INCOME TAX APPELLATE TRIBUNAL (PUNE BENCH)

DIPAK P. RIPOTE, Accountant Member, VINAY BHAMORE, Judicial Member

Nitin Arjun Pawar – Appellant

Versus

Income Tax Officer – Respondent

ITA No.1925/PUN/2025

| Table of Content |

|---|

| 1. s.149 bars s.148 notice beyond 3 years if escapement |

| 2. cash deposits sourced from agricultural land sale, accepted but misquantified. (Para 2 , 4 , 5 , 6 , 7 , 8 , 9) |

| 3. s.148 notices post-01.04.2021 for a.y.2015-16 invalid per sc concession. (Para 13 , 14 , 15 , 16 , 17 , 18 , 19 , 20) |

| 4. notice and assessment quashed; appeal allowed. (Para 21 , 22) |

आदेश/ ORDER

PER DR. DIPAK P. RIPOTE, AM:

This is an appeal filed by the Assessee against the order of ld.Commissioner of Income Tax(Appeal)[NFAC], passed under section 250 of the Income Tax Act, 1961 for the A.Y.2015-16 dated 11.07.2025 emanating from the Assessment Order passed under section 147 read with section 144B of the I.T.Act, dated 15.11.2023. The Assessee has raised the following grounds of appeal :

“1. On the facts and in the circumstances of the case and in law, Ld. AO erred in initiating the reassessment proceedings u/s. 147 and consequential order passed u/s 147 rws 144 are bad in law as the notice u/s 148 was issued by Income Tax Officer, (Jurisdictional Assessing Officer-JAO) and the assessment order is completed by Faceless Assessing Officer-FAO which is not permitted as per provisions of section 151A and therefore entire proceeding are void-ab-initio and therefore consequential order are bad in law

2. The notice issued u/s 148 in the instant case is bad in law, being not issued through automated allocation, in accordance with risk management strategy formulated by the Board as referred to in section 148 of the Act and therefore, the order passed u/s 147 rws 1448 may be declared as null and void.

3. The order passed u/s 148A(d) as well as notice issued u/s 148 without conducting requisite enquiries before issue of notice u/s 148 of the Act please be quashed and, therefore the order passed u/s. 147 rw s. 1448 may be declared as null and void

4. On the basis of facts, in the circumstances of the case and in view of the express provisions of Section 149, notice issued u/s 148 on 05/04/2022 for alleged escapement of income of Rs. 25,00,000/- is bad in law as no notice u/s 148 can be issued in this case, since three years have elapsed from the end of A.Y 2015-16 and the amount escaping assessment is less than Rs 50 lakhs. Therefore, order passed u/s 147 may please declared as null and void

5. On the basis of facts, in the circumstances of the case and as per law, the addition of Rs 25,00,000/-made on account of unexplained money u/s 69A be deleted as the same is made without appraising the fact, submissions as well as evidences furnished by the appellant

6 On the basis of facts and in the circumstances of the case the demand raised pursuant to order passed u/s 147 r.w.s. 1448 please be stayed Your appellant prays for deletion of entire addition.

Your appellant craves for to add, alter amend, modify, delete any or all grounds of appeal before or during the course of hearing in the interest of principle of natural justice.”

Submission of ld.AR :

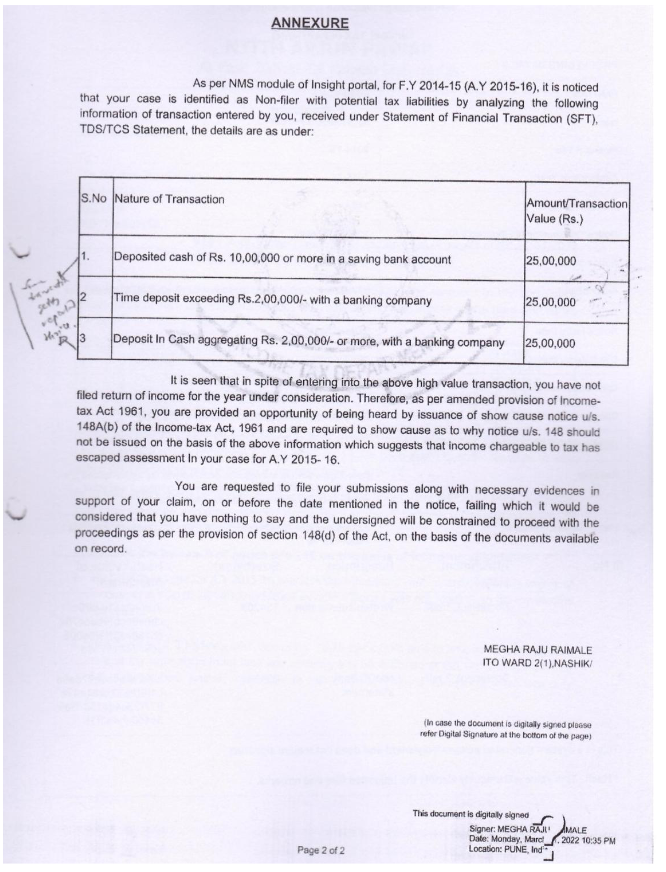

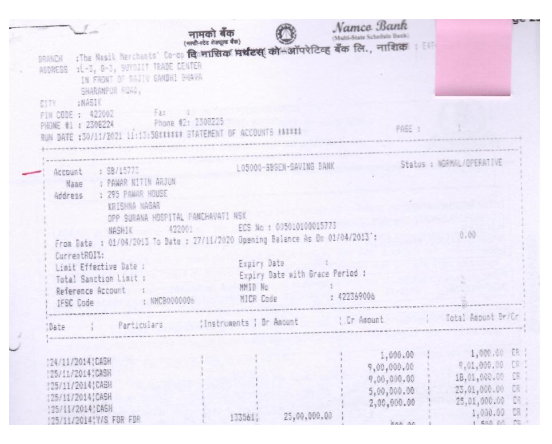

2. Ld.AR filed a paper book. Ld.AR submitted that the Assessing Officer has issued notice u/s.148A(b) of the Act, and then passed an order us/.148A(d) on 04.04.2022 for A.Y.2015-16 alleging escapement of income of Rs.75,00,000/-. Ld.AR invited our attention to the submission made by Assessee in response to notice u/s.148A(b) of the Act, wherein, Assessee has clearly explained that the cash deposited of Rs.25,00,000/- was transferred and kept as fixed deposits. This fact has been accepted by the Assessing Officer in the order u/s.148A(d) of the Act. Ld.AR therefore, further submitted that there were total deposits only of Rs.25,00,000/- which has been reported by banks under various heads which made Assessing Officer think it to be Rs.75,00,000/-. Ld.AR submitted that all these facts have been submitted by Assessee to the Assessing Officer during the proceedings initially under Section 133(6) and then under section 148A(b) of the Act. Ld.AR invited our attention to the submission made by Assessee in r

An indispensable Tool for Legal Professionals, Endorsed by Various High Court and Judicial Officers

Please visit our Training & Support

Center or Contact Us for assistance

Scan Me!

India’s Legal research and Law Firm App, Download now!

For Daily Legal Updates, Join us on :