INCOME TAX APPELLATE TRIBUNAL (MUMBAI BENCH)

JAYESH KANUNGO HUF KHETWADI MUMBAI – Appellant

Versus

ITO-19(2)(1) PAREL MUMBAI – Respondent

आदेश/ORDER

PER ANIKESH BANERJEE [J.M]:

Instant appeal of the assessee was preferred against the order of the National Faceless Appeal Centre (NFAC), Delhi [hereinafter referred to as "Ld. CIT(A)"] order passed u/s. 250 of the Income Tax Act, 1961 [hereinafter referred to as "Act"] order passed for the Assessment Year 2014-15 date of order 17.09.2025. The impugned order emanated from the order of the Ld. ITO-19(2)(1), Mumbai [hereinafter referred to as "Ld. AO"], order passed u/s.143(3) r.w.s. 147 date of order 30.12.2017.

2. The assessee has taken the following grounds:

“1. That on facts and circumstances of the case and in law the id. C.I.T. (Appeals), NFAC, Delhi has erred in not quashing the impugned assessment order dated 30/12/2017 passed u/s.143(3) r.w.s.147 by ld. Income Tax Officer-19(2)(1), Mumbai on either of or on all the following grounds:

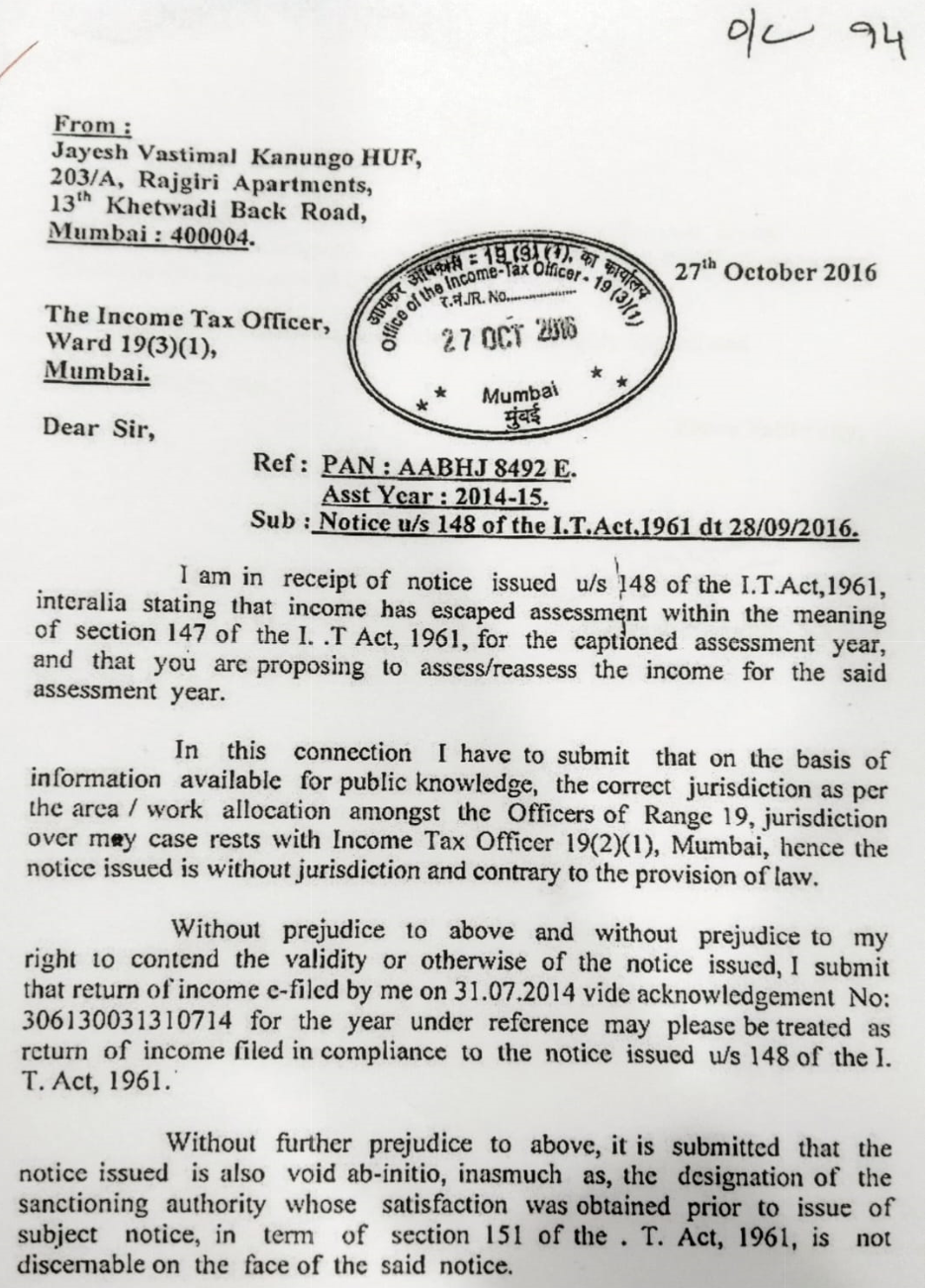

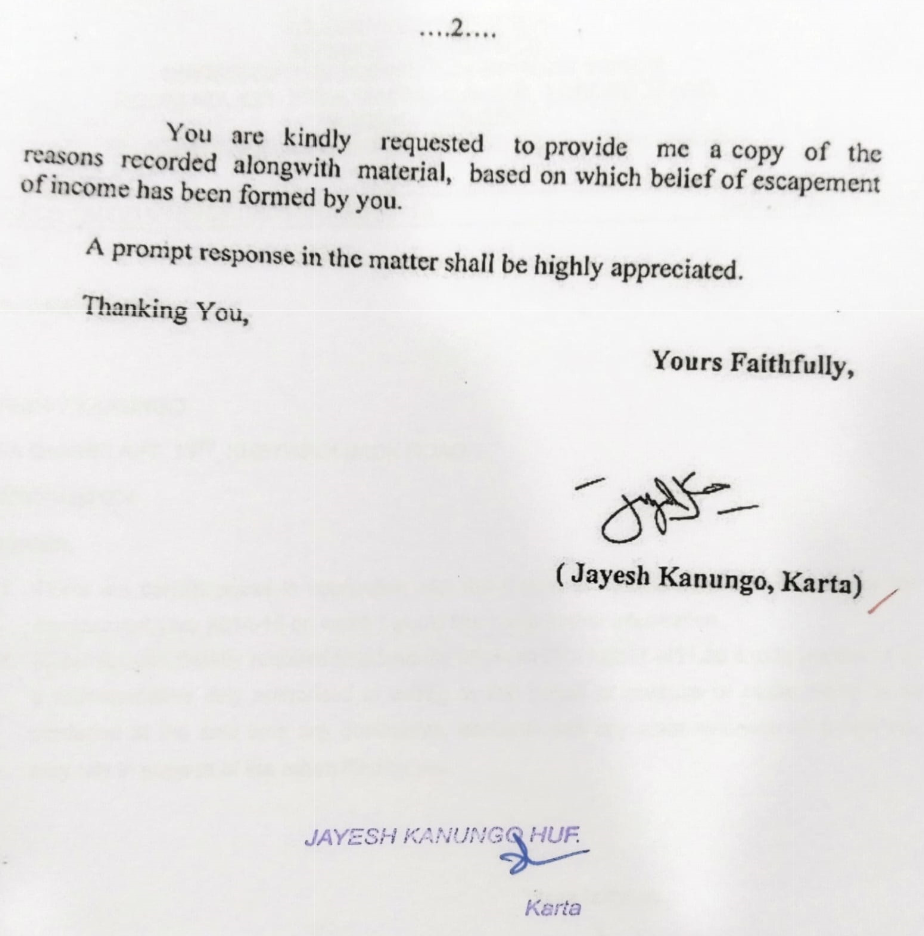

i) That the impugned assessment order passed by Id. ITO-19(2)(1), Mumbai without recording his own reason to reopen the assessment and issuing any own notice u/s.148 but on the basis of reason recorded and notice issued u/s.148 by non-jurisdictional ITO-19(3)(1), Mumbai being without jurisdiction and void ab initio hence may be quashed an

An indispensable Tool for Legal Professionals, Endorsed by Various High Court and Judicial Officers

Please visit our Training & Support

Center or Contact Us for assistance

Scan Me!

India’s Legal research and Law Firm App, Download now!

For Daily Legal Updates, Join us on :