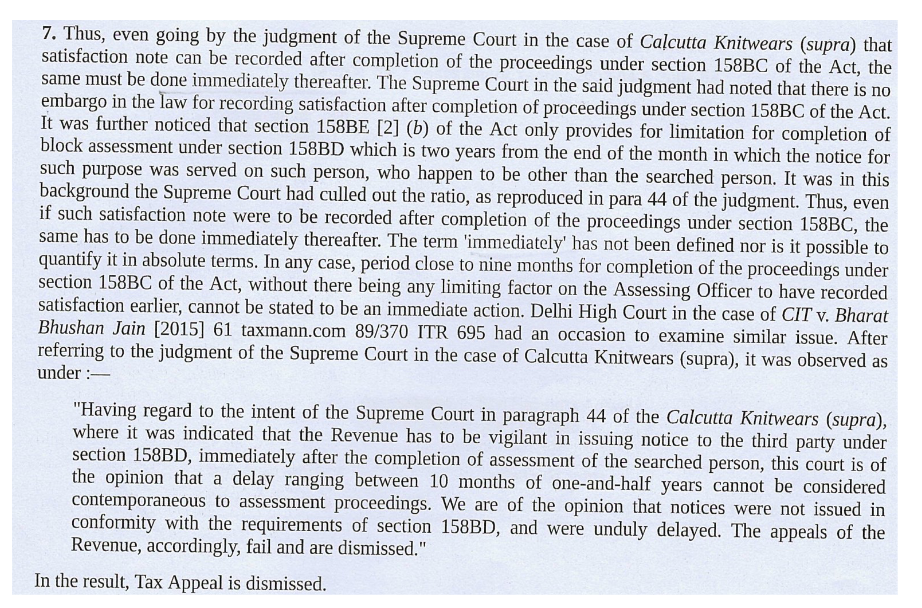

| 4. revenue defends timely section 153c satisfaction. (Para 9) |

| 5. court analyzes calcutta knitwears on satisfaction timing. (Para 10 , 11 , 12 , 13 , 14) |

| 6. section 153c notice invalid after 10 months. (Para 15) |

| 7. merits grounds infructuous; appeal allowed. (Para 16 , 17) |

| 8. identical relief for ay 2018-19. (Para 18 , 19 , 20) |

आदेश/ORDER

Per MANJUNATHA, G. A.M.

These two appeals are filed by the assessee are directed against the separate orders passed by the Learned Commissioner of Income Tax (Appeals)-12, Hyderabad, all dated 08/08/2025, for the Asst. Years 2017-18 and 2018-19. Since identical issues are raised by the assessee in these two appeals, for the sake of convenience, these appeals were heard together and are being disposed off, by this common consolidated order.

