INCOME TAX APPELLATE TRIBUNAL (INDORE BENCH)

B.M. Biyani, Accountant Member, Paresh M. Joshi, Judicial Member

Madhya Pradesh Industrial Foundation – Appellant

Versus

CIT (Exemption ) – Respondent

ITA No.147/Ind/2025 | ITA No.148/Ind/2025

| Table of Content |

|---|

| 1. appeals against rejection of 12ab/80g registration (Para 1 , 2) |

| 2. delay condoned applying sufficient cause principle (Para 3) |

| 3. cit(e) rejected applications due to wrong provisional code (Para 4 , 5) |

| 4. bona fide technical mistake not ground for rejection (Para 6 , 7) |

| 5. remanded for fresh consideration on merits (Para 8) |

आदेश/ORDER

Per B.M. Biyani, A.M.:

The captioned two (2) appeals, first being ITA No. 147/Ind/2025 relating to registration u/s 12AB and second being ITA No. 148/Ind/2025 relating to approval u/s 80G, are filed by assessee challenging two (2) separate orders bearing DIN: ITBA/EXM/F/EXM45/2024-25/1068639015(1) and DIN: ITBA/EXM/F/EXM45/2024-25/1068639139(1), both dated 12.09.2024 and passed by learned Commissioner of Income-Tax (Exemption), Bhopal [“CIT(E)”] in respective Form No. 10AD, by which the assessee’s applications in Form No. 10AB for grant of final registration u/s 12AB & final approval u/s 80G of Income-tax Act, 1961 [“the act”] have been rejected and the provisional registration u/s 12AB & provisional approval u/s 80G granted earlier by Central Processing Cell of Income-tax Department [“CPC”] have also been cancelled. The assessee has raised the grounds as mentioned in respective Appeal Memos (Form No. 36).

