INCOME TAX APPELLATE TRIBUNAL (INDORE BENCH)

B.M. Biyani, Accountant Member, Paresh M Joshi, Judicial Member

DCIT-4(1), Indore – Appellant

Versus

Maral Overseas Ltd. – Respondent

ITA No.571/Ind/2025 (AY: 2006-07)

| Table of Content |

|---|

| 1. factual background of assessment and cit(a) allowing gratuity deduction. (Para 1 , 2) |

| 2. revenue appeal dismissed. (Para 5) |

आदेश/ORDER

Per Paresh M Joshi, J.M.:

This is an Appeal filed by the Assessee under section 253 of the income tax Act 1961,[ herein after referred to as the Act for the sake of brevity] before this tribunal as & by way of a second Appeal. The Assessee is aggrieved by the order bearing Number:-1046/2021-22 dated 29.07.2022[DR No. 39/12 D No. 427] passed by the Ld. CIT(A) u/s 250 of the Act, which is herein after referred to as the “Impugned order”. The Relevant Assessment year is 2006-07 and the corresponding previous year period is from 01.04.2005 to 31.03.2006.

2. Factual Matrix

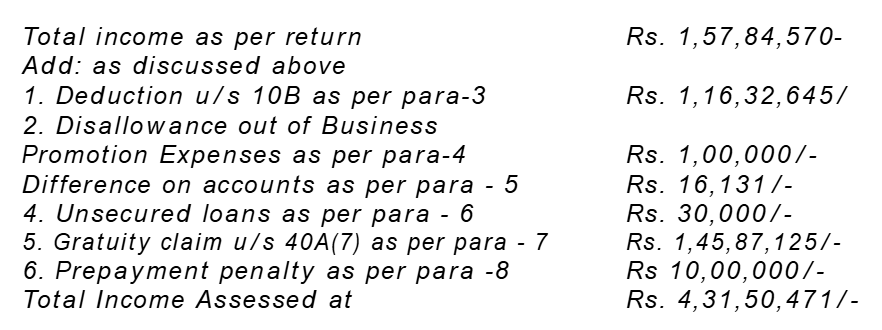

2.1 That as and by way of an assessment order made u/s 143(3) of the Act the balance losses of AY 2005-06 were carried forwarded to Rs. 20,20,76,816/-. The total Income as per the ROI was at Rs. 1,57,87,570/-. The Ld. AO in the aforesaid assessment order has made following additions as below:-

