INCOME TAX APPELLATE TRIBUNAL (RAIPUR BENCH)

Partha Sarathi Chaudhury, J

Raman Vasu Thachisaril Ramanalayam Clappana – Appellant

Versus

Income Tax Officer, Ward-Jagdalpur – Respondent

| Table of Content |

|---|

| 1. condonation of 396-day appeal delay granted. (Para 1 , 2 , 3) |

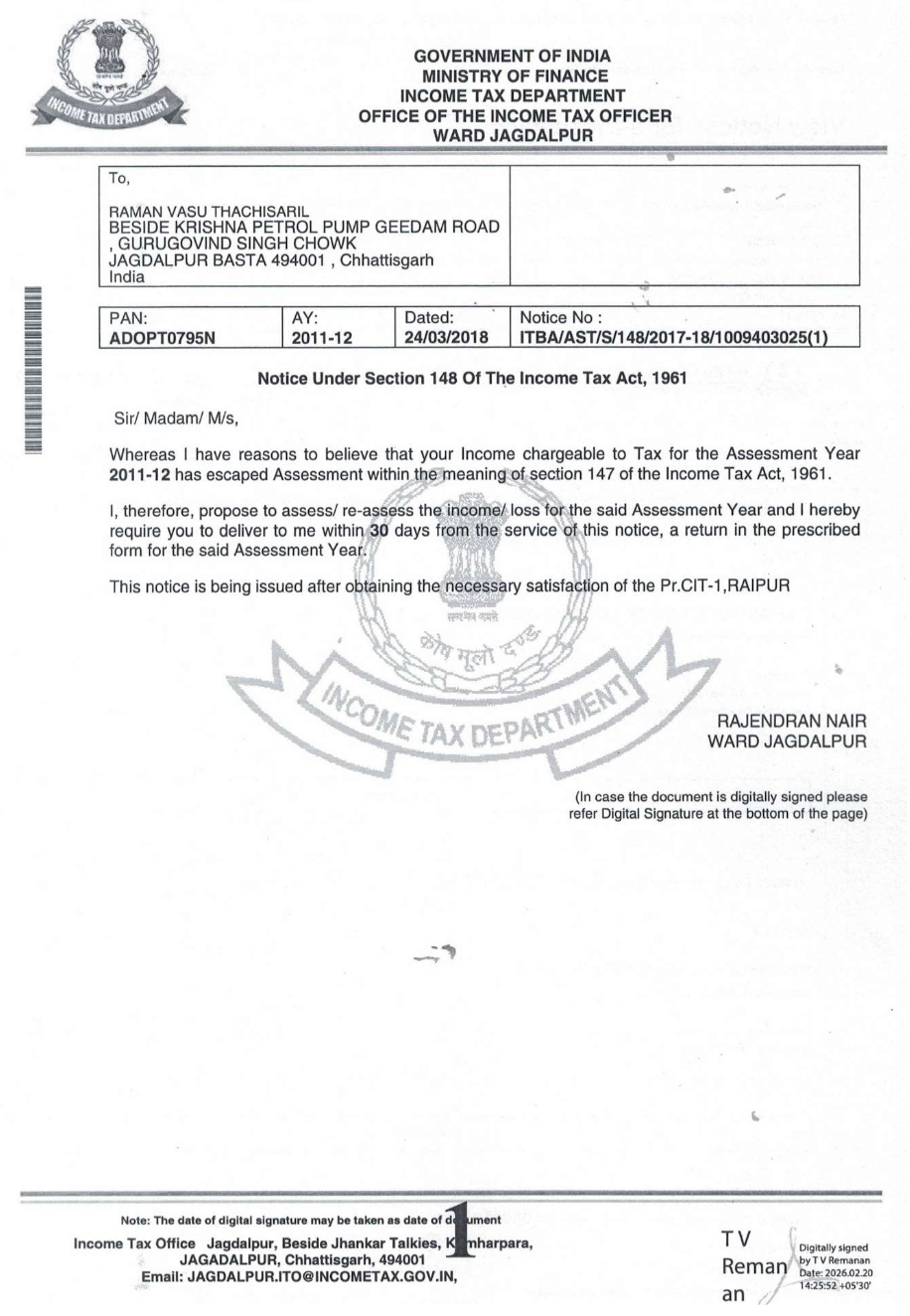

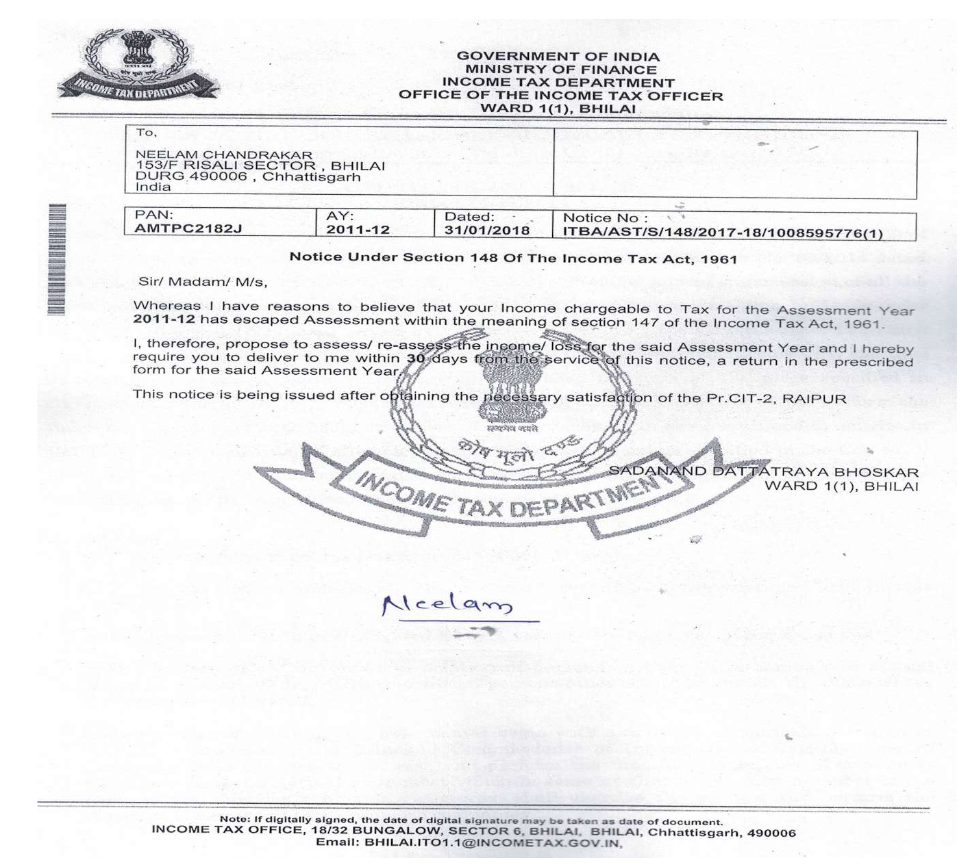

| 2. unsigned s.148 notice lacks authority signature. (Para 4 , 5 , 6) |

| 3. unsigned notices violate mandatory s.282a(1) signing. (Para 7 , 8) |

| 4. unsigned s.148 notice invalidates reassessment jurisdiction. (Para 9 , 10) |

| 5. reassessment quashed; appeal allowed. (Para 11 , 12 , 13) |

आदेश/ORDER

PER PARTHA SARATHI CHAUDHURY, JM

The present appeal preferred by the assessee emanates from the order of the Ld.CIT(Appeals)/NFAC, dated 14.10.2024 for the assessment year 2011-12 as per the grounds of appeal on record.