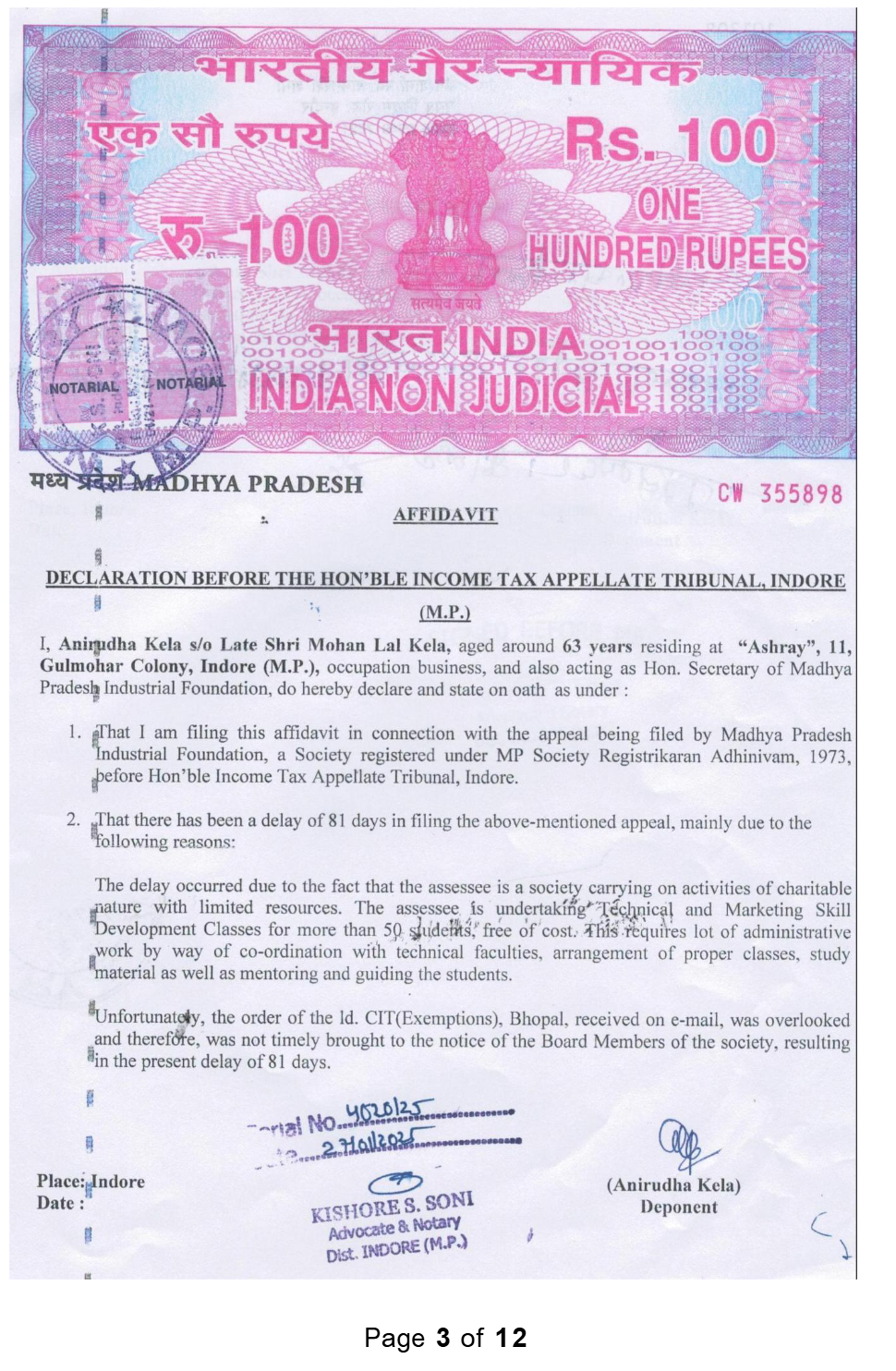

2. The registry has informed that the present appeals are delayed and therefore time-barred. The assessee has filed an application/affidavit for condonation of delay; the same is scanned and re-produced for an immediate reference:

3. The averments made by assessee in above affidavit, which are self- explanatory and which do not require repetition, were discussed and the Ld. DR for revenue does not have any objection if the bench condones delay and accordingly left it to the wisdom of bench. We have considered the explanation advanced by assessee and in absence of any contrary fact or material on record, the assessee is found to have a “sufficient cause” for delay in filing present appeal. We find that section 253(5) of the Act empowers the ITAT to admit an appeal after expiry of prescribed time, if there is a “sufficient cause”for not presenting appeal within prescribed time. It is also a settled position by Hon’ble Supreme Court in Collector, Land Acquisition Vs Mst. Katiji and others 1987 AIR 1353, 1987 2 SCC 387 that whenever substantial justice and technical considerations are opposed to each other, the cause of substantial justice must be preferred by adopting a justice-oriented approach. Thus, taking into account the facts of case, the provision of section 253(5) and the decision of Hon’ble Supreme Court, we take a judicious view, condone delay, admit appeal and proceed with hearing.

4. We have heard the learned Representatives of both sides and perused the case record including the impugned orders.

5. In these matters, the assessee is aggrieved by the action of CIT(E) in rejecting assessee’s applications for registration u/s 12AB and approval u/s 80G. The Ld. CIT(E) has rejected assessee’s application for final registration u/s 12AB on a technical reason that the assessee was existing since 19.10.1965 and therefore not eligible to obtain provisional registration u/s 12AB under “Item (A) of section 12A(1)(ac)(vi)”. The Ld. CIT(E) has assigned similar technical reason for rejecting assessee’s application for final approval u/s 80G by stating that the assessee was existing since 19.10.1965, therefore it was not eligible to obtain provisional registration u/s 80G under “Item (A) of clause (iv) of first proviso to sub-section (5) of section 80G”. Assigning these reasons, the Ld. CIT(E) rejected applications for final registration u/s 12AB/final approval u/s 80G and also cancelled the provisions registration u/s 12AB/provisional approval u/s 80G. For the sake of immediate reference, we re-produce below the order passed by CIT(E) in the matter of section 12AB:

“Annexure (mentioned in row-9 above)

The assessee has applied in Form 10AB for registration u/s 12AB under the new provision of I

An indispensable Tool for Legal Professionals, Endorsed by Various High Court and Judicial Officers

Please visit our Training & Support

Center or Contact Us for assistance

Scan Me!

India’s Legal research and Law Firm App, Download now!

For Daily Legal Updates, Join us on :