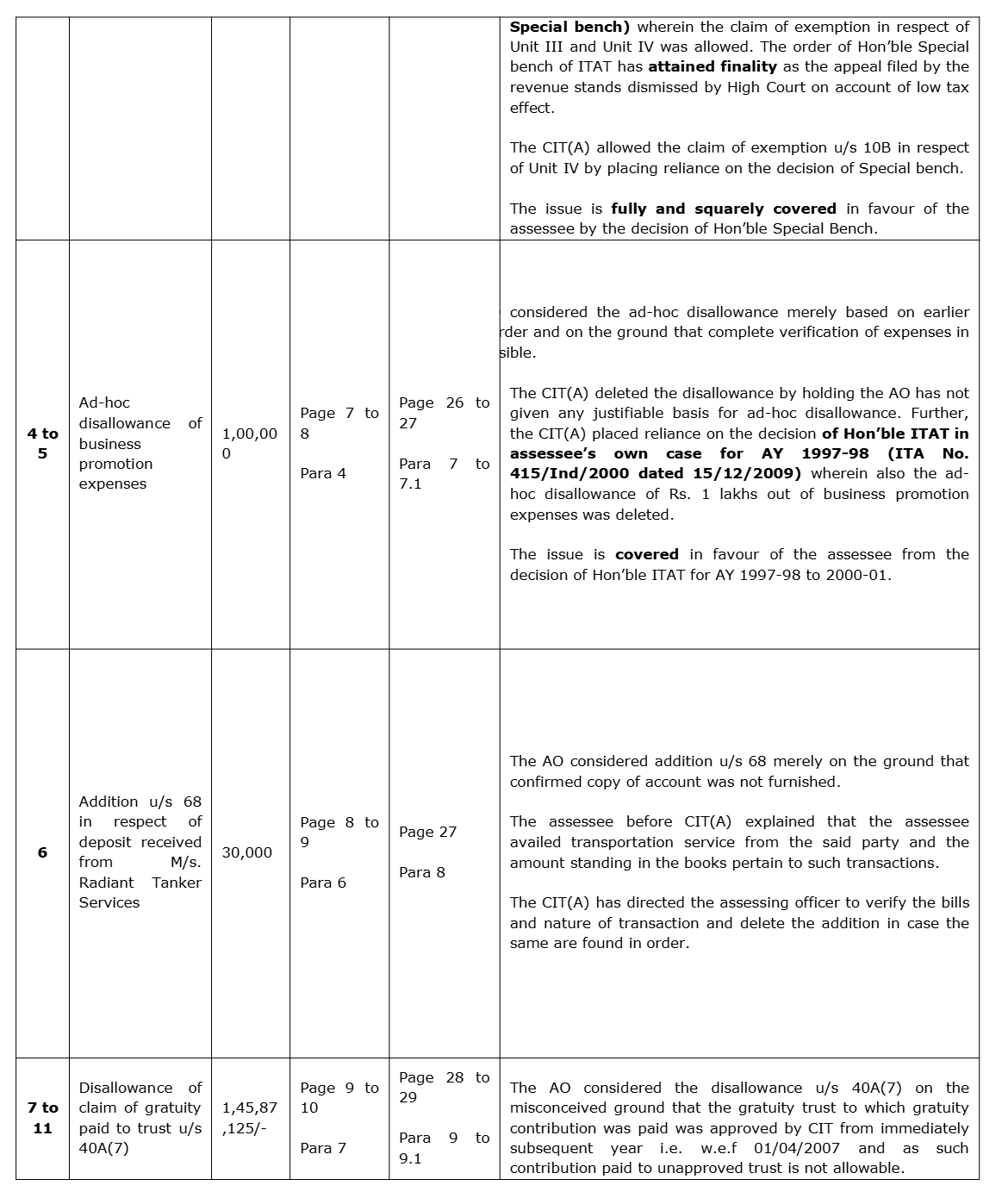

The total income was assessed at Rs. 4,31,50,471/-. Less set off of b/F losses as per order u/s 143(3) dated 29.12.2007 of AY 2005-06 Rs. 24,52,27,287/-.That the aforesaid assessment order was dated 24.12.2008 which is here in after referred to as the “Impugned assessment order”. The core issue was under caption gratuity claim u/s 40A(7) wherein para 7 of the “Impugned assessment order” the Ld. AO had held as follows:-

7.“Gratuity claim u/ s 40A(7) Assessee has claim gratuity u/ s 40A(7) Rs. 1,45,87,125/ -. Assessee has filed the application for approval of gratuity trust with income tax authorities for which approval was not received during the year. Assessee was asked to explain the claim of gratuity u/ s 40A(7). Assessee in its written submission dated 25.08.2008 stated that:-

"The claim of Rs. 1,45,67,125/ - is allowable to the assessee company as per clause (b) of section 40A(7). The gratuity fund set up for the employees of the company has been, subsequently granted approval by the Hon'ble Commissioner of Income Tax, Range-11, Indore w.e.f. 01.04.2007, It may be clarified that the assessee company has applied for the approval of its Gratuity trust to the Income lax Department way back in April, 2004. In view of the matter and also in light of the specific provisions of section 40A(7)(b), the same allowable, Since gratuity fund set up by the company for the employees was not approved by competent authority and assessee got approval w.e.f. 01.04.2007, it is not a approved gratuity fund. Therefore claim of assessee u/ s 40A(7), for gratuity is not allowable. It is also not allowable as per u/ s 40A(9) also which is reproduced as under:-

"No deduction shall be allowed in respect of any sum paid by the assessee as an employer towards the setting up or formation of, or as contribution to, any fund, trust, company, association of persons, body of individuals, society registered under the Societies Registration Act, 1860(21 of 1860), or other institution for any purpose, except where such sum is so paid, for the purposes and to the extent provided by or under clause (iv) or clause (v) or clause (v) of sub-section (1) of section 36, or, as required by or under any other law for the time being is force", The contribution of Rs. 1,45,87,125/ - was not made by the assessee in approved gratuity found, it is being disallowed and an amount of Rs. 1,45,87,125/ -is added back to the taxable income of the assessee.”