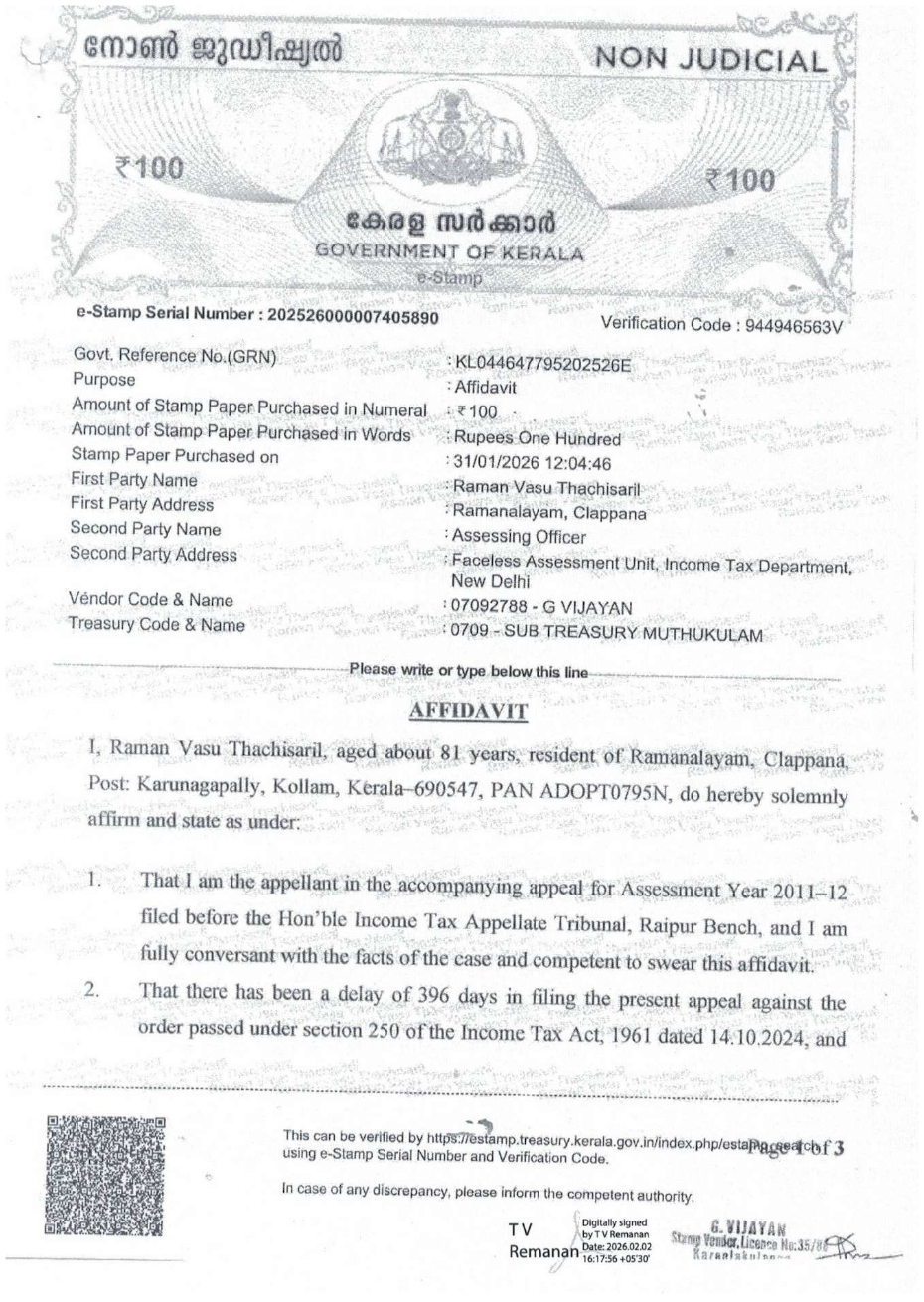

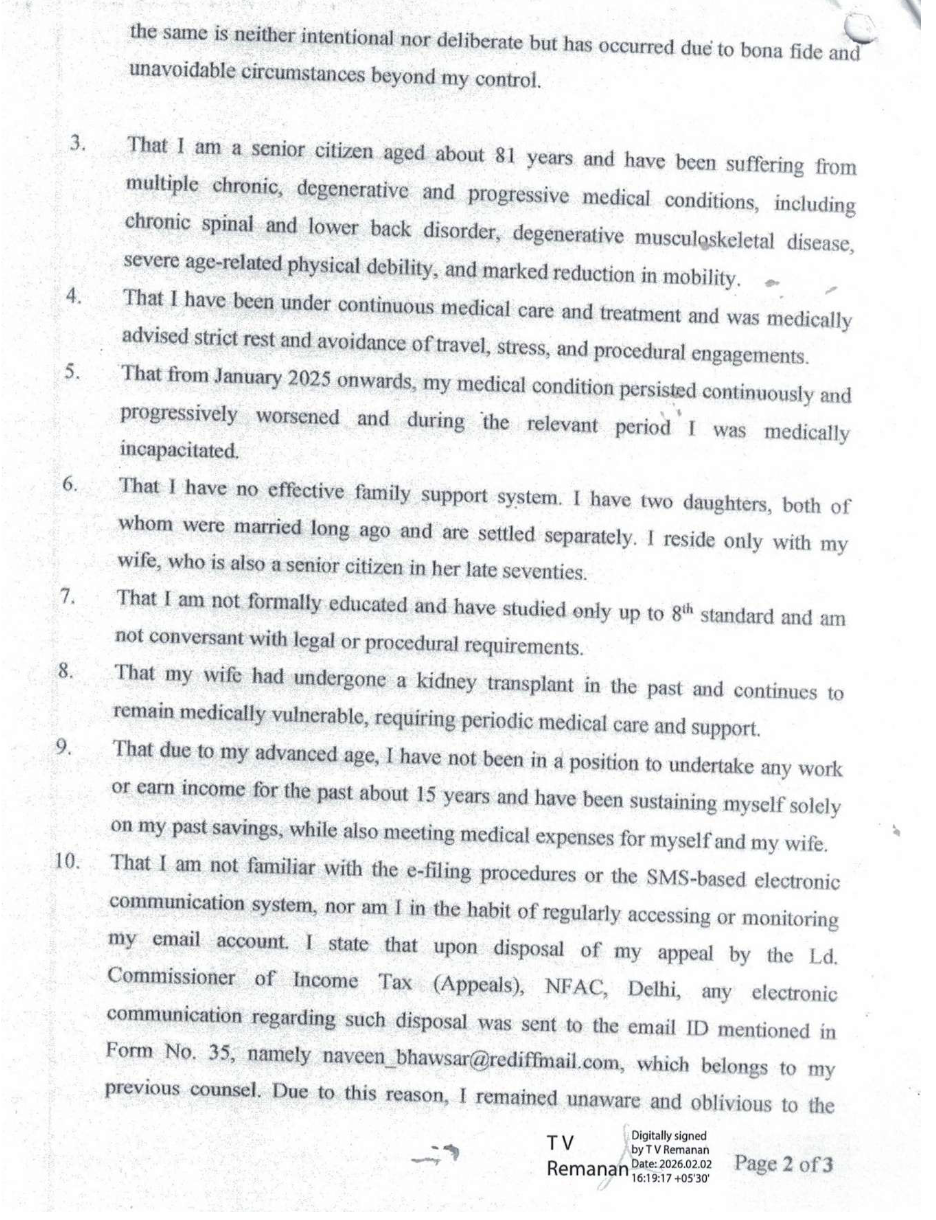

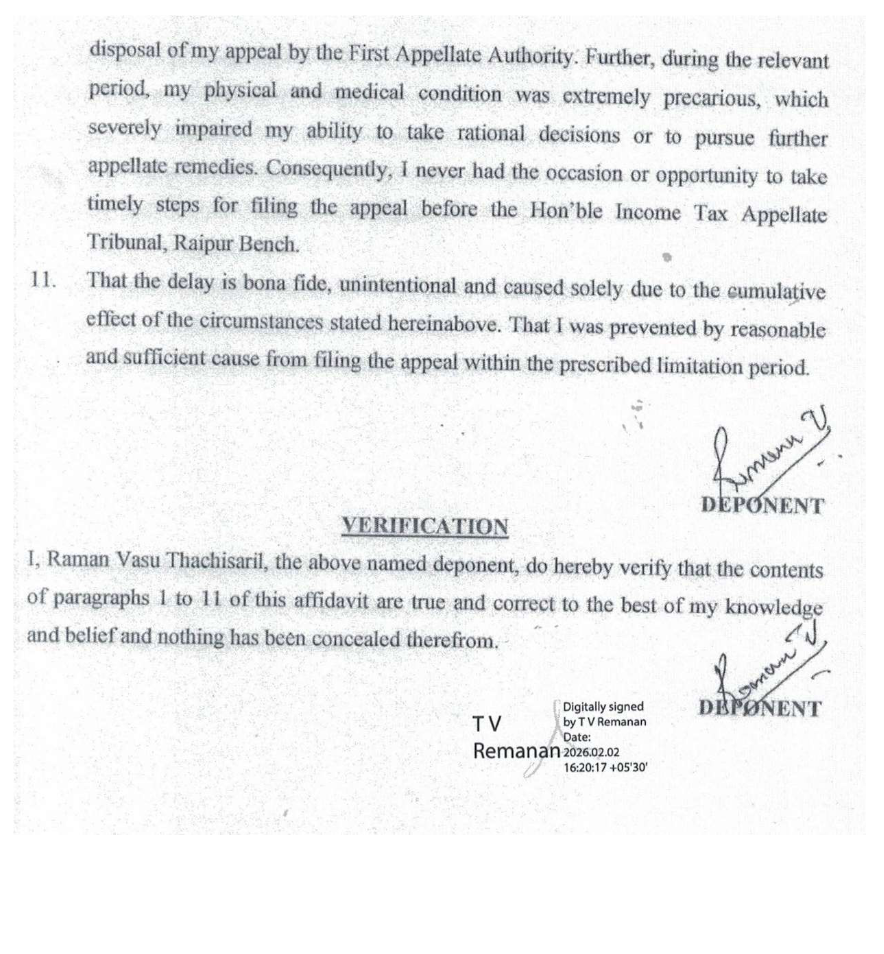

2. At the very outset, it is noted that there is delay of 396 days in filing appeal before the Tribunal. That explaining the reasons for such delay and praying for condonation of the same, the assessee had filed condonation petition a/w. affidavit, dated 02.02.2026 and medical certificates. The relevant contents of the said affidavit are extracted as follows:

3. I have carefully perused the contents of the affidavit and condonation petition as well as medical certificates and heard the submissions of the parties herein. In my considered view, there is no deliberate or malafide conduct on the part of the assessee

An indispensable Tool for Legal Professionals, Endorsed by Various High Court and Judicial Officers

Please visit our Training & Support

Center or Contact Us for assistance

Scan Me!

India’s Legal research and Law Firm App, Download now!

For Daily Legal Updates, Join us on :