INCOME TAX APPELLATE TRIBUNAL (BANGALORE BENCH)

WASEEM AHMED, Accountant Member, KESHAV DUBEY, Judicial Member

Jadagadder Pakkerappa Legal Heir: Sarojamma – Appellant

Versus

ITO Ward 1 & TPS Karnataka Shikaripura (Tq) – Respondent

| Table of Content |

|---|

| 1. factual background of reassessment and non-response (Para 1 , 3 , 4 , 5 , 6) |

| 2. parties' contentions on notice validity post-death (Para 7 , 8) |

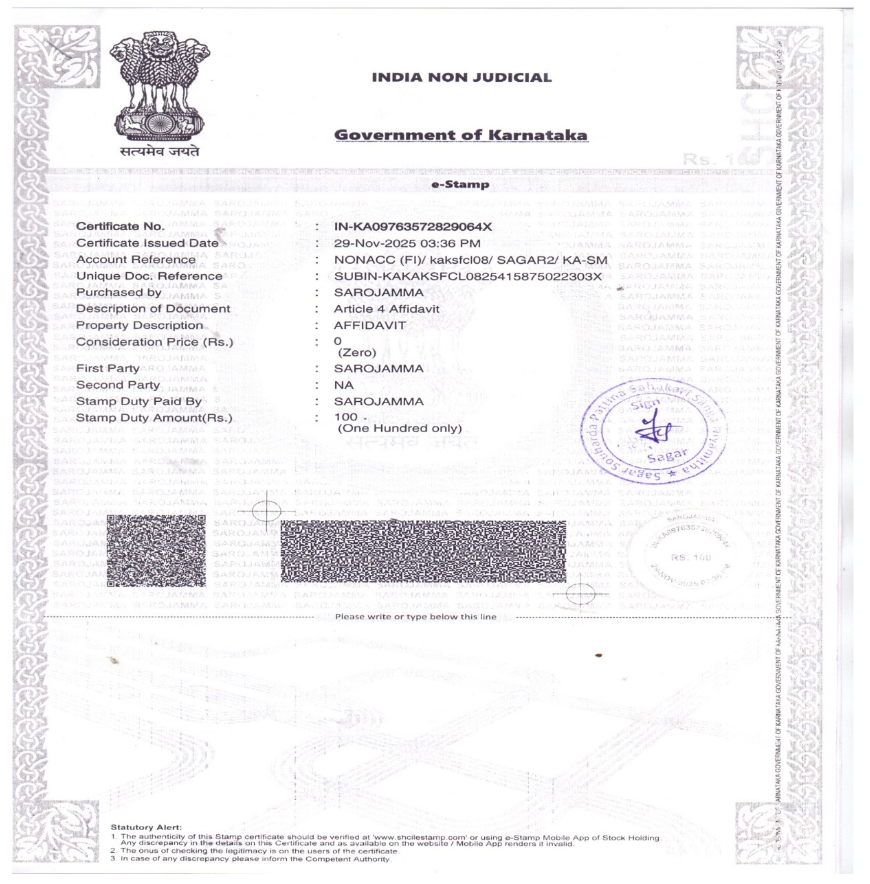

| 3. affidavit and undisputed death facts noted (Para 9) |

| 4. appeal allowed; reassessment quashed (Para 10) |

ORDER

PER KESHAV DUBEY, JUDICIAL MEMBER:

This appeal at the instance of the assessee is directed against the order of ld. CIT(A)/NFAC dated 27.5.2025 vide DIN & Order No.ITBA/NFAC/S/250/2025-26/1076474053(1) passed u/s 250 of the Income Tax Act, 1961 (in short “The Act”) for the assessment year 2016-17.