ITA No.1671/Hyd/2025 A.Y 2017-18

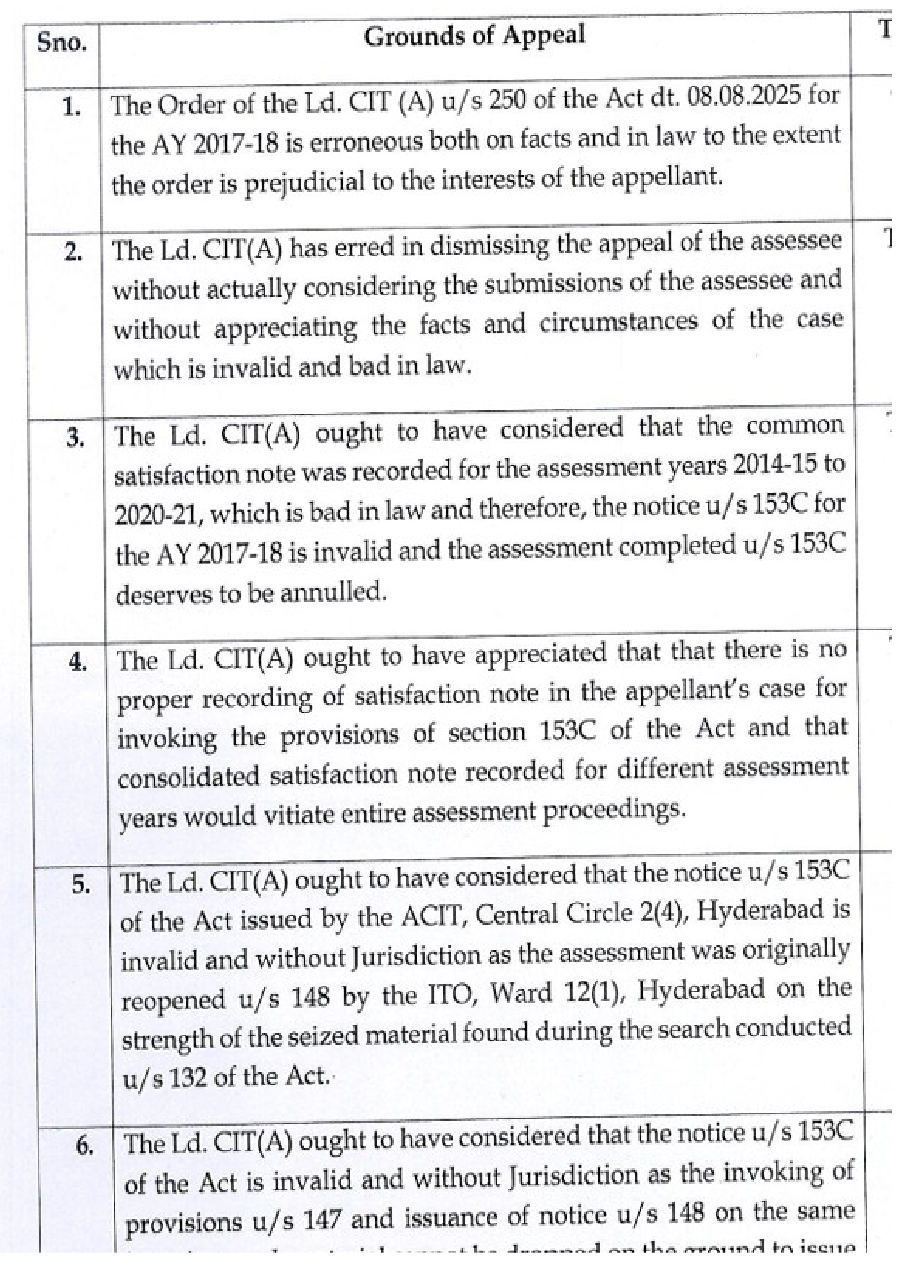

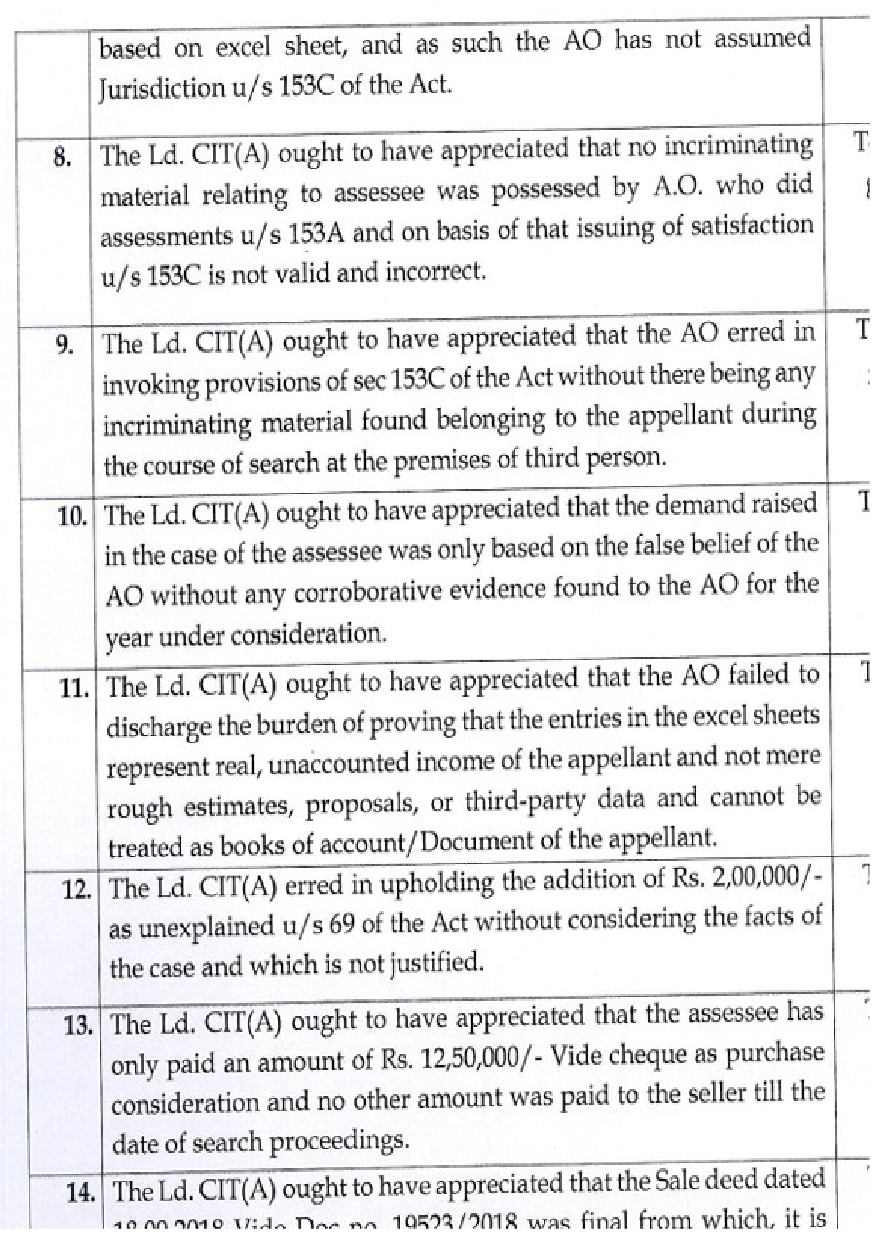

2. The assessee has raised the following grounds of appeal:

3. The brief facts of the case are that the assessee, an individual, filed his return of income for the A.Y 2017-18

An indispensable Tool for Legal Professionals, Endorsed by Various High Court and Judicial Officers

Please visit our Training & Support

Center or Contact Us for assistance

Scan Me!

India’s Legal research and Law Firm App, Download now!

For Daily Legal Updates, Join us on :