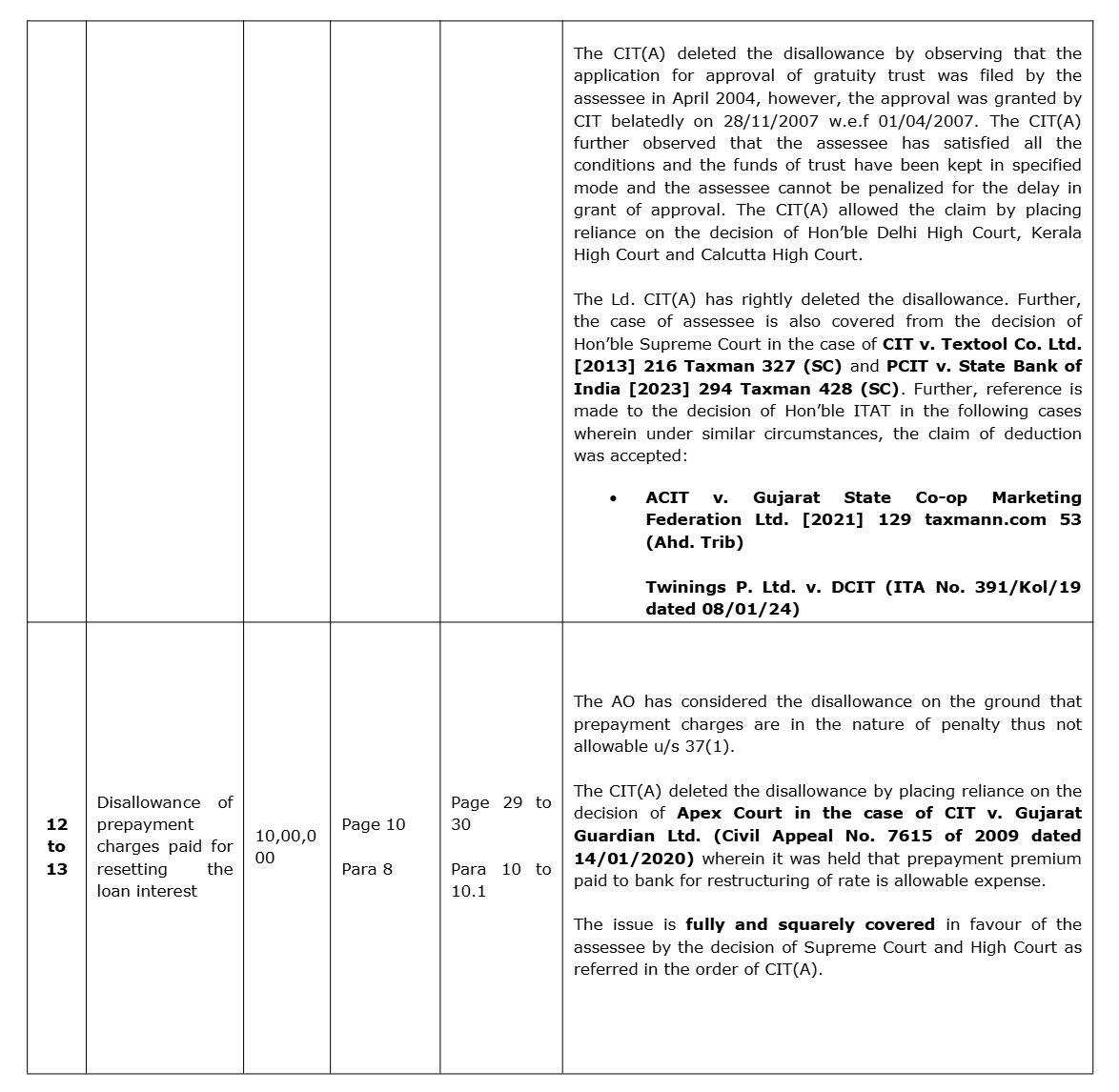

2.2 That the assessee being aggrieved by the aforesaid “Impugned assessment order” prefers the first appeal u/s 246A of the act before the Ld. CIT(A) who by the “Impugned order” has allowed the first appeal of the assessee on the grounds & reasons stated therein. In respect of core issue of gratuity claim u/s 40A(7) the Ld. CIT(A) in the “Impugned order” had held as under:-

“9. Ground no. 4 is related to disallowance u/ s 40A(7) of Rs. 1,45,87,125/ -. During the year under consideration the appellant had made a contribution of Rs. 1,

An indispensable Tool for Legal Professionals, Endorsed by Various High Court and Judicial Officers

Please visit our Training & Support

Center or Contact Us for assistance

Scan Me!

India’s Legal research and Law Firm App, Download now!

For Daily Legal Updates, Join us on :