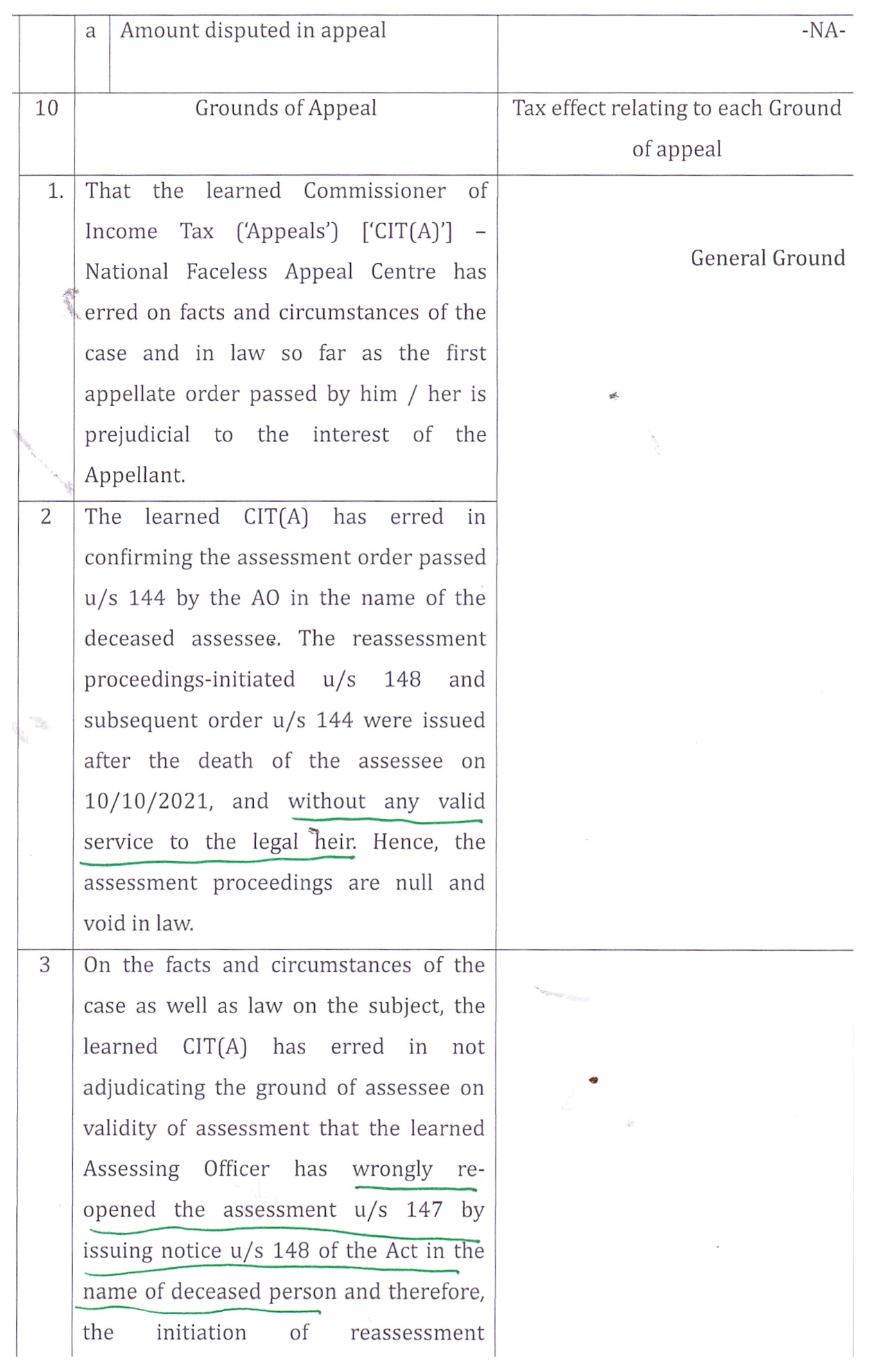

2. The assessee has raised the following grounds of appeal:

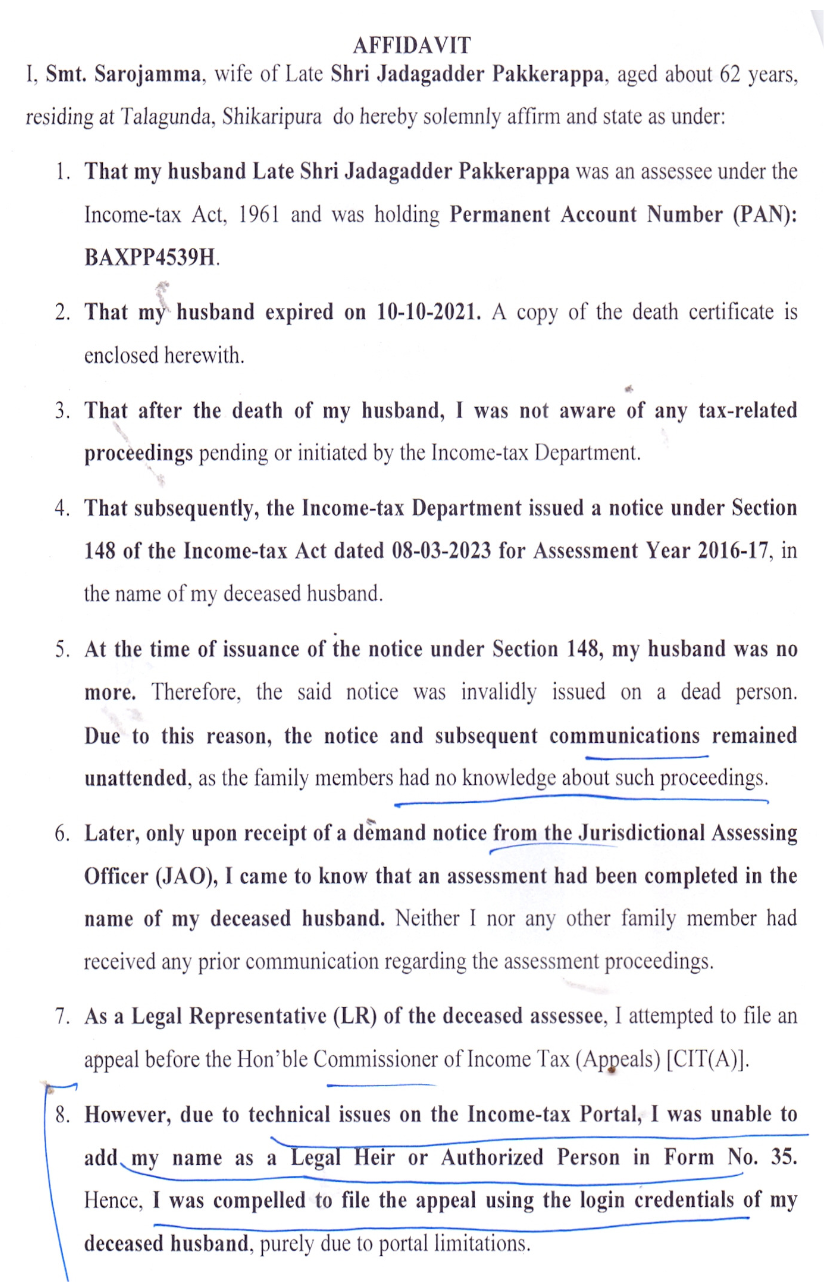

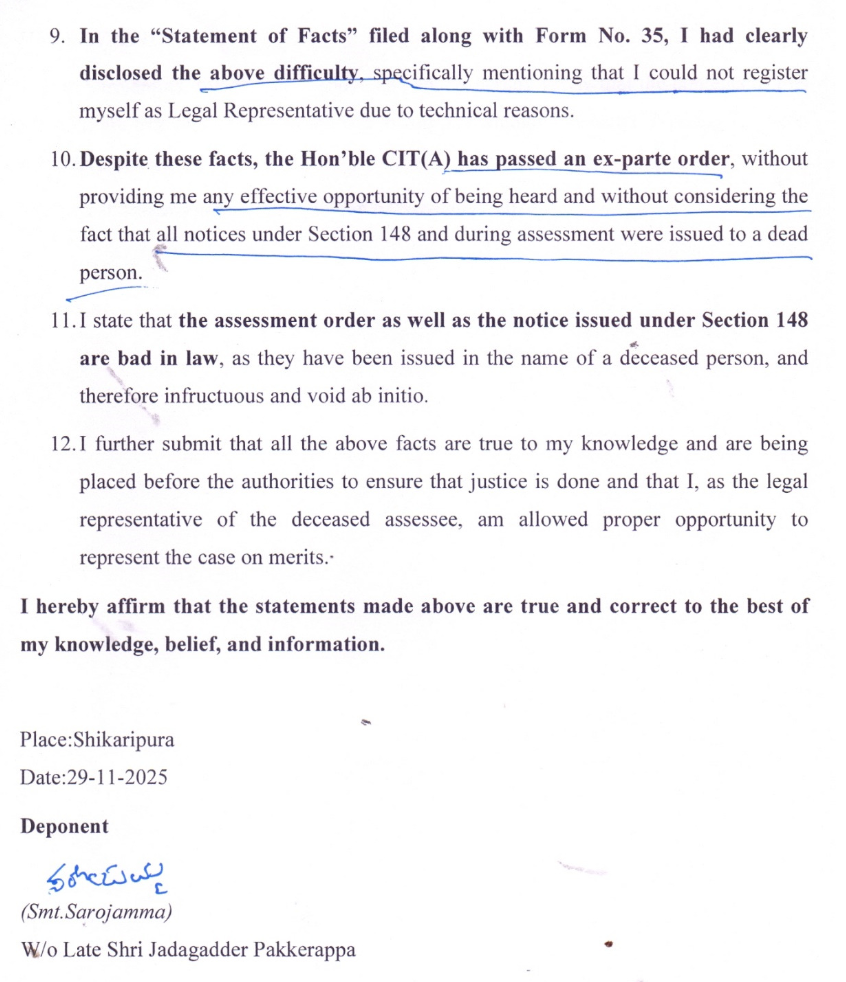

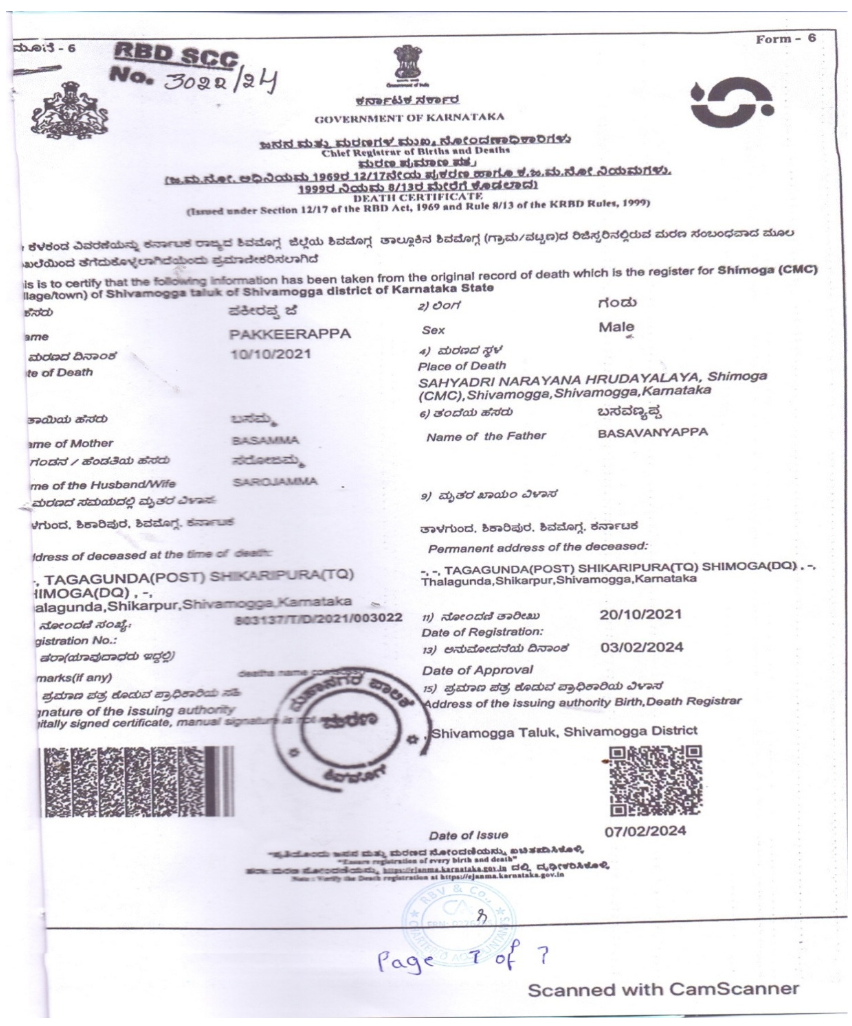

3. The assessee late Shri Jadagadder Pakkerappa represented by his wife and legal heir Smt. Sarojamma filed this appeal against the order of ld. CIT(A)/NFAC dismissing the appeal on the ground that the assessee neither produced any evidence nor complied with the various notices issued during the entire appellate proceedings. Brief facts of the case are that as per the information available on record, the AO observed that the assessee had sold an immovable property amounting to Rs.60,00,000/- during the year under consideration. However, on verification of e-filing port

An indispensable Tool for Legal Professionals, Endorsed by Various High Court and Judicial Officers

Please visit our Training & Support

Center or Contact Us for assistance

Scan Me!

India’s Legal research and Law Firm App, Download now!

For Daily Legal Updates, Join us on :